PPN 06/21: Frequently asked questions

Updated 17 April 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/procurement-policy-note-0621-taking-account-of-carbon-reduction-plans-in-the-procurement-of-major-government-contracts/ppn-0621-frequently-asked-questions

1. Who does the policy and guidance apply to?

The Procurement Policy Note (PPN) applies to all Central Government Departments, their Executive Agencies and Non Departmental Public Bodies in conducting procurement procedures regulated by the Public Contracts Regulations 2015. They are referred to in the PPN and associated guidance as ‘In-scope Organisations’.

2. When should this PPN be applied?

PPN 06/21 was published on 5th June 2021, and came into effect for new procurements launched from 30th September 2021. From this date, In-Scope Organisations should take action to apply PPN 06/21 when procuring goods and/or services and/or works which are subject to the Public Contracts Regulations 2015, where there is an anticipated contract value of £5 million per annum and above (excluding VAT), unless it is not related to the subject matter of the contract and proportionate to do so.

PPN 06/21 applies to the procurement of framework agreements and dynamic purchasing systems (DPS) only where it is related to the subject matter of the contract and proportionate, and where it is anticipated that the individual value of any contract to be awarded under the framework agreement or DPS is £5 million per annum and above (ex VAT). Where a framework/DPS is in scope, and it is related to the subject matter of the contract and proportionate, PPN 06/21 should be applied at framework/ DPS level, rather than to individual call-offs.

3. Should PPN 06/21 be applied by Devolved Administrations?

PPN 06/21 is not stated to be mandatory for Devolved Administrations. However it has been adopted by the Welsh Government and mandated for Welsh Government contracts valued at £5 million or above from 1 April 2022 and recommended as good practice to the rest of the Welsh Public Sector. Please see WPPN 06/21 for details.

4. Is PPN 06/21 applied to call offs from frameworks or Dynamic Purchasing Systems?

PPN 06/21 applies to the procurement of framework agreements and DPS only where:

- it is related to the subject matter of the contract and proportionate, and

- where it is anticipated that the individual value of any contract to be awarded under the framework agreement or DPS is £5 million per annum and above (ex VAT).

Where a framework agreement or DPS has included PPN 06/21, the measure should be included in the Selection Questionnaire or DPS Questionnaire (DPSQ) for the Framework or DPS. In-scope organisations may verify that the supplier continues to meet the Carbon Reduction Plan (CRP) requirements prior to entering into a call off contract.

5. Does PPN 06/21 apply to contracts that were started before 30th September 2021?

No, the effective date for the PPN is 30th September 2021, meaning that it should be applied to relevant procurements which have commenced on or after that date.

6. How do I determine if PPN 06/21 is related to the subject matter of the contract and proportionate to my procurement?

Environmental considerations and carbon reduction will be a factor in the delivery of most, if not all, contracts. It is expected that in the majority of cases for contracts with a value exceeding £5 million per annum, PPN 06/21 will be related to the subject matter of the contract and proportionate to assess whether the supplier has the necessary technical ability to perform the contract, taking into account such factors.

This may include, but is not limited to:

- Contracts which have a direct impact on the environment in the delivery of the contract;

- Contracts which require the use of buildings by staff engaged in the delivery of the contract;

- Contracts which require the transportation of goods or people used in the delivery of the contract;

- Contracts which require the use of natural resources in the delivery of the contract.

7. How should PPN 06/21 be applied in the commercial process?

PPN 06/21 should be applied at the selection stage of the procurement, and included in the SQ. PPN 06/21 introduces a new criterion which requires bidding suppliers to detail their commitment to achieving Net Zero through the publication of a CRP in order to pass and proceed further in the competition.

Suppliers’ CRPs should not be scored’ or compared against each other and assessment takes the form of a check that they meet the requirements of the measure. Further guidance on selection questions and how to apply them and assess supplier responses can be found in the Guidance on adopting and applying the Carbon Exclusion Measure in the procurement of major contracts

8. How should we assess supplier responses?

PPN 06/21 is applied at the selection stage of the procurement. Suppliers’ CRPs should not be scored or compared against each other and assessment takes the form of a check that they meet the requirements of the measure.

Example: Supplier A and Supplier B have both submitted CRPs which meet the requirements of the measure. Supplier A has committed to achieving Net Zero by 2050. Supplier B has committed to achieving Net Zero by 2030. In this instance both will pass, and neither scores higher or has any other advantage over the other.

Further guidance on selection questions and how to apply them and assess supplier responses can be found in the Guidance on adopting and applying the Carbon Exclusion Measure in the procurement of major contracts

9. What should the Carbon Reduction Plan contain?

In-scope organisations should satisfy themselves that suppliers have provided a published CRP which:

- Has been published on the supplier’s website

- Has been signed off at an appropriate level within 12 months of the date of the procurement

- Includes a signed declaration confirming the supplier’s commitment to achieving Net Zero by 2050 (at the latest)

- Details the supplier’s Greenhouse Gas emissions

- Details the environmental management measures that can be applied in the delivery of the contract.

Full details of the reporting requirements for Carbon Reduction Plans can be found in the Technical standard for Completion of Carbon Reduction Plans. Further guidance on selection questions and how to apply them and assess supplier responses can be found in the Guidance on adopting and applying the Carbon Exclusion Measure in the procurement of major contracts

10. Can I accept suppliers’ corporate social responsibility (CSR) statements, policies and/or case studies as proof instead of a Carbon Reduction Plan?

No, CSR statements, policies and/or case studies cannot be accepted instead of a CRP. To ensure compliance, suppliers should complete the CRP template provided in PPN 06/21. The CRP template has been created to collate the required information in one place for ease of use for commercial teams, and to minimise the burden placed upon suppliers, particularly start-ups, Small and Medium Sized Enterprises (SMEs) and Voluntary, Community and Social Enterprises (VCSEs).

Deviations from the template format will only be accepted if all the information requested in the template is provided in accordance with the requirements of the policy, guidance and Technical Standard. Suppliers will only require one CRP (valid for 12 months), which can be used for all procurements where the measure is adopted.

11. Can I accept commitments under the Science Based Targets Initiative (SBTI) or Race to Zero as evidence of compliance with PPN 06/21?

The Race to Zero and the SBTI are schemes for suppliers to demonstrate their commitment to reducing emissions over time. However, these schemes do not align with the requirements of PPN 06/21 and a CRP based on/using the template outlined in PPN 06/21 is required.

Suppliers may detail their membership of schemes such as SBTI or Race to Zero within their CRP as an example of the environmental management measures they have in place.

12. Why are you looking at emissions from the bidding entity and not the entity’s wider UK business emissions as a whole?

In-scope organisations must determine whether the supplier (i.e. the bidding entity) has the necessary technical ability to deliver the contract requirements, as it is the bidding entity that the In-scope organisation will be entering into contract with.

Whilst many suppliers have different trading entities within their wider business which are used to bid for government work, it is only the bidding entity that is relevant to be considered for the purposes of applying this policy.

Where the bidding entity is different from the UK or global parent, CRPs should reflect the commitments and emissions of the bidding entity. Where a supplier has existing emissions reporting or commitments which do not align with the boundary of the bidding entity, suppliers should consider the Technical standard for Completion of CRPs and adopt an appropriate methodology to account for emissions incurred by the bidding entity.

This may include a standalone assessment of the bidding entity’s emissions; or an approximation based upon equity share, where emissions are accounted for from operations according to its share of equity in the operation. This model may be helpful where emissions are recorded centrally across a range of entities, e.g. recorded UK wide by the parent company rather than at the bidding entity level.

Where it is not possible to separate out the data for the bidding entity or to accurately approximate its emissions, the bidding entity may submit a CRP covering not only itself but also its parent company, as long as the criteria set out in paragraph 7 of the PPN are met (see also FAQ response below).

13. I am a subsidiary company where carbon data is reported centrally. My parent company has published a CRP which covers the whole organisation. Can I submit that CRP if I do not have one of my own?

In order to ensure the CRP remains relevant, a CRP covering the bidding entity and its parent organisation is only permissible where the detailed requirements of the CRP are met in full, as set out in the Technical Standard[footnote 1] and Guidance[footnote 2], and all of the following criteria are met:

- The bidding entity is wholly owned by the parent;

- The commitment to achieving net zero by 2050 for UK operations is set out in the CRP for the parent and is supported and adopted by the bidding entity, demonstrated by the inclusion in the CRP of a statement that this will apply to the bidding entity;

- The environmental measures set out are stated to be able to be applied by the bidding entity when performing the relevant contract; and

- The CRP is published on the bidding entity’s website.

Bidding entities must take steps to ensure they have their own CRP as soon as reasonably practicable and should note that the ability to rely on a parent organisation’s CRP may only be a temporary measure under this selection criterion.

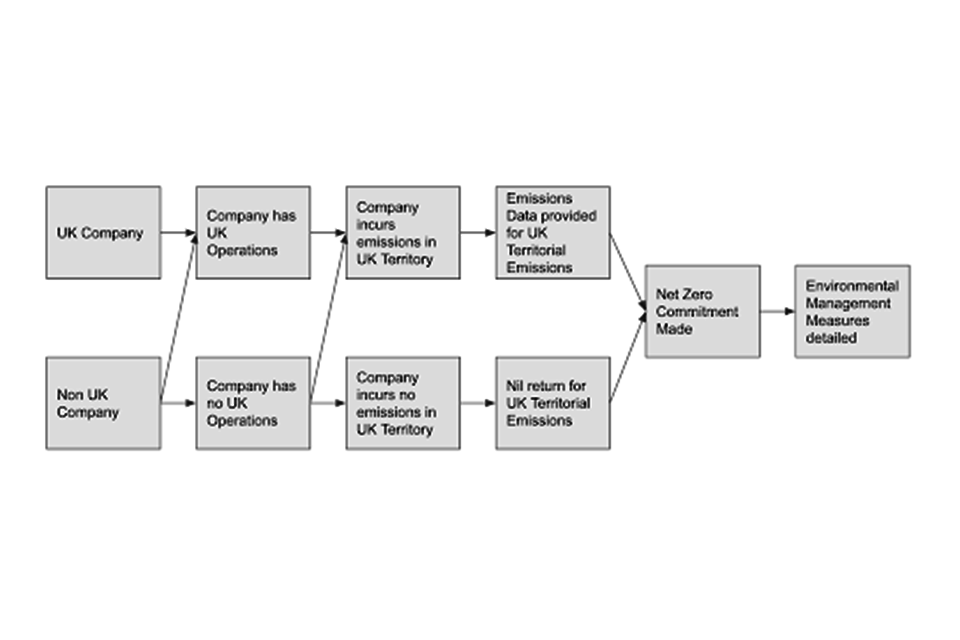

14. How should overseas suppliers account for their emissions?

The measure applies equally to overseas suppliers who are bidding for in-scope procurements. All suppliers are required to produce a CRP, which includes confirmation of their commitment to Net Zero for their UK operations, details of their UK emissions and an indication of the environmental management measures they will be able to apply when performing the contract.

If an overseas supplier does not currently carry-out operations in the UK, and therefore does not have UK emissions data, compliance with the measure can be achieved without this, provided the supplier fulfils the other requirements of the CRP – i.e. by confirming they have made a Net Zero commitment and providing details of environmental management measures in place where they carry-out operations. Examples or information relating to environmental management measures are not required to be based on measures undertaken by the supplier in the UK.

The following flow chart details how suppliers should complete their CRP, in particular their emissions reporting:

Further guidance on selection questions and how to apply them and assess supplier responses can be found in the Guidance on adopting and applying the Carbon Exclusion Measure in the procurement of major contracts

15. How does this measure interact with the Social Value Model?

The two measures are distinct from one another, in that they apply at different points in the procurement process. PPN 06/21 should not be applied as part of the requirements of the Social Value Model, it is a separate measure, and should be applied at the selection stage.

This measure, PPN 06/21 applies at the selection stage of the procurement process. This measure requires bidding suppliers to submit a CRP, containing the required information, and to publish this on their website.

PPN 06/20: Social Value Model is applied at the later award stage. There are five Social Value themes that can be included depending on the nature of the contract. Fighting Climate Change is one theme and, where it is included in the award criteria, Suppliers could be asked to specify what actions they will take to deliver additional environmental benefits through the performance of the specific contract, as opposed to at an organisational level.

More information on the Social Value Model and how it can be used within the procurement process can be found in the Guide to using the Social Value Model[footnote 3].

16. What emissions should be reported in the Carbon Reduction Plan?

The Greenhouse Gas (GHG) Protocol breaks down emissions sources into three categories or ‘Scopes’:

- Scope 1 emissions are direct greenhouse gas emissions that occur from sources that are controlled or owned by the reporting organisation, e.g. emissions associated with fuel combustion in boilers, furnaces, vehicles.

- Scope 2 emissions are indirect greenhouse gas emissions associated with the purchase of electricity, steam, heat, or cooling. They are accounted for by the reporting organisation as they are a result of the organisation’s energy use.

- Scope 3 emissions include all sources not within an organisation’s scope 1 and 2 boundary. Scope 3 emissions often represent the majority of an organisation’s total greenhouse gas emissions.

Scope 3 emissions fall within 15 categories, though organisations may not incur emissions in all categories. Scope 3 emission sources include emissions both upstream and downstream of the organisation’s activities.

When completing your CRP you should include your UK emissions for Scope 1 and Scope 2, along with a subset of five Scope 3 emissions categories:

- Business travel

- Employee commuting

- Waste generated in operations

- Upstream transportation and distribution

- Downstream transportation and distribution.

Full details of the reporting requirements for Carbon Reduction Plans can be found in the Technical standard for Completion of Carbon Reduction Plans

17. Will there be any other training or support that will be given to assist suppliers and commercial teams?

The Cabinet Office is continuing to work alongside partners such as Crown Commercial Service and the Confederation of British Industry to host webinars and round tables on the policy measure from time to time to support implementation.

Further information on supplier webinars hosted by Crown Commercial Service, and other organisations will be made available on their websites.

18. Can in-scope organisations go further than the PPN if desired?

In scope organisations with a more ambitious target for achieving Net Zero may wish to go further than the PPN, however they may not amend the Selection Criteria requirements established by PPN 06/21, or the requirements of the CRP.

Any contract specific requirements may be introduced in the award stage of the procurement and through the use of the Social Value model. Under the Social Value Model, Theme 3: Fighting Climate Change has model award questions, criteria and sub criteria that can be included where relevant to the delivery of the contract and proportionate.

More information on the Social Value model and how it can be used within the procurement process can be found in the Guide to using the Social Value Model (pdf, 279 KB)[footnote 4].

19. What support is available for businesses in calculating their Carbon Footprint?

A number of private sector organisations, charities and industry bodies are able to offer further support and tools for businesses wanting to calculate their carbon footprint. Some of these services are available for free for SME and VCSE suppliers, others may charge. Suppliers should ensure that CRPs produced by third parties on their behalf still meet the requirements of this policy.

20. My organisation has their own target for Net Zero that is earlier than the target established by the Climate Change Act. Am I able to adjust the selection criteria to reflect the earlier Net Zero target date?

We are fully supportive of In-scope organisations having earlier target dates to achieve Net Zero. However, the selection criteria for this PPN should not be amended to a date earlier than 2050. This ensures compliance with the policy, and maintains alignment with the UK’s wider Net Zero commitments as established by the Climate Change Act 2018 (as amended). This ensures a proportionate adoption of the policy, and ensures that the greatest number of suppliers are able to respond to your procurement.

In-scope organisations may wish to consider how they could use other means to support their organisational Net Zero objectives. This could include the use of the Social Value Model or other contract specific evaluation measures to drive specific actions and behaviours from bidding suppliers. This would ensure that the PPN is adhered to, and that there will also be wider considerations for green procurement built into the commercial process.

21. Do Subcontractors need to have a CRP?

A CRP is required from the organisation with whom the In-scope organisations will enter into a contract if it is successful. There is no requirement for subcontractors to produce a CRP in compliance with this policy, save for where subcontracted organisations are also bidding on a procurement in their own right – in these cases, the CRP is required for that separate submission only.

Where the response is being completed on behalf of a consortium of suppliers, a CRP should be completed by each consortium member (see standard selection questionnaire guidance in PPN 08/16 for further guidance on groups of bidders).

In order to gain additional clarity and understanding of their own supply chain emissions, some supplier organisations are establishing their own policies that may request emissions data or a Net Zero commitment. Such requirements are separate from this policy initiative, and any queries should be discussed with the requesting supplier organisation.

22. At what stage in a procurement process will I be asked to provide a CRP?

Suppliers wishing to bid for an in-scope contract are required to submit a CRP at the selection stage of the procurement. Selection questions (as published in the guidance) will be added to the Standard Selection Questionnaire for suppliers to complete. Suppliers will be asked to confirm their Net Zero commitment, and confirm that they have a CRP in place. A link to the CRP will also be requested at the selection stage. If the supplier does not have a website, they must provide a copy of the CRP in writing to the relevant in-scope organisation within 30 days.

The CRP should be updated regularly (at least annually) and published and clearly signposted on the supplier’s UK website.

23. Would a supplier fail the CRP check If their emissions increase?

The provided emissions data is not to be used as a basis for assessment in the procurement process, but may be used to track suppliers’ progress in reducing their emissions over time. An increase in emissions compared to the baseline year or a previous year does not mean that the CRP fails the selection criteria.

Suppliers may wish to provide an explanation for any increase in emissions, and should note that they may need to undertake further action to mitigate their carbon emissions in pursuit of achieving Net Zero by 2050 at the latest. Where a supplier’s emissions footprint is significantly increased as a result of takeovers/buyouts, they may wish to consider re-baselining their emissions.