Higher rates of Stamp Duty Land Tax (SDLT) on purchases of additional residential properties

Updated 16 March 2016

© Crown copyright 2016

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/consultation-on-higher-rates-of-stamp-duty-land-tax-sdlt-on-purchases-of-additional-residential-properties/higher-rates-of-stamp-duty-land-tax-sdlt-on-purchases-of-additional-residential-properties

Foreword

Owning a home is an aspiration for millions of people in our country. This government is committed to helping people achieve that aspiration, by supporting those who want to work hard, save and buy their own home. Home ownership is also a key part of the government’s plan to provide economic security for working people at every stage of their life.

In the last Parliament, we took significant steps to support housing supply and low-cost home ownership, and at the Spending Review and Autumn Statement 2015 we went further by announcing a bold Five Point Plan for housing. This Plan re-focuses support for housing towards low-cost home ownership for first-time buyers.

Alongside delivering 400,000 affordable housing starts by 2020-21, extending the Right to Buy to housing association tenants, accelerating housing supply and introducing London Help to Buy, the Five Point Plan includes the introduction of higher rates of Stamp Duty Land Tax (SDLT) on purchases of additional residential properties.

The higher rates will be 3 percentage points above the current SDLT rates, and will take effect from 1 April 2016. The government will use some of the additional tax collected to provide £60 million for communities in England where the impact of second homes is particularly acute.

The tax receipts will help towards doubling the affordable housing budget. This will help first time buyers and is part of the government’s commitment to supporting home ownership.

This consultation represents a real opportunity to inform and develop a key part of the government’s Five Point Plan for housing, and I look forward to the contributions of all interested parties.

Financial Secretary to the Treasury

1. Introduction

1.1 Background

The government announced at the Spending Review and Autumn Statement 2015 a Five Point Plan for housing, in order to re-focus support for housing towards low-cost home ownership for first-time buyers. This plan includes commitments to:

- deliver 400,000 affordable housing starts by 2020-21

- extend the Right to Buy to Housing Association tenants

- accelerate housing supply and get more homes built

- extend the Help to Buy: Equity Loan scheme to 2021 and create a London Help to Buy scheme, offering a 40% equity loan

- charge higher rates of Stamp Duty Land Tax (SDLT) on purchases of additional residential properties, such as buy-to-let properties and second homes, from 1 April 2016

The higher rates of SDLT are part of the government’s commitment to supporting home ownership. The higher rates will apply to most purchases of additional residential properties in England, Wales and Northern Ireland where, at the end of the day of the transaction, individual purchasers own two or more residential properties and are not replacing their main residence.

The higher rates will also generally apply to purchases of residential property by companies. The vast majority of transactions, such as first time buyers purchasing their first property or home owners moving from one main residence to another will be unaffected.

The government is considering an exemption from the higher rates for those making significant investments in residential property, given the role of this investment in supporting the government’s housing agenda. This is considered in more detail in section 2.

The government will use some of the additional tax collected to provide £60 million for communities in England where the impact of second homes is particularly acute. The tax receipts will also help towards doubling the affordable housing budget.

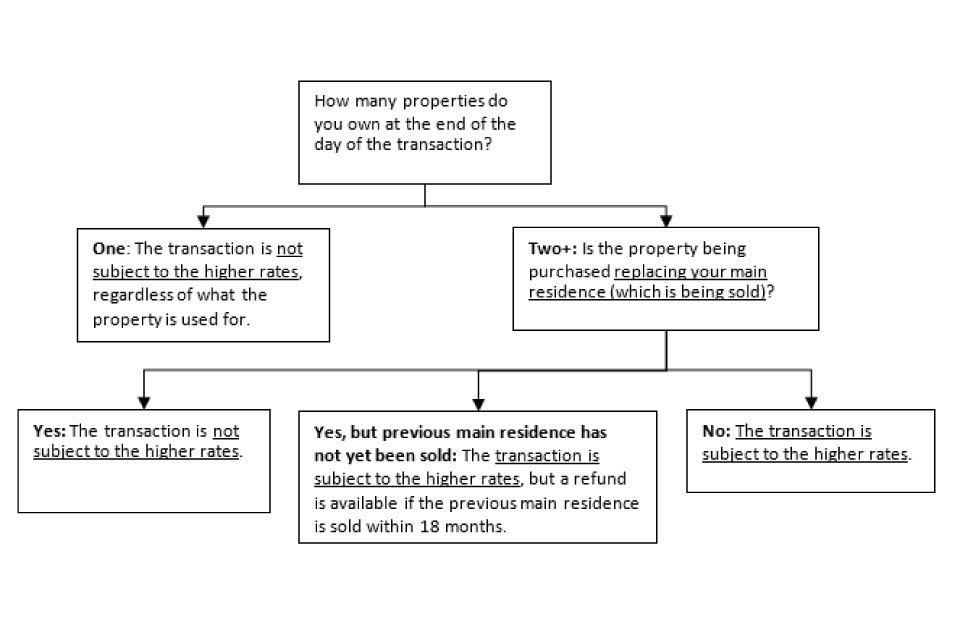

How to check if a purchase of a property by an individual is liable for the higher rates

Stamp Duty diagram

1.2 Aim of the consultation

This consultation sets out the details of the higher rates of SDLT and seeks views in key areas of its design. Views are invited from a wide range of respondents including individuals, companies, legal professionals and representative and professional bodies.

The government will consider all responses before confirming the final policy design at the Budget on 16 March 2016. In addition, the government is keen to engage with a wide range of stakeholders and will aim to hold a number of meetings to gather views on specific issues.

1.3 Policy context

The government is committed to supporting home ownership, which is an aspiration for many hard working people and provides security for families.

In the last Parliament, the government took significant steps to support housing supply and low cost home ownership – a reformed planning system, support for SME house builders and Help to Buy increased housing starts to a 7 year high and the number of first time buyers increased by almost 60% between 2010 and 2014.

Higher rates of SDLT on additional residential properties form part of the government’s Five Point Plan for housing. The government believes it is right that people should be free to purchase a second home or invest in a buy-to-let property.

However, the government is aware that this can impact on other people’s ability to get on to the property ladder. Applying higher rates of SDLT to additional residential property purchases is part of the government’s commitment to supporting home ownership and first time buyers.

SDLT is generally payable on the purchase or transfer of property where the amount paid is above a certain threshold. It applies to purchases in England, Wales and Northern Ireland and is payable by the purchaser. The amount payable varies depending on the purchase price and whether the property is being used for residential or non-residential purposes.

At the Autumn Statement 2014, the government radically reformed SDLT on residential properties, making the system fairer and more efficient and cutting SDLT for 98% of people who pay it. Previously, the system operated on a ‘slab’ structure, whereby tax was due at one percentage rate on the entire property value.

This was reformed to a structure where each new SDLT rate is payable on the portion of the value which falls within each band, like income tax.

1.4 Structure of the consultation

Section 2 of this consultation sets out the details of the proposed policy design. This includes a consideration of the circumstances in which a transaction would be subject to the higher rates, including identification of difficult cases, and the circumstances where exemption from the higher rates may be justified. Section 2 also sets out the government’s approach for how a main residence is to be defined.

Section 3 will explain potential changes to the administration of SDLT by HMRC and the processes taxpayers will be expected to go through to ensure compliance.

Section 4 provides detail on how the consultation process will work and how to respond.

1.5 Stage of consultation

The policy outlined in this document is at stage 2 (determining the best option and developing a framework for implementation including detailed policy design) of the government’s tax consultation framework.

1.6 Planned timeframe

This consultation will run from 28 December 2015 to 1 February 2016.

Confirmation of the final design will be announced at the Budget on 16 March 2016. The higher rates will apply from 1 April 2016.

2. Policy Design

2.1 Introduction

The higher rates of SDLT on purchases of additional residential properties continue the government’s commitment to supporting home ownership and first time buyers, and form part of the government’s Five Point Plan for housing.

In developing the policy proposals for the higher rates of SDLT, the government is seeking to balance support for the wider housing agenda whilst maintaining the efficiency, fairness and simplicity of the tax system, and minimising tax avoidance opportunities.

The vast majority of residential property transactions will not pay the higher rates of SDLT. In particular, the higher rates will never apply where, at the end of the day of the transaction, an individual purchaser only owns one residential property (or, in the case of joint purchasers, that at the end of the day of the transaction each one of the joint purchasers only own one residential property)[footnote 1].

The government estimates around 90% of residential property transactions in England, Wales and Northern Ireland will not pay the higher rates of SDLT.

The most common scenario in which purchasers will pay the higher rates is where they are purchasing a buy-to-let or second home in addition to their main home. More complex cases are discussed later on in this consultation.

The higher rates will only apply to additional residential properties purchased in England, Wales and Northern Ireland on or after 1 April 2016. The higher rates will be 3 percentage points above the current SDLT residential rates. They will be charged on the portion of the value of the property that falls into each band.

| Band | Existing residential SDLT rates | New additional property SDLT rates |

| £0* - £125k | 0% | 3% |

| £125k - £250k | 2% | 5% |

| £250k - £925k | 5% | 8% |

| £925k - £1.5m | 10% | 13% |

| £1.5m + | 12% | 15% |

*Transactions under £40,000 do not require a tax return to be filed with HMRC and are not subject to the higher rates.

Example 1:

An additional residential property is purchased for £200,000. SDLT is calculated as follows:

3% on the first £125,000 = £3,750

5% on the remaining £75,000 (the portion between £125,000 and £200,000) = £3,750

The total SDLT due is therefore: £3,750 + £3,750 = £7,500

Example 2:

An additional residential property is purchased for £100,000. SDLT is calculated as follows:

3% on £100,000 = £3,000.

2.2 When the higher rates will apply

The higher rates will not apply if at the end of the day of the transaction an individual owns only one residential property, irrespective of the intended use of the property.

Example 3:

X sells a property which was her main residence and purchases a new residential property. At the end of the day of the transaction she has one property, so X will not pay the higher rates of SDLT.

Example 4:

Y is purchasing his first property. At the end of the day of the transaction he owns one property, so he will not pay the higher rates of SDLT. This is regardless of whether Y intends to use it as a main residence or, for example, a rental property.

Example 5:

K, who lives in rented accommodation, sells the only residential property he owns, a buy-to-let, and purchases another buy-to-let. At the end of the day of the transaction he owns one property, so he will not pay the higher rates of SDLT.

If at the end of the day of the transaction an individual purchaser owns two or more residential properties, whether the purchaser pays the higher rates or not will depend on whether they are replacing their main residence (further details on what is a main residence are given in section 2.8).

If the purchaser has sold a previous main residence within 18 months before the day of the transaction and the transaction is a purchase of a new main residence, the purchaser will be considered to be replacing a main residence. Where an individual is replacing a main residence the higher rates of SDLT will not apply.

However, if the purchaser is not replacing a main residence (either because they have not sold a previous main residence within the last 18 months or the property being acquired is not a new main residence), the higher rates will apply.

Recognising that there may be certain circumstances where purchasers may end up in difficult circumstances, some purchasers will be eligible for a refund of the additional SDLT paid – this is discussed in more detail in section 2.11.

Figure 1: How to check if a purchase of a property by an individual is liable for the higher rates

Stamp Duty diagram

Example 6:

Z already owns a main residence and is purchasing a property that will be used as a buy-to-let. At the end of the day of the transaction she owns two properties and has not replaced her main residence, so the higher rates will apply.

Example 7:

A owns both a main residence and a second home. She sells her main residence and purchases a new one. Although she has two properties at the end of the day of the transaction, she has replaced her main residence so the higher rates will not apply.

Example 8:

H owns a main residence. He is purchasing a new main residence, but rather than selling his previous main residence he will rent it out. At the end of the day of the transaction H owns two properties and is not replacing a main residence (as he is not selling his previous main residence), so the higher rates will apply.

Example 9:

N purchases her first property, which she will use as a buy-to-let. At the end of the day of the transaction she owns one property, so she will not pay the higher rates of SDLT, even though she is not using it as her main residence.

Two years later, N purchases a residential property which she will use as her main residence, but she decides to keep her buy-to-let property. In this instance, as she has two properties at the end of the day of the transaction and has not replaced a main residence (as she has not sold a previous main residence), the higher rates will apply.

Example 10:

O is a buy-to-let investor with 10 residential properties in his portfolio. He also owns one residential property which he uses as his main residence. He decides to sell his previous main residence and purchase a new main residence.

At the end of the day of the transaction, he owns 11 properties – his new main residence and his 10 buy-to-let properties. However, as he has replaced his main residence he will not pay the higher rates of SDLT.

2.3 Transition

The higher rates will only apply to purchases of additional residential property which complete on or after 1 April 2016. If contracts are exchanged after 25 November 2015 then the higher rates will apply if the purchase is completed on or after 1 April 2016.

However, if contracts were exchanged on or before 25 November 2015 but not completed until on or after 1 April 2016, the higher rates will not apply.

Example 11:

V already owns a main residence and exchanges contracts to purchase an ‘off plan’ residential property on 25 November 2015. Once built, V will use this as a buy-to-let property. The transaction is completed on 15 April 2016.

Although the completion date is after 1 April 2016, as he exchanged on or before 25 November 2015 the higher rates will not apply.

Example 12:

A exchanges contracts on an additional property which she will use as a second home on 30 March 2016. The transaction is completed on 2 April 2016. She does not intend to sell her main home.

Contracts were exchanged after 25 November 2015 and the transaction was completed on or after 1 April 2016, so the higher rates will apply.

2.4 Married couples and civil partners

Married couples and civil partners who own one property at the end of the day of a transaction will not pay the higher rates of SDLT. However, if either of them owns more than one residential property they may pay the higher rates when purchasing another property.

The government will treat married couples and civil partners living together as one unit. This is consistent with other areas of the tax system including Capital Gains Tax private residence relief where married couples are entitled to relief on one residence between them.

This means that:

- married couples and civil partners may own one main residence between them at any one time for the purposes of the higher rates

- property owned by either partner (and any minor children) will be relevant when determining if an additional property is being purchased or not. Therefore, an individual buying a property may be liable for the higher rates if his or her spouse or civil partner has an existing residential property. If the spouse or civil partner then sells that residential property they may be able to claim a refund

Married couples and civil partners are treated as living together, and therefore as one unit, unless they are separated:

- under a court order; or

- by a formal Deed of Separation executed under seal.

In each case the marriage or civil partnership must have broken down. Where a married couple or civil partners sometimes live apart (but the relationship has not broken down), which property is the couple’s main residence will need to be determined by the facts (more detail is available in section 2.8).

Example 13:

Mr and Mrs I own a main residence together. They decide to purchase a second home jointly. At the end of the day of the transaction they own more than one residential property and are not replacing their main residence, so the higher rates will apply.

Example 14:

Mr and Mrs L own two residential properties jointly. Although they spend time in both, only one of these properties is their main residence. If they sell the residential property that is their main residence and purchase a new main residence, they will not pay the higher rates, as at the end of the day of the transaction they own two properties but are replacing their main residence.

However, if they sell the property that is not their main residence, their second home, and purchase another second home, they will pay the higher rates, as at the end of the day of the transaction they own two residential properties and have not replaced their main residence.

Example 15:

Mr and Mrs M are married. Mr M owns a home (which he purchased on his own before he was married) where the couple live as their main residence. Mrs M then buys a property to be rented out. At the end of the day of the transaction they own more than one residential property and are not replacing their main residence, so the higher rates will apply.

Example 16:

Mr A marries Mr B. They each own a property (which they purchased individually before they were married and used as their respective main homes). Mr B then sells his former main home and purchases a new property to rent out.

At the end of the day of the transaction Mr A and Mr B own more than one residential property and are not replacing their main residence, so the higher rates will apply.

Example 17:

Ms C and Ms D are in a civil partnership. Ms C owns a property (which she purchased on her own before her civil partnership) where they live together as their main residence. However, Ms C and Ms D decide to separate. After they have separated under a court order, Ms D decides to purchase a property.

At the end of the day of the transaction Ms D owns one residential property, so the higher rates will not apply.

Question 1:

Are there any difficult circumstances involving family breakdown which mean that treating married couples and civil partners as one unit until they are separated is not appropriate? If there are, how would you suggest those circumstances are treated?

2.5 Joint purchasers

There are many scenarios where two or more people may own or purchase property jointly.

The government proposes that if, at the end of the day of a transaction, any of the joint purchasers has two or more properties and is not replacing a main residence, the higher rates will apply to the entire consideration for the transaction. This provides simplicity and aligns with other areas of the tax system.

However, as the purchased property may be a first property for one or more of the joint purchasers, the government is keen to hear from respondents as to whether this is the fairest outcome.

Example 18:

F and G own a property jointly. F decides to purchase a buy-to-let property on his own. At the end of the day of the transaction he owns two properties and has not replaced his main residence, so the higher rates of SDLT will apply.

Example 19:

B and C are purchasing a property together. This will be B’s first property, but C owns another property that she is not selling. For C, this will be an additional property as, at the end of the day of the transaction, she will own two properties and is not replacing a main residence. Therefore, the higher rates of SDLT will apply.

Question 2:

Do you agree that, where property is purchased jointly, if any of the purchasers in a transaction are purchasing an additional residential property and not replacing a main residence, the higher rates should apply to the whole transaction value? If not, how would you suggest the government treats joint purchasers?

2.6 Partnerships

Partnerships are generally treated for SDLT as if the partners are joint purchasers of partnership property. The government intends that this treatment should also apply for the purposes of deciding whether higher rates of SDLT apply to partnership purchases and deciding whether individual partners have more than one property at the end of the day of purchase.

2.7 Purchasing a property for children to live in

The government appreciates that in many cases individuals and couples may help their children to get onto the property ladder. Whether the higher rates of SDLT will apply will depend on the structure of any transaction, and in particular who owns the property purchased.

Example 20:

Mr and Mrs J own a main residence together. They decide to purchase a property for their children to live in. At the end of the day of the transaction Mr and Mrs J own more than one residential property and are not replacing their main residence, so the higher rates will apply.

Example 21:

I owns one residential property. He decides to purchase another property jointly with his daughter. The property will be his daughter’s first property. At the end of the day of the transaction, I owns more than one residential property and has not replaced his main residence, so the higher rates will apply.

Example 22:

T helps her son, S, purchase his first residential property. She gives him money towards a deposit and acts as a guarantor on the mortgage, but will not jointly own the property with him. At the end of the day of the transaction S will own one property, so the higher rates will not apply.

2.8 Determining whether a purchaser is replacing an only or main residence

Where a purchaser (or, in the case of joint purchasers, all purchasers) own one property at the end of the day of a transaction they will not pay the higher rates. Purchasers will only need to determine whether they have replaced a main residence if they own two or more properties at the end of the day of the transaction.

In that situation, a purchaser will pay the higher rates of SDLT if they are not replacing their main residence. If they are replacing their main residence, they will not pay the higher rates.

In most cases, where individuals move house they may purchase and sell property on the same day (for example, if they are involved in a chain of transactions). However in some circumstances people may sell their old main residence some time before, or some time after, purchasing a new main residence.

These situations are considered in more detail in sections 2.9 and 2.10. Where an individual sells their previous main residence after purchasing a new main residence, a refund of the higher rates may be claimed. This is discussed further in section 2.11.

Most individuals only have one residence at any given time. Where an individual has more than one property, in most cases it will be clear which one is the main residence. For example where an individual owns two properties, one which they live in and one which they let out.

Individuals will not be able to elect which of their residences is their main residence and therefore the treatment of a main residence for the purposes of the higher rates of SDLT may differ from the treatment for capital gains tax.

The government’s view is that any elective treatment for SDLT may reduce uncertainty but it would be open to abuse and on balance is not justified. Instead, the government proposes that whether a property is a main residence will be based on fact.

HMRC will take into account a number of factors when considering whether a given property is an individual’s main residence. These will include:

- where the individual and their family spends their time;

- if the individual has children, where they go to school;

- at which residence the individual is registered to vote;

- where the individual works;

- the location and degree of furnishing and location of moveable possessions; and

- the correspondence and registration addresses given to various organisations.

In most cases the position will be clear and few factors will need to be considered. For example, where a married couple own two properties, one of which is convenient for their work and their children’s school and where they spend most of their time, and a holiday home which they visit occasionally, the former property would be their main residence.

The government proposes a two stage test to determine whether a purchase of a residential property is a replacement of a main residence or not. The first is whether, at the time of the transaction, a property sold in the last 18 months was the only or main residence of the individual. The second is whether the purchaser of the new property intends to occupy that property as their only or main residence.

When considering the first stage of the test, the property being sold must have been the only or main residence of the purchaser at some point in the 18 months before the purchase of the new property. In the majority of cases, an individual owns only one residence throughout a period, and it is this residence that will be their only or main residence.

Where an individual has more than one residence, which of these was their main residence will be a question of fact.

The second stage of the test is prospective and based on whether the purchaser intends to use the newly purchased property as their only or main residence. Where an individual has made plans at the date of purchase to move into the new property as their only residence, it will be obvious that the intention test is met.

Where evidence clearly shows that either another property will continue to be their main residence or that the property is purchased for some other purpose (such as use of a buy-to-let mortgage or other evidence of an intention to market the property for rent) the transaction will not be a replacement of a main residence.

Question 3:

For the first stage of the test for determining whether a purchaser is replacing an only or main residence, does considering previously disposed of property in the way presented above cause practical difficulties or hardship in particular cases?

Question 4:

For the second stage of the test, do you agree that the rule should require the purchaser to intend to use the newly purchased property as their only or main residence?

2.9 Delay between sale of a previous main residence and purchase of a new one

The government appreciates there may be circumstances where an individual sells a property which was their only or main residence, but there is then a period before they purchase their new main residence. The government does not want to disadvantage people in those circumstances.

The government believes that there should be a maximum 18 month period between sale of a previous main residence and purchase of a new main residence for the purpose of determining whether the higher rates apply.

The government is of the view that this is a sufficient period in the vast majority of cases.

Example 23:

G sold a property which was his main residence 3 months ago. He still owns another property which he lets out. Since the sale of his main residence he has lived in rented accommodation.

G then purchases a new residential property which he intends to use as a main residence.

At the end of the day of the transaction, he has two properties, but as he is replacing his main residence (he is purchasing a new main residence within 18 months of selling his previous main residence), the higher rates will not apply.

Example 24:

J owns two properties, a main residence and a holiday home. He decides to move into his holiday home as his new main residence, keeping his old main residence to let out.

3 months later, J sells his previous main residence and purchases a smaller property.

At the end of the day of the transaction, J has two properties, and whether the higher rates will apply will depend on whether J is replacing a main residence.

If J intends to move into the newly purchased property as his new main residence, the higher rates will not apply.

Question 5:

Do you agree that 18 months is a reasonable length of time to allow purchasers a period between sale of a previous main residence and purchase of a new main residence that allows someone to claim they are replacing their only or main residence and therefore not pay the higher rates of SDLT?

2.10 Overlap between purchase of new main residence and sale of previous main residence

In some circumstances, individuals will purchase a new main residence before disposing of their previous main residence. This may be intended, such as where multiple properties are owned temporarily due to employment or family reasons.

In some circumstances it may be unintended, such as where a purchaser was involved in a chain of transactions and the sale of a previous main residence fell through, but the purchaser proceeds on the purchase of their new main residence.

For purchasers who experience a temporary overlap between the purchase of a new main residence and the sale of a previous one, the government does not want to increase the overall tax burden.

In these situations, at the end of the day of the purchase of a new main residence the purchaser will own two or more properties and will not have replaced their previous main residence, as their previous main residence has not yet been sold.

It may be difficult to determine whether an individual has an intention to sell their previous residential property at this point, and a careful balance needs to be struck by the government to ensure that the tax system remains robust to tax avoidance and abuse.

Therefore, the government proposes that the higher rates of SDLT should apply to such transactions. To ensure fairness, the government proposes to introduce a refund mechanism for those who sell their previous main residence within 18 months of the purchase of the new main residence.

2.11 Refund upon sale of a previous main residence

This refund will be on the difference between the amount of SDLT paid under the higher rates and the amount of SDLT that would have been due under the normal residential SDLT rates.

This will mean that, after the refund, the purchaser will have paid the normal residential rates of SDLT.

A refund will be allowed in situations where a purchaser paid the higher rates of SDLT on the purchase of a new main residence and within 18 months disposes of a previous main residence.

Example 25:

Mr and Mrs K own one property, which is their main residence. They decide to purchase another property, which they will use as their main residence, but decide not to sell their previous main residence. At the end of the day of the transaction they own two properties and have not replaced their main residence, so the higher rates will apply.

Two months after this purchase, they sell their former main residence. Mr and Mrs K have disposed of a former main residence within 18 months of purchasing a new main residence. As such, upon sale of their previous main residence they will be eligible for a refund.

Example 26:

D and E are purchasing a property jointly which is intended to be their main residence. E already owns a property, which was previously used as a main residence, which he will not have sold at the time of purchase.

Upon purchase, as E will own two properties and has not replaced his main residence, the higher rates will apply. However, E then sells his previous main residence 12 months later. At this point, D and E will be eligible for a refund.

Example 27:

F is selling her main residence and purchasing a new one. However, her chain unexpectedly breaks down, meaning at the end of the day of the transaction she owns two properties and has not replaced her main residence.

Therefore, she will pay the higher rates. A month later, she sells her previous main residence. At this point F will be eligible for a refund.

Example 28:

Q owns a buy-to-let property. He decides to purchase a new residential property, but does not sell his existing property. At the end of the day of the transaction he owns two residential properties and has not replaced his main residence, so he will pay the higher rates of SDLT.

5 months later Q sells his buy-to-let property. As this buy-to-let property was not his main residence, he has not replaced his main residence. Therefore, he will not be eligible for a refund.

Question 6:

Do you agree there should be a refund mechanism in place for those who sell their previous main residence up to 18 months after the purchase of a new main residence? Are there any other cases where a refund of the additional SDLT paid should be given?

Question 7:

Can you suggest any other actions the government could take to mitigate the cash flow impact on those who only temporarily own two residential properties?

Question 8:

Are there any other situations regarding main residences which require further consideration?

The government appreciates that for purchasers who own two or more properties temporarily due to unintended circumstances, paying the higher rates of SDLT (and to potentially claim a refund shortly after) may seem burdensome.

In order to allow individuals whose purchase of a new main residence precedes the sale of a previous main residence by only a few days, it may be preferable to allow the normal rates of SDLT to be paid as long as the previous main residence has been sold by the time the SDLT return is filed.

Currently an SDLT return is due within 30 days of the completion of a purchase but at the Spending Review and Autumn Statement 2015 the government announced plans to consult on reducing this to 14 days.

Question 9:

Would there be a benefit to a significant number of purchasers if the test for whether someone owns one, or more than one, residential properties, were undertaken at the time of submitting the SDLT return, rather than at the end of the day of the transaction?

2.12 Property owned and purchased outside of England, Wales and Northern Ireland

SDLT only applies to purchases of land and property in England, Wales and Northern Ireland. A purchase of residential property located outside these areas will not pay SDLT, instead it may be liable for any property transactions tax in that jurisdiction.

Example 30:

R owns a property in Wales, which she uses as a main residence. She decides to purchase a buy-to-let property in Scotland. SDLT is devolved to Scotland, so she will not pay SDLT, but the Land and Buildings Transactions Tax (LBTT) on the purchase of the buy-to-let property. The rates and structure for LBTT are set by the Scottish Government.

However, property owned globally will be relevant in determining whether a property purchased in England, Wales or Northern Ireland is an additional property. This means that if someone is purchasing their first or only property in England, Wales or Northern Ireland, they may pay the higher rates if they own property outside these areas.

Example 31:

S owns a property in Scotland, which she uses as a main residence. She is purchasing her first property in England, Wales or Northern Ireland, which she will use as a second home. At the end of the day of the transaction she owns two or more properties globally and is not replacing her main residence, so she will pay the higher rates of SDLT.

Example 32:

T owns a property outside England, Wales and Northern Ireland which he uses as a main residence. He decides to sell that property and purchase a residential property in England, Wales or Northern Ireland. At the end of the day of the transaction he owns one residential property globally, so he will not pay the higher rates of SDLT.

Question 10:

Do you agree with the government’s proposed approach to considering property owned anywhere in the world when determining whether the higher rates of SDLT will be due?

2.13 Inherited properties

Individuals do not pay SDLT on properties they inherit, and this treatment will not change with the introduction of the higher rates of SDLT. However, inherited property will be relevant when determining if a purchaser is purchasing an additional residential property or not.

Example 33

U owns a property which she uses as a main residence. She inherits a property from her parents. An inheritance is not chargeable to SDLT, so she will not pay SDLT, even though after the inheritance she owns two properties. U decides to sell the inherited property and purchase a buy-to-let with the proceeds.

After this purchase, she has two or more residential properties and has not replaced her main residence. Therefore, she will pay the higher rates of SDLT on the newly purchased buy-to-let property.

2.14 Other cases

Employer provided accommodation

Work related accommodation which is provided and owned by an employer does not count when considering whether an individual is purchasing an additional property or not.

If an individual is living in work related accommodation provided and owned by their employer, that individual will be able to purchase one property without the higher rates applying (even if it will not be used as a main residence) as at the end of the day of purchase they will own one property.

Furnished holiday lets

The government proposes that properties bought as furnished holiday lets should be treated in the same way as all other residential properties – if the property is purchased as an additional property the higher rates will apply.

Timeshare properties

In most instances, timeshare agreements are not chargeable for SDLT purposes and therefore the higher rates will not apply to purchases of timeshares.

In rare circumstances, the timeshare agreement may be chargeable to SDLT, depending on the details of the agreements. If a timeshare agreement is chargeable to SDLT, the higher rates may apply.

Caravans, mobile homes and houseboat purchases

The purchase of caravans, mobile homes and houseboats does not create the same issues for home owners and first time buyers as second homes or buy-to-let properties. Therefore, the government will exclude all purchases of caravans, mobile homes and houseboats from the higher rates.

The ownership of a caravan, mobile home or houseboat will not be taken into account when determining whether a new property purchase by an individual is an additional property.

Example 34:

V lives in accommodation provided and owned by her employer. She decides to purchase a property, which will be the only property she owns. At the end of the day of the transaction she owns one property, so she will not pay the higher rates.

Question 11:

Do you agree with the proposed treatment of furnished holiday lets?

Question 12:

Are there any other cases which the government should consider?

2.15 The treatment of properties under £40,000

Currently, all transactions under £40,000 do not require an SDLT return to be filed with HMRC where no tax is due. This provides simplicity and minimises taxpayer burden. This will remain the case for purchases of additional residential property.

Residential properties, including a tenancy or lease of a residential property, worth less than £40,000 will not be taken into account when determining if an additional residential property is being purchased.

Example 35:

B owns a residential property which he uses as a main residence. He then purchases a property for £25,000 which he will use as a second home. The purchase price is less than £40,000 and so the higher rates will not apply.

Example 36:

G currently owns a property worth less than £40,000 which he does not intend to sell. He decides to purchase another residential property. At the end of the day of transaction, he is deemed to own one residential property as his ownership of the property worth less than £40,000 is not taken into account. Therefore, the higher rates will not apply.

2.16 Treatment of non-residential property purchases

The higher rates of SDLT will only apply to purchases of residential property. The definition of residential property and non-residential property will not change due to the introduction of these higher rates. This means that a purchaser of a non-residential property will never pay the higher rates of SDLT, even if it is later converted into residential property.

Non-residential property includes:

- commercial property (such as shops or offices);

- agricultural land;

- bare land (even where that land may subsequently be used for residential purposes);

- forests;

- any other land or property which is not used as a residence;

- 6 or more residential properties bought in a single transaction; and

- A mixed use property (one with both residential and non-residential elements).

Mixed use transactions, that is the purchase of residential and non-residential properties together in a single transaction, is currently considered a non-residential transaction for SDLT purposes. The government does not intend to change that treatment.

2.17 Treatment of multiple residential property purchases

Where multiple residential properties are purchased in a single or linked transaction, that transaction is eligible for multiple dwellings relief (MDR).

Under MDR, the residential rates of SDLT are applied to the average price of each property (multiplied by the number of properties purchased) rather than applying to the entire transaction value.

This brings the total SDLT due closer to the amount that would be due if the same properties had been purchased separately.

Where 6 or more residential properties are bought together, the purchaser can choose whether to apply the non-residential rates of SDLT (to the entire transaction value) or to choose the residential rates of SDLT with MDR applied.

The government intends to retain this system for the purchase of multiple residential properties.

When the new higher rates come into force this will mean purchases of multiple residential properties in one transaction, where some or all of them are additional properties, will be eligible for multiple dwellings relief, with the higher rates applied to the average price of the dwelling purchased.

For purchases of 6 or more residential properties in the same transaction, the purchaser will be able to choose whether multiple dwellings relief, with the higher rates, will apply, or the non-residential rates (which will be charged on the total purchase price).

Example 37:

A developer purchases 10 additional residential properties in one transaction, for a total of £3 million. The average purchase price is therefore £300,000. He is purchasing 6 or more residential properties in the same transaction, so he can chose whether multiple dwellings relief, with the higher rates, will apply, or the non-residential rates.

Multiple dwellings relief:

The SDLT due, with the higher rates applied, on the average purchase price of £300,000 is £14,000. This is then multiplied by the number of properties (10) to give the total amount of SDLT due - £140,000.

Non-residential rates:

The non-residential rates apply to the total transaction value - £3 million. As this is in the 4% band, SDLT will be due at 4% on £3 million - £120,000. In this instance, the developer will chose to pay under the non-residential rates.

2.18 The treatment of registered social landlords and charities

The SDLT system currently includes exemptions for some residential property purchases made by charities and registered social landlords. It is not the government’s intention to bring either charities or registered social landlords into the higher rates of SDLT in circumstances in which they would usually be exempt.

2.19 The treatment of large scale investors

The new higher rates of SDLT form part of the government’s overall housing strategy including support for home ownership. The higher rates of SDLT are therefore intended to apply to the vast majority of circumstances where individuals or companies and other non-natural persons purchase additional properties, which can impact on other people’s ability to get on the housing ladder.

However the government is aware that some purchases of additional properties can positively contribute to an overall increase in housing supply and support the government’s wider housing strategy, helping to facilitate the development and quality of the housing stock across tenure types.

Given the potential positive impacts some significant developments can have, an exemption from the higher rates of SDLT targeted at some forms of investment in property may be justified.

In designing any exemption a careful balance needs to be struck to ensure that the higher rates of SDLT support home ownership and first time buyers, and do not discourage those significant investments in residential property.

These developments may be new-build, converted buildings or renovation and conservation projects. Significant investments may also be made via the bulk purchase of existing housing stock, freeing up finance for developers to undertake other projects and providing greater certainty to developers.

Where these developments involve the bulk purchase of multiple completed units multiple dwellings relief (MDR) is available.

The development certainty and diversity of finance which may be provided by very large investors may be less likely to come from individuals or smaller companies and institutions. Small scale individual landlords, for example, may be more likely to purchase individual properties sequentially from the existing housing stock, directly competing against first time buyers for properties.

Where individual landlords do purchase individual units off-plan in new developments, they may be less likely to achieve the scale of investment needed to provide certainty or security to a development.

The government wants to ensure that any exemption is narrowly targeted to apply only to those purchases of additional properties which significantly contribute to new housing supply and the government’s wider housing objectives.

The Autumn Statement indicated the government’s initial view was that any exemption from the higher rates would only apply to corporates and funds (such as companies, and pension and collective investment schemes) who have an existing residential property portfolio of at least 15 properties at the time of a transaction.

Since then, the government has considered that there may be circumstances where significant investment by individual purchasers may positively contribute to development and the government’s housing objectives in the same way as investment by corporate purchasers, and so there may be circumstances in which it is justified to exempt purchases made by individuals from the higher rates.

There are also a number of alternative methods of designing an exemption focused on significant investment and the increase in overall housing supply which may be more targeted than by designing an exemption by reference to the purchaser’s existing property portfolio.

For example, it may be more appropriate to target an exemption based on the bulk purchase of at least 15 residential properties, on the basis that bulk purchases are more likely to provide significant sources of finance and development certainty to a project.

Given this, the government would be interested in respondent views on whether an exemption from the higher rates which was instead targeted at the bulk purchase of at least 15 residential properties in one transaction would be a better approach, and whether there is evidence to suggest that this exemption should be available to individual investors as well as non-natural persons.

Question 13:

Do you agree that an exemption should be available to individual investors as well as all non-natural persons? Alternatively, is there evidence to suggest any exemption should be limited to only certain types of purchaser? If so, which types of purchaser?

Question 14:

Do you think that either the bulk purchase of at least 15 residential properties or a portfolio test where a purchaser must own at least 15 residential properties are appropriate criteria for the exemption? Which would be better targeted?

Question 15:

Are there better alternative or additional tests that could be used to better target an exemption and fulfil the government’s wider housing objectives?

Question 16:

Are there any other issues or factors the government should take into account in designing an exemption from the higher rates?

2.20 The first purchase of a residential property by a company or collective investment vehicle

As made clear in this consultation, where an individual purchases their first residential property the higher rates will not apply. If the government mirrored this treatment for purchases made by companies and collective investment vehicles this would create a potential tax avoidance opportunity.

In particular, an individual could purchase an additional property via a company to avoid the higher rates of SDLT.

To guard against this avoidance risk the government proposes that the first purchase of a residential property by a company or collective investment vehicle is subject to the higher rates of SDLT (subject to the final decision on the treatment of significant investors as discussed in section 2.19).

Question 17:

Do any specific kinds of collective investment vehicle or other non-individuals need to be treated differently to companies?

2.21 The treatment of trusts and settlements

Property is sometimes held by trustees in trusts, and to ensure the fairness and integrity of the tax regime the higher rates of SDLT will apply to some purchases made by trusts.

Purchases by trustees of bare trusts will continue to be treated as if they are made by the beneficial owner and there will be no difference in treatment compared to the beneficial owner purchasing themselves.

Trust that are not bare trusts could be used as a vehicle to hold existing property so that an individual appears to have no other interests in property at the end of the day of a property purchase.

In order to prevent this, the government intends to treat certain beneficiaries of trusts as owning interests in a residential property if the trust owns an interest in a residential property.

The government considers that beneficiaries with a life interest or interest in possession under a trust should be treated in this way.

Less immediate or certain interests like interests in remainder or discretionary interests in property could give individuals a financial interest in a property. The government considers that generally, interests in remainder and discretionary interests are too remote or insignificant to be counted as an interest held by the beneficiary.

In order to not disadvantage those whose homes are held in trust because of either inheritance or because the beneficiary is disabled, the government does not want the higher rates to apply to either the purchase of an individual beneficiary’s residence where no other property is owned by the individual or to the replacement of a beneficiary’s only or main residence.

It is the intention, so far as possible for the purposes of determining whether the higher rate is payable, to treat purchases by trustees for beneficiaries with life interests or interests in possession as if the purchase were made by the individual themselves.

Purchases by trustees where beneficiaries have no interest in possession over the property will be liable to the higher rates.

Example 38:

A, the trustee of a new settlement for the benefit of B for life, remainder to C, purchases a property. B is an individual who owns no existing property. B is entitled to occupy the purchased property under the terms of the settlement. This will be B’s only property at the end of the day of the transaction, so A will not pay the higher rates of SDLT.

This is the case regardless of whether C owns a property. After this, B purchases a property in his own right. At the end of the day of the transaction, B has interest in two properties (as B’s interest in possession in respect of the property owned by the trust counts), so B will pay the higher rates of SDLT.

Example 39:

D, the trustee of a discretionary settlement for the benefit of individuals, E, F and G, purchases a property. None of the beneficiaries have a right to occupy the property under the trust, nor can they require D to pay them any income from the property.

There are no beneficiaries with a right to the income from the property or entitled to occupy the property under the terms of the settlement and so D will pay the higher rates of SDLT. Later, E purchases his first property. At the end of the day of the transaction, he owns one property.

E’s possible future benefit from the trust does not amount to an interest in an existing property for the purposes of determining whether the higher rates apply, so E does not pay the higher rates of SDLT.

Example 40:

H, the trustee of a settlement for the benefit of J for life, remainder to K, owns a property which is J’s only residence. H also owns an investment property. H sells J’s main residence and then purchases a new residence that J intends to occupy as his only residence.

At the end of the day of the transaction, J has an interest in two properties (the new main residence and the investment property), but as his main residence has been replaced, H will not pay the higher rates of SDLT.

Question 18:

Do you agree with the proposed treatment of trusts, including the higher rates of SDLT applying to trusts purchasing residential property except where a purchase is a first property or replacement of a main residence for a beneficiary?

3. Administration and compliance

3.1 Changes to the SDLT return form

In order to administer and ensure compliance with the new higher rates, changes will be required to the existing SDLT return.

Taxpayers will have to specify that a given transaction is for an additional residential property. This will leave the SDLT return with four categories of property: residential property, non-residential property, mixed, and residential – additional property.

The government recognises that the higher rates of SDLT will create additional requirements for agents acting for purchasers. The government expects most of the additional information that needs to be obtained from purchasers will be straightforward and uncontroversial.

For example, questions about whether the purchaser (or any joint purchaser) will own more than one residential property at the end of the day of the transaction will need to be considered. This information will need to be kept up to date by the purchaser and the conveyancer during the period between instruction and completion.

One piece of information which will be required from purchasers is whether any newly purchased residential property will be a main residence and replacing a previous main residence. This would be required in a situation where a purchaser with multiple properties at the end of the day of a transaction would not pay the higher rates.

In order to determine this, agents will need to determine whether the purchaser has disposed of any residential property within 18 months of the new transaction and whether or not that disposal was a disposal of the purchaser’s only or main residence.

Ultimate responsibility for the accuracy of an SDLT return remains with the purchaser and HMRC will provide guidance on how purchasers can determine whether the disposal of a property can be considered as a disposal of a main residence.

Conveyancers may not be best placed to judge whether a purchaser is correct about which property has been their main home. The government recognises that conveyancers are a key part of ensuring SDLT compliance and are keen to maintain this.

The government is considering how it can help conveyancers other than by providing written guidance, calculators and publicising the consequences for purchases of getting things wrong.

The government would be interested in views as to whether a specific set of questions designed by HMRC for conveyancers to use with their clients would aid compliance.

Question 19:

Do you think that purchasers are more likely to give accurate answers to main residence questions if HMRC provides specific questions for the conveyancer to ask the purchaser?

Question 20:

Would a formal declaration by the purchaser that the answers to any such questions are accurate help to increase compliance without creating undue burdens for conveyancers? How do you think such a declaration should work?

Question 21:

Besides normal publicly available guidance, are there any additional products that HMRC can provide to help purchasers understand what rates of tax they will be paying on a planned purchase?

3.2 Refund mechanism

Where an individual has purchased a new main residence but not yet sold a previous main residence, they will pay the higher rates.

If, within 18 months of purchasing the new main residence they then sell their old main residence, they will be entitled to a refund on the higher rates paid. This scenario is described in sections 2.10 and 2.11.

Currently the number of refunds claimed by taxpayers through the SDLT system is small, unlike other taxes where amendments to returns are more common. The government will be making changes to the administration of SDLT to allow claims for refunds of the higher rates for the scenarios outlined in sections 2.10 and 2.11.

In considering how any refund mechanism should work, the government is seeking to balance the need to ensure any process is simple and convenient for taxpayers, but is also robust to abuse.

As SDLT is a tax dealt with largely by solicitors and conveyancers, there may be a benefit to linking the process and timing of claiming for a refund with the sale of the previous main residence which triggers this refund.

HMRC is designing a suitable system for the filing of claims and payment of refunds in a secure fashion whilst minimising turnaround time. It is likely that this will take the form of a standalone online process. HMRC will consult with stakeholders on the design of the refund process.

Example 42:

M purchases an additional residential property for £250,000 which he intends to live in, before he sells his previous main residence.

As at the end of the day of the transaction M owns more than one residential property and has not replaced his main residence, so he will pay the higher rates of SDLT. The amount of SDLT paid is £10,000.

M uses his newly purchased property as a main residence, and six months later, sells his previous main residence. As he is disposing of a previous main residence within 18 months of purchasing a new main residence, so M is eligible for a refund.

M will be refunded £7,500, which is the difference between the SDLT he paid (£10,000) and the SDLT due under the normal residential SDLT rates (£2,500).

3.3 Compliance

SDLT is a self-assessment tax and purchasers are responsible for the accuracy of their own returns. Where an understatement of SDLT results from a mistake and that mistake is careless or deliberate, penalties of up to 100% of the tax understated can apply alongside other sanctions.

HMRC will use other information available to it to identify returns that may be incorrect and undertake compliance to determine whether there are under or overstatements of tax liability. HMRC has nine months following submission of an SDLT return to open an enquiry.

HMRC can ask for information in support of an individual’s claim that a property was or was intended to be their only or main residence.

4. The consultation process

4.1 Responding to the consultation

The closing date for this consultation is 1 February 2016.

Responses to the consultation should be sent either by post to:

SDLT Additional Properties Consultation

Enterprise and Property Tax Team

HM Treasury

1 Horse Guards Road

London

SW1A 2HQ

or email: sdltadditionalproperties@hmtreasury.gsi.gov.uk

When responding, please state whether you are responding as an individual or as part of an organisation. If responding on behalf of a representative body please make it clear who the organisation represents and, where applicable, how the members’ views were assembled.

The government is keen to engage with a wide range of stakeholders and will aim to hold a number of meetings to gather views on specific issues during the consultation period.

4.2 Confidentiality and disclosure

All written responses may be made public on the Gov.uk website unless the author specifically requests otherwise in writing.

Information provided in response to this consultation, including personal information, may be published or disclosed in accordance with the access to information regime. These are primarily the Freedom of Information Act (FOIA), the Data Protection Act (DPA) and the Environmental Information Regulations 2004.

If you would like the information that you provide to be treated as confidential, please be aware that, under the FOIA, there is a statutory Code of Practice with which public authorities must comply and which deals, amongst other things, with obligations of confidence.

In view of this, it would be helpful if you could explain to us why you regard the information you have provided as being confidential. If we receive a request for disclosure of information we will take full account of your explanation, but we cannot give an assurance that confidentiality will be maintained in all circumstances.

In the case of electronic responses, general confidentiality disclaimers that often appear at the bottom of emails will be disregarded for the purpose of publishing responses unless an explicit request for confidentiality is made in the body of the response.

Subject to the previous two paragraphs, if you wish part (but not all) of your response to remain confidential, please supply two versions, one for publication on the website with the confidential information deleted, and another confidential version for use by the Treasury.

Any FOIA queries should be sent by post to:

Correspondence and Enquiry Unit

Freedom of Information Section

HM Treasury

1 Horse Guards Road

London

SW1A 2HQ

Or by email to: public.enquiries@hmtreasury.gsi.gov.uk

4.3 The government’s code of practice on consultation

This consultation is being conducted in accordance with the government’s code of practice on consultation. A copy of the code of practice criteria and a contact for any comments on the consultation process can be found in Annex B.

At 7 weeks, this consultation is shorter than the standard consultation time so that the responses can inform the government before the higher rates take effect.

4.4 Next steps

This consultation will last for a period of 5 weeks, closing on 1 February 2016. After the consultation period has closed, the government will consider the responses to the consultation. In line with the code of practice for written consultations, the government will publish a summary of responses to the consultation.

Annex A: Summary of consultation questions

Question 1:

Are there any difficult circumstances involving family breakdown which mean that treating married couples and civil partners as one unit until they are separated is not appropriate? If there are, how would you suggest those circumstances are treated?

Question 2:

Do you agree that, where property is purchased jointly, if any of the purchasers in a transaction are purchasing an additional residential property and not replacing a main residence, the higher rates should apply to the whole transaction value? If not, how would you suggest the government treats joint purchasers?

Question 3:

For the first stage of the test for determining whether a purchaser is replacing an only or main residence, does considering previously disposed of property in the way presented above cause practical difficulties or hardship in particular cases?

Question 4:

For the second stage of the test, do you agree that the rule should require the purchaser to intend to use the newly purchased property as their only or main residence?

Question 5:

Do you agree that 18 months is a reasonable length of time to allow purchasers a period between sale of a previous main residence and purchase of a new main residence that allows someone to claim they are replacing their only or main residence and therefore not pay the higher rates of SDLT?

Question 6:

Do you agree there should be a refund mechanism in place for those who sell their previous main residence up to 18 months after the purchase of a new main residence? Are there any other cases where a refund of the additional SDLT paid should be given?

Question 7:

Can you suggest any other actions the government could take to mitigate the cash flow impact on those who only temporarily own two residential properties?

Question 8:

Are there any other situations regarding main residences which require further consideration?

Question 9:

Would there be a benefit to a significant number of purchasers if the test for whether someone owns one, or more than one, residential properties, were undertaken at the time of submitting the SDLT return, rather than at the end of the day of the transaction?

Question 10:

Do you agree with the government’s proposed approach to considering property owned anywhere in the world when determining whether the higher rates of SDLT will be due?

Question 11:

Do you agree with the proposed treatment of furnished holiday lets?

Question 12:

Are there any other cases which the government should consider?

Question 13:

Do you agree that an exemption should be available to individual investors as well as all non-natural persons? Alternatively, is there evidence to suggest any exemption should be limited to only certain types of purchaser? If so, which types of purchaser?

Question 14:

Do you think that either the bulk purchase of at least 15 residential properties or a portfolio test where a purchaser must own at least 15 residential properties are appropriate criteria for the exemption? Which would be better targeted?

Question 15:

Are there better alternative or additional tests that could be used to better target an exemption and fulfil the government’s wider housing objectives?

Question 16:

Are there any other issues or factors the government should take into account in designing an exemption from the higher rates?

Question 17:

Do any specific kinds of collective investment vehicle or other non-individuals need to be treated differently to companies?

Question 18:

Do you agree with the proposed treatment of trusts, including the higher rates of SDLT applying to trusts purchasing residential property except where a purchase is a first property or replacement of a main residence for a beneficiary?

Question 19:

Do you think that purchasers are more likely to give accurate answers to main residence questions if HMRC provides specific questions for the conveyancer to ask the purchaser?

Question 20:

Would a formal declaration by the purchaser that the answers to any such questions are accurate help to increase compliance without creating undue burdens for conveyancers? How do you think such a declaration should work?

Question 21:

Besides normal publicly available guidance, are there any additional products that HMRC can provide to help purchasers understand what rates of tax they will be paying on a planned purchase?

Annex B: The code of practice on consultation

This consultation is being conducted in line with the code of practice for written consultation, which sets down the following criteria:

- formal consultation should take place at a stage when there is scope to influence the policy outcome

- consultations should normally last for at least 12 weeks with consideration given to longer timescales where feasible and sensible

- consultation documents should be clear about the consultation process, what is being proposed, the scope of influence and the expected costs and benefits of the proposals

- consultation exercises should be designed to be accessible to, and clearly targeted at, those people the exercise is intended to reach

- keeping the burden of consultation to a minimum is essential if consultations are to be effective and if consultees’ buy-in to the process is to be obtained

- consultation responses should be analysed carefully and clear feedback should be provided to participants following the consultation; and

- officials running consultations should seek guidance in how to run an effective consultation exercise and share what they have learned from the experience

If you feel that this consultation does not fulfil these criteria, please contact:

Consultation Coordinator

HM Revenue & Customs

100 Parliament Street

London

SW1A 2BQ

Or email: HMRC Consultation co-ordinator

-

Throughout this consultation ‘residential property’ means a dwelling. ↩