Single source baseline profit rate, capital servicing rates and funding adjustment methodology - October 2019

Updated 3 October 2019

© Crown copyright 2019

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/ssro-single-source-baseline-profit-rate-methodology-consultation/outcome/single-source-baseline-profit-rate-capital-servicing-rates-and-funding-adjustment-methodology-october-2019

1. Introduction

1.1 Under the Defence Reform Act 2014 (the Act), the Single Source Regulations Office (SSRO) is required annually to review the figures used to determine the contract profit rate for pricing qualifying defence contracts (QDCs) and qualifying sub-contracts (QSCs). Section 19(2) of the Act requires that, for each financial year, the SSRO must provide the Secretary of State with its assessment of the appropriate baseline profit rate, capital servicing rates for fixed capital and working capital, and the SSRO funding adjustment.

1.2 The baseline profit rate is step 1 of the six-step process set out at section 17(2) of the Act and regulation 11 of the Single Source Contract Regulations 2014 (the Regulations) for determining the contract profit rate for a qualifying defence contract. The Act and Regulations do not set out how the baseline profit rate should be calculated, but the SSRO must aim to ensure that good value for money is obtained in government expenditure on qualifying defence contracts, and that persons (other than the Secretary of State) who are parties to qualifying defence contracts are paid a fair and reasonable price under those contracts.

1.3 The capital servicing rates are used in the determination of the baseline profit rate and as part of step 6 of the six-step process set out in the Act and Regulations for determining the contract profit rate for a qualifying defence contract. The Act and Regulations do not set out how the capital servicing rates should be calculated, but the purpose of step 6 is to adjust the contract profit rate so as to ensure that the contractor receives an appropriate and reasonable return on the fixed and working capital employed by the contractor for the purposes of enabling the contractor to perform the contract.

1.4 The SSRO funding adjustment is step 4 of the six-step process set out in the Act and Regulations for determining the contract profit rate for a qualifying defence contract. The Regulations provide that this adjustment shall be a deduction from the price payable under QDCs and QSCs. The explanatory notes to the Act further set out an expectation that the SSRO will be funded equally by the Secretary of State and Industry. Industry funding is intended to be equitably shared across contractors based upon the value of their QDCs.

1.5 The SSRO’s Guidance on the baseline profit rate and its adjustment explains how parties to a QDC or QSC apply these rates when determining the contract profit rate.

1.6 This document sets out the SSRO’s methodology used to calculate the baseline profit rate, capital servicing rates and SSRO funding adjustment for recommendation to the Secretary of State in January 2020.

1.7 The rates, together with the reasons for any difference to the SSRO’s recommendation, must be published by the Secretary of State in accordance with sections 19(4)-(6) of the Act.

2. Key terms and definition

| Activity characterisation | A written description of the group of economic activities and the relevant boundaries which define an activity type. |

|---|---|

| Activity type | A group of economic activities, defined by the SSRO, which correspond to types of activity that contribute to the delivery of QDCs and QSCs. For example ‘Develop and Make’, ‘Provide and Maintain’, ‘Ancillary Services’ or ‘Construction’. |

| Comparability analysis | Transactions carried out by comparable companies are used as a benchmark. |

| Comparability principle | The aim of the baseline profit rate is to provide the starting point in the determination of the contract profit rate (totalling steps one to six). It is set with reference to the returns of companies whose economic activities are included in whole or in part in the activity types that contribute to the delivery of QDCs and QSCs. |

| Comparable company | A company whose economic activities are included, in whole or in part, within an activity type. |

| Comparator group | A group of comparable companies undertaking one or more of the economic activities which make up an activity type. |

| Economic activity | An activity that involves the production, distribution and consumption of goods and services. |

| NACE Rev 2 code | The European Union system of classifying economic activities for the purpose of statistical and other analysis. The SSRO uses NACE codes in conjunction with text search terms to identify comparable companies within the Orbis database. |

| OECD Guidelines | The OECD transfer pricing guidelines for multinational enterprises and tax administrations (2017). This provides guidance on the application of the “arm’s length principle”, which is the international consensus on transfer pricing. |

| Orbis | The database of company-specific information and data supplied by Bureau van Dijk, a Moody’s Analytics company. The SSRO uses this to identify comparable companies and as a source of financial data for those comparable companies for use in the calculation of the baseline profit rate. |

| Text search term | A word or group of words relating to economic activities used to identify comparable companies. For example ‘manufacture’ or ‘production’. The SSRO uses text search terms in conjunction with NACE codes to identify comparable companies within the Orbis database. |

| Underlying profit rate | The median profit level indicator of the comparator group after deducting allowances for the servicing of capital employed. An unadjusted underlying rate can also be calculated using financial data for the comparator companies that is not adjusted for capital servicing. |

3. Baseline profit rate: Key concepts at a glance

Infographic showing principles, automated and manual parts of the baseline profit rate

4. Approach to the baseline profit rate and capital servicing rates

4.1 This section summarises the approach taken in the SSRO’s methodology for calculating the baseline profit rate (BPR) and capital servicing rates (CSRs).

4.2 In overview, the methodology identifies companies whose economic activities are included in whole or in part in the activity types that contribute to the delivery of QDCs and QSCs. These comparable companies form the comparator groups for each activity type.

4.3 The financial data of the comparable companies that form the comparator groups are combined with capital servicing rates derived from relevant bond yields or interest rates to calculate a single underlying profit rate for each activity type. This process is used to calculate four underlying profit rates based on the following activity types:

- Develop and Make (D&M);

- Provide and Maintain (P&M);

- Ancillary Services; and

- Construction.

4.4 Three-year rolling averages of the ‘Develop and Make’ and ‘Provide and Maintain’ underlying profit rates are used as the basis for the composite baseline profit rate that the SSRO recommends to the Secretary of State.

4.5 The methodology adopts a comparable company search process that follows transfer pricing principles to identify comparable companies. The planned lifespan of a comparator group is three years, after which a new search is performed. Annual reviews are undertaken to validate the existing group in the intervening years.

4.6 Transfer pricing is employed extensively by multinational enterprises and tax authorities globally to ensure that companies operating in a number of territories receive appropriate income and profit in each. The UK’s transfer pricing legislation details how transactions between connected parties are handled and, in common with many other countries, is based on the OECD’s internationally-recognised ‘arm’s length principle’, whereby the profit mark-up on transactions between connected entities are benchmarked against comparable transactions between independent entities to ensure that profits are transferred to, and so are taxed in, the appropriate jurisdiction. The OECD’s guidelines and their related expectations and practices are widely known and understood, and their practical implications have been explored.

Box 1: Application of the ‘arm’s length principle’ in taxation

-

Determination of years to be covered.

-

Broad-based analysis of the taxpayer’s circumstances.

-

Understanding the controlled transaction(s) under examination, based in particular on a functional analysis, in order to choose the tested party (where needed), the most appropriate transfer pricing method to the circumstances of the case, the financial indicator to be tested (in the case of a transactional profit method), and to identify the significant comparability factors to be taken into account.

-

Review of existing internal comparables, if any.

-

Determination of available sources of information on external comparables where such external comparables are needed taking into account their relative reliability.

-

Selection of the most appropriate transfer pricing method and, depending on the method, determination of the relevant financial indicator (e.g. determination of the relevant net profit indicator in case of a transactional net margin method).

-

Identification of potential comparables: determining the key characteristics to be met by any uncontrolled transaction in order to be regarded as potentially comparable, based on the relevant factors identified in Step 3 and in accordance with the comparability factors set forth at Section D.1 of Chapter 1.

-

Determination of and making comparability adjustments where appropriate.

-

Interpretation and use of data collected, determination of the arm’s length remuneration.”

OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations (2017), paragraph 3.4

4.7 The application of the arm’s length principle in international taxation is analogous to the SSRO’s requirement to recommend a baseline profit rate, which simulates the outcome of a market process (for example a competitive tender). Box 1 sets out an overview of the application of the arm’s length principle as it would apply in the context of international taxation.

4.8 The principle of the BPR is to ensure that QDC and QSC contractors receive a fair level of profit on contracts, consistent with their functions performed. While this approach is distinct from tax matters, the goal is similar to that of certain transfer pricing methods, which seek to identify an arm’s length profit mark-up by benchmarking returns achieved by comparable companies. Figure 1 illustrates the application of best practice in transfer pricing in the context of the BPR.

4.9 The methodology for calculating the BPR from comparator companies selected using this approach involves:

i. calculating a profit level indicator for each company;

ii. calculating a capital servicing adjustment for each company;

iii. adjusting each company profit level indicator for capital servicing;

iv. removing loss makers in the current year;

v. calculating an underlying profit rate; and

vi. calculating the baseline profit rate.

4.10 The remainder of this document sets out the details relating to the application of each step taken by the SSRO.

Figure 1: Application of best practice approach to transfer pricing

Diagram showing process of transfer pricing

5. Functional analysis

5.1 Steps 3 and 7 in Box 1 are clear that the transactions (or activity) to be tested (in this case QDCs and QSCs) must be understood and the component aspects identified and sought in comparable companies. To do this, the activities to be tested must be characterised.

5.2 In developing these activity characterisations, the SSRO considered the nature of the activities involved in QDCs and QSCs. The SSRO invests time and resources to understand the defence industry as well as the contracts which are reported to it. The organisation does this in a number of different ways:

- It undertakes a regular programme of site visits to defence companies to understand their businesses and the nature of the work involved in QDCs.

- It regularly reviews the MOD’s Defence Contracts Bulletin and the wider defence industry media to identify and understand the type of contracts being awarded.

- It logs queries to the SSRO Support Helpdesk so it can understand the areas where contractors may not be clear about the requirements of the regime and how these apply to individual contracts.

- It provides information on all QDCs to SSRO staff so they can understand at a high level the elements of each contract.

- It attends a range of defence industry events like the DSEI conference, Farnborough Air Show and DPRTE to identify future developments and requirements.

- It has a number of staff who have experience of defence procurement and/or the defence environment. It supplements this through expanding its access to a network of subject matter experts from across the stakeholder community and beyond.

- It speaks with the MOD and industry project teams to understand the complexity involved in defence procurement contracts. 8 It attends training courses delivered by the Defence Academy to understand more about defence procurement.

- It reviews the annual reports and other publicly available information about defence companies to understand past performance, industry health and future priorities.

- It reviews individual company details to confirm whether they are a comparator company in the calculation of the baseline profit rate.

- It learns about each individual contract through the statutory reports it receives and the additional information which is provided by contractors through our engagement with them and their responses to consultations.

- It provides statistical bulletins based on what it learns across contracts on a range of topics, such as pricing methods, and sub-contracting.

5.3 Descriptions of the activities a company is typically expected to undertake to be considered as comparable are at Appendix A.

5.4 These activities are not exclusive to defence contractors. For example, manufacturers of industrial production or agricultural equipment may fall within essentially the same criteria and as such may be considered as potentially comparable manufacturing activities (subject to other considerations such as location).

5.5 The OECD acknowledges that a search focused purely on a product can return limited results, particularly in smaller or niche industries. A broader search also negates potential concerns regarding the influence of government contracting under frameworks, such as the Single Source Contract Regulations themselves, which could be viewed as influencing the results.

5.6 The SSRO has developed these activity characterisations based on the principle that a comparable company is one that undertakes economic activities that are included in whole or in part in the activity types that contribute to the delivery of QDCs and QSCs.

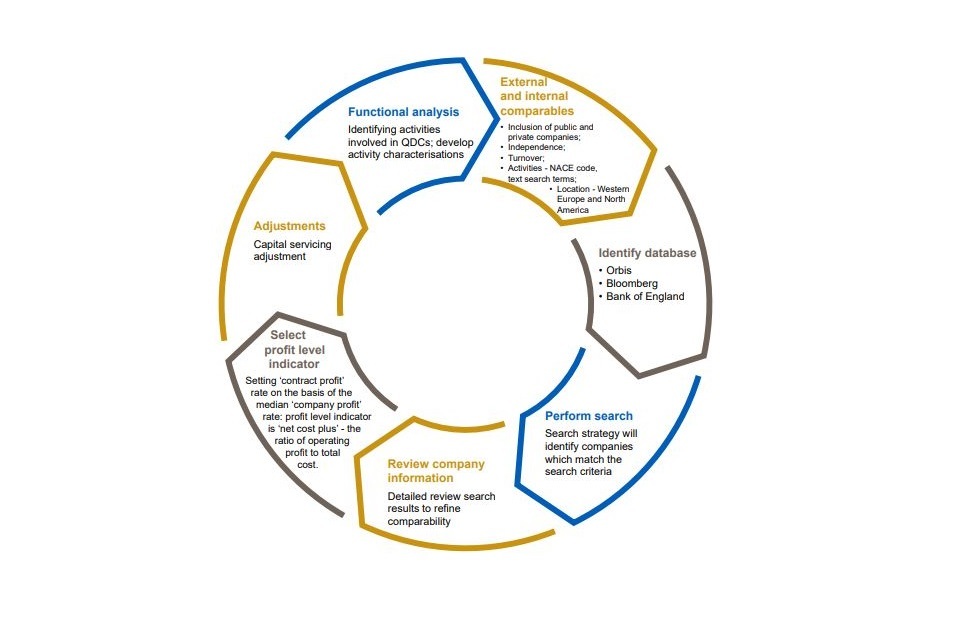

6. Identifying external and internal comparables

6.1 Steps 4 to 7 in Box 1 involve identifying companies that undertake comparable economic activities and transact with enterprises on an independent basis.

6.2 ‘External comparables’ are where companies perform comparable activities, but not for the MOD. ‘Internal comparables’ are where companies perform comparable activities for the MOD, perhaps alongside other business with independent parties.

6.3 Internal comparables will have a close relationship to the transactions involved in a QDC or QSC. However, differences are likely to exist between comparable transactions carried out for the MOD and those with an independent third party due to the characteristics of the UK defence market. Therefore, the SSRO’s approach principally relies on the use of external comparables, which are supplemented by internal comparables.

6.4 The company search process has three stages:

i. The first stage applies tailored search criteria to a database of company information (see section 9). This identifies a range of potential external comparator companies that meet a broad set of comparability criteria.

ii. The second stage is a search for potential internal comparator companies, and to identify those companies also found in the first stage that are internal comparator companies (see section 10).

iii. At the third stage, the potential comparator companies found by the two searches are manually reviewed against detailed activity characterisations to deliver the comparator groups (see section 11).

7. Initial selection and ensuring that data is maintained year-on-year

7.1 The potential external comparator companies are initially the result of a full database search carried out in the first year of the multi-year search cycle. Subsequent annual updates pass the prior year’s final comparator groups through the financial search criteria again but there is no new search against the full database until the next cycle begins.

7.2 A full search for external comparator companies is anticipated to be required every three years. However, the SSRO monitors Orbis on a regular basis and may conduct a refresh earlier than planned should it be observed that the comparator groups are no longer sufficiently representative of the population of companies in the database.

7.3 The search for potential internal comparator companies is carried out every year.

7.4 The detailed review against activity characterisations is carried out every year to ensure that companies remain appropriate comparators to the activities in question. Companies that fail to continue to meet the financial or functional criteria will be removed from the comparator group.

8. Identify database

8.1 To identify comparator companies, comparable transactions between independent parties need to be identified. To achieve this, information from a third-party database is used.

8.2 A third-party database serves three functions in this process:

i. Firstly, it provides the functionality to automatically assess a very large pool of companies against a set of tailored search criteria to identify potential external comparator companies.

ii. Secondly, it provides additional information that assists in a detailed manual review against activity characterisations.

iii. Thirdly, it is the source of company financial information used to calculate the underlying profit rates once the comparator groups have been identified.

8.3 The SSRO uses historical reported data of companies as the basis for benchmarking contract profits. A lack of available contract-level data and the unreliability of forecasts means there is no feasible alternative but to use historical company data to benchmark contract profits.

8.4 A range of publicly-available databases exist which can be used to meet these requirements. The Orbis database provided by Bureau Van Dijk is used by the SSRO. Orbis is a comprehensive, global database containing information on over 300 million public and private companies[footnote 1] . ##9. Perform search for potential external comparators

9.1 Comparable companies are identified by applying the financial and functional search criteria described in this section using data in the most recent year and the four years prior to that.

9.2 The use of multiple-year data is recognised by the OECD guidelines to offer additional insight into factors which may (or should) have influenced the transaction being examined. For example, information on changes in size or loss-making may indicate at what stage a company is in its life cycle.

9.3 Financial results reported in other currencies are converted to GBP using the exchange rates reported on Orbis for each year. The exchange rates used on Orbis come by default from the International Monetary Fund (IMF) website and refer to the closing date of the statement.

Data availability

9.4 Companies are required to have data for their most recent year present in Orbis at the time of the company search.

9.5 The SSRO defines a company’s ‘most recent year’ as its financial year ending during the period from 1 April to 31 March inclusive immediately prior to when the company search is performed.

Active companies

9.6 Companies are only included in the search if they are active trading companies and are not dormant.

Legal form

9.7 Companies are only included in the search if they take on one of the following legal forms:

- Public limited company (PLC, AG, SA, SPS, NV, OYJ, ASA, KK, etc.)

- Private limited company (Ltd, GmbH, SARL, SRL, BV, OY, AS, YK, etc)

9.8 LLPs and partnerships are not included in the search as a result of the potentially incomparable nature of their base costs. For example, payments to partners are classified as “partners’ drawings” or distributions rather than operating costs. As such, costs may be understated compared to the costs of companies that pay and recognise salary costs. The results of LLPs or partnerships could therefore distort the benchmarking results.

Independence

9.9 Companies are only included in the search if they are independent. In order to select only companies that are independent at least one of the following is required:

- The company is classified as ‘A’ independent: has known recorded shareholders, none of which having more than 25% of direct or total ownership; or

- The company is classified as ‘B’ independent: has known recorded shareholders, none of which with an ownership percentage (direct, total or calculated total) over 50%, but having one or more shareholders with an ownership percentage above 25%.

9.10 It is important to identify only those companies that are independent and transact solely with third parties rather than related entities.

Consolidated accounts test

9.11 Companies are only included in the search if their accounts do not include intragroup transactions. Consolidated accounts can be considered to give a fair reflection of arm’s length transactions between the group and third parties (subject to the overall independence of the group).

9.12 Unconsolidated group accounts cannot be relied upon as there is no guarantee that any intragroup transactions are conducted on an arm’s length basis. An exception to this is in cases where a company has subsidiaries that are dormant since there will be no related party trading to consider. Companies with both unconsolidated accounts and subsidiaries are therefore rejected.

Geographic location

9.13 Companies located in the following geographic regions are included in the search:

- Western Europe: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, Netherlands, Malta, Norway, Portugal, Spain, Sweden, Switzerland and the UK

- North America: USA and Canada

9.14 A company’s location is determined by the country of its incorporation (i.e. the place where a company is established and formally registered). A company’s place of incorporation is typically, but not always, the location of its head office and management function.

Data Quality and Company Size

9.15 Companies are only included in the search if their financial data is of sufficient quality, determined by if that company is of a size that would normally require an independent financial audit. This requires companies to have data that demonstrates they meet the following criteria for all of the last five years:

- an annual turnover of more than £10.2 million; and either one of the following:

- total assets worth more than £5.1 million; or

- 50 or more employees on average.

Operating profit (EBIT)

9.16 Companies are excluded that report a negative EBIT in all of the five years. This requires companies to have EBIT data for all years subject to this criteria.

9.17 The OECD Guidelines recognise that an independent enterprise would not tolerate losses indefinitely, but that an associated enterprise may remain in business under these circumstances if it was beneficial to the group as a whole. The SSRO’s analysis uses independent enterprises therefore persistent loss-makers are excluded.

Assets and liabilities data

9.18 Companies must have data for tangible fixed assets, current assets, cash and cash equivalents, current liabilities and short-term debt for the most recent two years available in Orbis. This is to enable the calculation of the Capital Servicing Adjustment (section 13).

Tangible fixed assets

9.19 Companies must have a tangible fixed assets value greater than nil for the most recent two years. This is to reflect the expectation that companies performing comparable activities will be required to own or control assets for use in their commercial activities.

Function

9.20 The SSRO’s activity characterisations are written descriptions of economic activities which correspond to types of activity that contribute to the delivery of QDCs and QSCs.

9.21 Assessment against the activity characterisations is too complex to be solely filtered for automatically. The search criteria are broader than the activity characterisations in order to deliver a pool of potential comparator companies that are manually reviewed in detail (section 11).

9.22 Within Orbis, each company is placed within the industry standard classification system Statistical Classification of Economic Activities in the European Community (NACE)[footnote 2]. A company may have more than one NACE code and the search draws on all codes attributed to a company.

9.23 Within Orbis, each company is provided with a brief trade description, primary business line description and full overview description which indicate their business activities. Keywords are searched for within these fields.

9.24 Tables B1, B2, B3 and B4 in Appendix B present the NACE codes and text search terms used in the search strategy for the activity types of ‘Develop and Make’, ‘Provide and Maintain’, ‘Ancillary Services’ and ‘Construction’.

10. Identify potential internal comparators

10.1 Comparable companies are identified by inspecting Ministry of Defence (MOD) supplier lists to ensure that the MOD’s actual suppliers are represented in the comparator groups, where they meet the other criteria.

10.2 The SSRO inspects statistics published by the MOD and uses the SSRO’s Defence Contract Analysis and Reporting System (DefCARS) data to identify potential additional comparators that are not found through the external comparator’s search process (section 9).

10.3 As with external comparators, only companies that are independent and transact solely with third parties rather than related entities are appropriate. Therefore, where relevant, the SSRO identifies the global ultimate owner (GUO) of the contracting company as the potential internal comparator.

10.4 The potential internal comparators must meet the Orbis search criteria described in Section 9, excluding the ‘function’ criteria. This ensures that comparators meet the necessary financial criteria, but are included for consideration irrespective of how their activities are recorded in Orbis.

11. Review company information

11.1 Information on each potential comparator company resulting from the search for both external comparables (section 9) and for internal comparables (section 10) is reviewed in detail to determine if it can be accepted for entry into a comparator group. This involves assessing if the company’s activities are comparable with those set out in the relevant activity characterisation and if it operates in comparable markets. Descriptions of the activities a company is typically expected to undertake to be considered as comparable are at Appendix A.

11.2 The underlying principle is that an ideal comparable company will undertake those activities that are described in the relevant activity characterisation and the market characterisation.

11.3 In order for a company to be accepted into a comparator group, positive evidence is required that it undertakes comparable activities. If the company does not perform comparable activities, or the review is inconclusive, that company must be rejected. In line with the OECD Guidelines this review follows an iterative process, refining comparability at each stage.

11.4 At the first stage, the Orbis ‘main activity’, ‘primary business line’ and ‘main production sites’ are reviewed. This is used as a triage to reject companies that are non-comparable, for example those identified in the D&M activity type search that focused on sales or advertising. At this stage, companies are only rejected where there is strong positive evidence of non-comparability or where main production sites are located outside of comparable markets.

11.5 Companies not rejected at the first stage are then reviewed in greater detail. Orbis is interrogated to establish the company’s activities and where these take place. A broad range of information is examined, such as the location and activities of any subsidiaries and segmental data. Internet searches are carried out to locate information about the company. Typically, this involves examining the company website and, if required, the company reports. Details of the main subsidiaries of the company are also examined where the company is a group or holding company.

11.6 Where positive evidence of comparability or non-comparability can be established the decision to accept or reject the company is made. Where this does not yield sufficient information, or where the website or company reports are not accessible or could not be translated to determine comparability, the company is rejected.

11.7 The activities undertaken by group companies as a whole are considered rather than just those of the holding company. For example, the holding company of an airline is deemed to have an aviation-related function irrespective of the specific activities of the holding company.

11.8 Decisions are subject to a further round of reviews for quality assurance purposes, including examining the presence or otherwise of the MOD’s suppliers. This entire process is supported by independent transfer pricing experts.

11.9 The outcome of the detailed review is a set of comparable companies from which financial indicators are identified to calculate the underlying profit rates.

12. Select profit level indicator

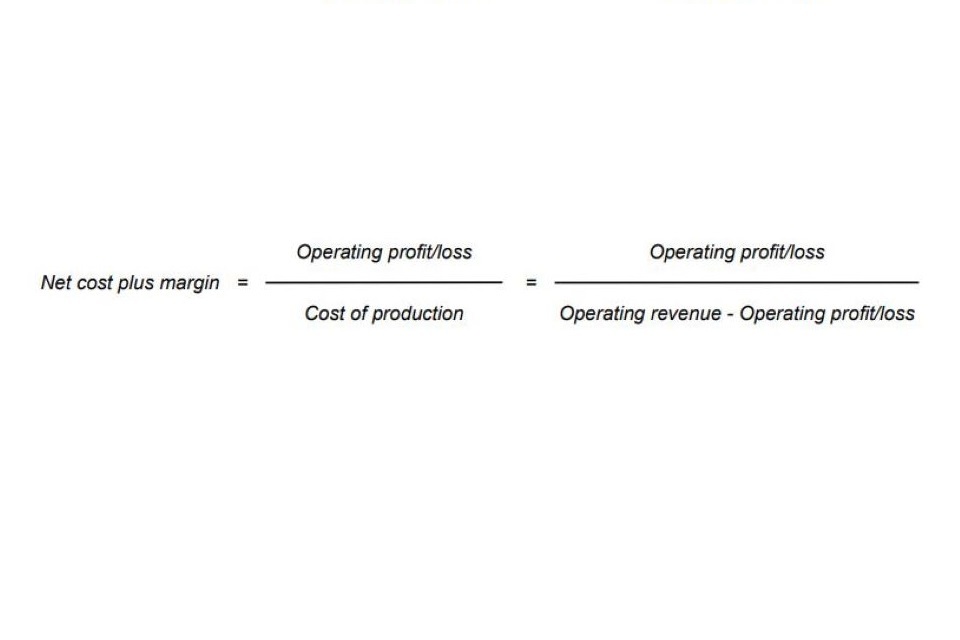

12.1 To determine the underlying profit rate for each activity type, an appropriate profit level indicator (PLI) must be used. A PLI refers to the margin or measure used relative to an appropriate base (for example costs, sales or assets) that is realised from a transaction.

12.2 The net cost plus margin (also known as return on cost of production) is the PLI used by the SSRO. It is the closest equivalent measure of return on Allowable Costs used to determine the contract profit rate of QDCs and QSCs. The SSRO uses earnings before interest and tax (EBIT) as the measure of the return a company makes on its core operations. It excludes the impact of tax, financing structures, and some other income or expenses. EBIT includes depreciation and amortisation which contractors may be reimbursed for through Allowable Costs on a contract-by-contract basis (where these pass the relevant tests). This maintains consistency with the approach to Allowable Costs[footnote 3]

12.3 The PLI is calculated as:

Formula: Net cost plus margin = operating profit/loss divided by cost of production = Operating profit/loss divided by Operating revenue minus operating profit/loss

13. Adjustments

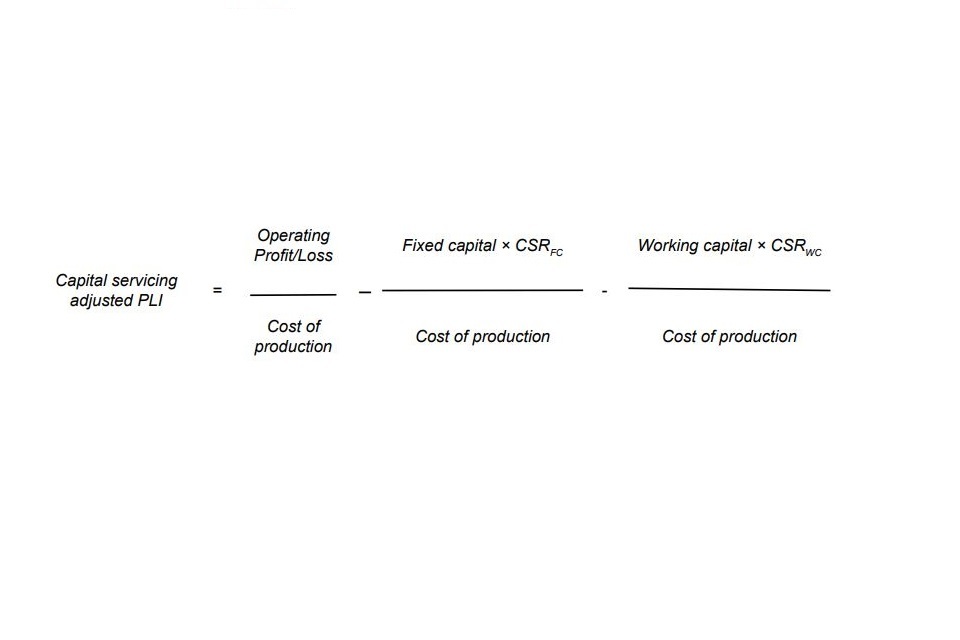

13.1 Section 17(2) of the Act, and Regulation 11(7), set out the requirement for the capital servicing adjustment at ‘step 6’: “Take the amount resulting from step 5 and add to or subtract from it an agreed amount (“the capital servicing adjustment”), so as to ensure that the primary contractor receives an appropriate and reasonable return on the fixed and working capital employed by the primary contractor for the purposes of enabling the primary contractor to perform the contract.”

13.2 The PLI of each comparator company is adjusted with respect to capital employed to set a baseline upon which ‘step 6’ can be added. The approach of the SSRO is to adjust the PLI in proportion to the ratio of fixed and working capital employed by each comparator company. This is the reverse of the approach taken at ‘step 6’ in calculating the capital servicing adjustment set out in Guidance on the baseline profit rate and its adjustment.

13.3 The SSRO makes a capital servicing adjustment to take into account the different levels of fixed capital and working capital employed by the companies in the comparator group. This adjustment acts to ameliorate the effects of extreme outliers in the data and is considered by the SSRO to enhance comparability which is consistent with OECD Guidelines.

13.4 The capital servicing adjusted profit level indicator is calculated according to the following:

Formula: Capital servicing adjusted PLI = Operating Profit/Loss divided by Cost of production minus Fixed capital × CSRFC divided by Cost of production minus Working capital × CSRWC divided by Cost of production

13.5 CSRFC and CSRWC are the capital serving rates for fixed capital and working capital respectively. The SSRO calculates the capital servicing rates for:

- fixed capital;

- positive working capital; and

- negative working capital.

13.6 The figures for fixed and working capital are the average of the opening and closing balances for the most recent year of the company whose PLI is being adjusted. The definitions of each balance sheet item, the relevant Orbis data fields and a detailed breakdown of the calculation of the capital servicing adjusted PLI is at Appendix C.

13.7 The capital servicing rates that apply at this stage are the same as those recommended to the Secretary of State for application at ‘step 6’ in the calculation of the contract profit rate. This ensures that contractors are not disadvantaged should the aggregate credit rating of the comparator groups differ from their own.

13.8 Bloomberg and the Bank of England are the sources of data for the capital servicing rates.

Fixed capital servicing rate

13.9 The fixed capital servicing rates use the C40515Y Bloomberg index for 15 year BBB rated daily yields of sterling denominated corporate bonds. The time period is seven years up to and including data available at 30 November in the year immediately prior to that in which the rate being calculated applies.

13.10 The ‘Yellow Book’ regime’s methodology used a BBB- credit rating approximated by a BBB interest rate plus an additional 0.5 percentage points applied. To reflect this legacy issue, the 0.5 percentage point adjustment is applied to all data points up to and including 31 December 2014.

13.11 The fixed capital servicing rate is calculated as the mean average of the seven years of daily data.

Positive working capital servicing rate

13.12 The positive working capital servicing rate is calculated using Bloomberg data for one year BBB rated sterling denominated corporate bonds yields (C4051Y index). The time period is three years up to and including data available at 30 November in the year immediately prior to that in which the rate being calculated applies.

13.13 The positive working capital servicing rate is calculated as the mean average of the three years of daily data.

Negative working capital servicing rate

13.14 The negative working capital servicing rate is calculated using Bank of England data on monthly interest for short term deposits (CFMBI32 index)[footnote 4]. The time period is three years up to and including data available at 30 November in the year immediately prior to that in which the rate being calculated applies.

13.15 The negative working capital servicing rate is calculated as the mean average of the three years of monthly data.

14. Calculating the underlying profit rates and composite baseline profit rate

14.1 Companies that made a loss in the most recent year, determined by a negative capital servicing adjusted PLI, are excluded from this calculation. Loss-making companies are removed to reflect the expectation of positive profit on estimated Allowable Costs in QDCs. This maintains consistency with the construct of the profit formula as a mark-up on estimated Allowable Costs and removes the possibility of a negative BPR being produced.

14.2 The underlying profit rate of each activity group for the current year is calculated using the median of comparator company data. The choice of average should reflect the specific characteristics of the data set and the median is a superior measure of central tendency compared to the mean or weighted mean, given the SSRO places no upper limit on the profit level or size of comparator companies.

14.3 The three-year mean averages of the underlying profit rate for the current year and those of the two immediately preceding years are calculated. The SSRO does not reassess previous year’s underlying rates for the current year.

14.4 The mean average of the resulting rates for ‘Develop and Make’ and Provide and Maintain’ is the composite baseline profit rate that the SSRO recommends to the Secretary of State.

The SSRO funding adjustment

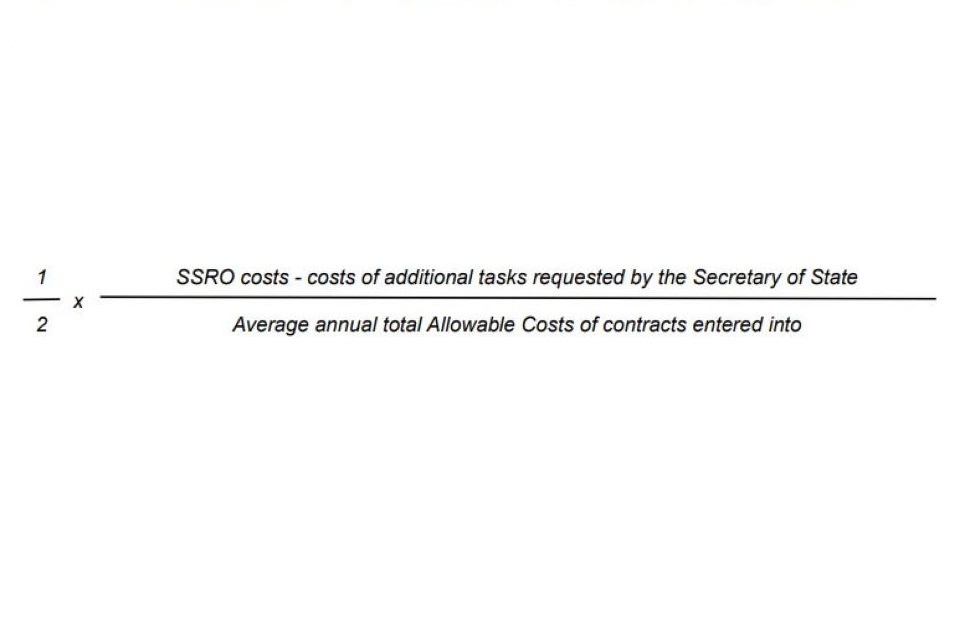

1. The calculation of the SSRO funding adjustment

1.1 The method to calculate the funding adjustment calculation is intended to set it at a level that allows the MOD to recover half of the SSRO’s costs through a reduction in the amounts paid on single source contracts, shared across contractors based upon the value of their QDCs and QSCs.

1.2 The SSRO funding adjustment is calculated as:

Formula: 1/2 x SSRO costs - costs of additional tasks requested by the Secretary of State divided by Average annual total Allowable Costs of contracts entered into

1.3 The SSRO’s costs, and the costs of additional tasks requested by the Secretary of State, are the mean averages of the three full financial years preceding the year of the recommendation.

1.4 Where the SSRO’s audited financial information is not yet available for three years, the funding adjustment will be based on the latest years that are available.

1.5 The average annual total Allowable Costs of contracts entered in to will be a mean average of the annual sum of the Total Allowable Costs (including any Risk Contingency Allowance) values reported in latest available report for all QDCs entered in to in each of the three preceding financial years. Where contract amendments are made the most recently reported values will be used but each contract will be included only once in the calculation.

1.6 QDC data will be drawn for the periods which align to that used for SSRO running costs, based on the most recently available published statistics at the time of calculation.

2. Data sources and adjustments

2.1 All SSRO costs, including referrals and one-off items, will be included unless specifically incurred as a result of a request for additional work by the Secretary of State. The partyear costs incurred during the set-up year (2014/15) and costs incurred by the MOD in establishing the SSRO were not included.

2.2 The SSRO costs and the costs of additional tasks requested by the Secretary of State will be drawn from the audited financial statements in the preceding three financial years. The costs are drawn from the Statement of Comprehensive Net Expenditure – Net Expenditure. This means capital expenditure is accounted for via depreciation rather than in cash terms (the SSRO is funded and pays for capital expenditure as it is incurred).

2.3 The QDCs’ data used to calculate the SSRO funding adjustment comes from the latest Quarterly qualifying defence contracts statistics. The total value of QDCs is based on:

- Data for any contract which became a QDC between 1 April and 31 March of a given financial year

- The total Allowable Costs (including any Risk Contingency Allowance) reported in the latest available report as of the date of extraction.

Appendix A – Activity characterisations

1. Market characterisation

1.1 Companies undertaking comparable activities in any activity group are expected to operate in markets that would typically include Western Europe and North America.

1.2 Where a company undertakes global operations consideration should be given to the nature of the activities occurring in different geographic areas. The comparable activities of the business are expected to meet the relevant activity characterisation and be undertaken in comparable geographic areas.

1.3 The determination of where a company’s activities are undertaken might be by reference to the amount of cost incurred, the number of employees, the value of assets employed, or other measures depending on the nature of the activities undertaken.

1.4 It may be acceptable for comparable firms to undertake some activities in non-comparable geographic areas. However, these activities are not expected to extend beyond what might reasonably be required to deliver the company’s principle business.

1.5 The end customers for the outputs generated by comparable companies may be located in any geographic area. For example, a company that exports goods or services from a comparable market to a non-comparable market is unlikely to be excluded on that basis.

2. Develop and make

2.1 Companies undertaking comparable activities considered as ‘Develop and Make’ are expected to engage in manufacturing and the design and development contributing to that process. This would therefore not include manufacturing on behalf of a hiring firm that supplies the design, or those solely undertaking research or design work with no associated manufacturing. Where development activities do not seek to result in a novel or differentiated product the company is less likely to be considered comparable.

2.2 Comparable activities would typically be of the type that can be likened to those involved in producing equipment used for military or defence purposes. This would include scientific or technical research, design, development or testing activities leading to the production of selfcontained sub-systems or finished goods. To the extent that a product is being assembled or constructed then it is likely to represent comparable manufacturing. This could cover a broad range of products such as structural metal goods, machinery, electronic and mechanical subsystems, vessels, containers, general machinery, ships, aircraft, and wheeled or tracked vehicles or other means of transportation and other items of machinery of an industrial nature. If the product is a commoditised unit or processed raw manufacturing input, for example a generic electrical or mechanical components, sheet metal, shaped plastic, ancillary items such as basic tools, then this may not be sufficiently complex and is likely to be excluded. Electronic or mechanical assemblies or subsystems that are complex and not of a commoditised nature are more likely to be considered the output of a comparable manufacturing process.

2.3 The value added, cost base or profits of the business are expected to principally derive from the manufacturing, design and development activities as described above. For example comparable firms would not be expected to derive the majority of their value added through the purchase of raw materials, luxury branding, the exploitation of patents and copyrights or distribution activities. It may be acceptable for comparable firms to engage in some loosely associated activities as part of delivering core comparable business (for example the procurement of inputs and the distribution and marketing of final goods). However these activities are not expected to extend beyond what might reasonably be required to deliver the company’s principal business. Significant involvement in activities that are obviously non-comparable in nature (for example provision of financial services, marketing or food processing) would be cause to reject a company.

2.4 The end customers for the outputs generated by comparable companies are expected to be other businesses, institutions or governments. Comparable companies are not expected to maintain marketing models, sales operations, large networks of product outlets or dealerships aimed at the general public.

3. Provide and maintain

3.1 Companies undertaking comparable activities considered as ‘Provide and Maintain’ are expected to deliver services to ensure the availability of an asset either through repair and servicing to third party equipment, or through hire or lease arrangements that include associated upkeep and maintenance services.

3.2 Comparable activities would typically be of the type which can be likened to those involved in the support and provision of equipment used for military or defence purposes. This could cover a broad range of products such as structural metal goods, machinery, electronic and mechanical subsystems, vessels, containers, general machinery, ships, aircraft, and wheeled or tracked vehicles or other means of transportation and other items of machinery of an industrial nature. Comparable companies may also provide the facilities embodying or integrating the equipment and the training necessary to operate or maintain these assets.

3.3 Repair and servicing activities include arrangements where spares and labour are charged for as they are required, or may include these costs as part of a longer term contracting arrangement. Diagnosis, repair and installation activities would be expected to require an in-depth knowledge of the asset being serviced. This would exclude companies whose capabilities are limited to rudimentary work, such as those involving user-serviceable parts or domestic installations (for example domestic white goods). Hire and leasing arrangements should be focused on items of an industrial or commercial nature.

3.4 The value added, cost base or profits of the business are expected to principally derive from the asset provision and maintenance activities described above. For example, the provision of aftersales service to products that a company manufactures or sells would be insufficient to consider a company to be comparable. Companies are unlikely to be comparable if they include a significant consumer-targeted sales and marketing model or the sale of associated finance products (for example in the case of consumer automotive sales). It may be acceptable for comparable firms to engage in some loosely comparable activities as part of normal business (for example parts procurement, warehousing, logistics, installation, or the sale of the company’s ex-hire fleet). However these activities are not expected to extend beyond what might reasonably be required to deliver the company’s principle business. Significant involvement in activities which are obviously non-comparable in nature (for example manufacturing or distribution) is grounds for rejection.

3.5 The end customers for the services provided by comparable companies are expected to be businesses, institutions or governments. Comparable companies are not expected to maintain significant marketing models or sales operations in relation to the goods they service, or large networks of service outlets or dealerships aimed at the general public.

4. Ancillary services

4.1 Companies undertaking comparable activities considered as ‘Ancillary Services’ are expected to deliver either one of administrative, facilities or IT support activities. Companies undertaking these support services are not expected to bear any significant risks other than that of failing to provide the contracted outputs. This captures risk in relation to the delivery of the services, contract risk, procurement risk, staff risk and some quality control risk in respect of these activities.

4.2 Administrative support relates to outsourced business services such as payroll processing, call centres, HR, basic book-keeping, routine tax or legal advice and other clerical work. IT support services would include data management, data processing, network hosting, IT repairs and maintenance and IT security services. Facilities support services would include property cleaning, property repairs and maintenance, canteen services, laundry, gardening and general guarding and security services.

4.3 The value added, cost base or profits of the business are expected to principally derive from the Ancillary Services activities described above. Companies that engage in support services loosely connected to those described above, but which are of a specialised nature would not typically be considered comparable. Such non-comparable services would include provision of security services in prisons, the design and procurement of IT infrastructure, the services of chartered professionals, or the supply of clinical staff to hospitals. Companies that do not undertake activities akin to ancillary support services (for example recruitment, construction, software development, management consultancy, engineering consultancy) are not considered comparable.

4.4 The end customers for the services provided by comparable companies are expected to be other businesses, institutions or governments. Comparable companies are not expected to be entities which solely exist to provide these services to members of their own corporate group. Comparable companies are not expected to primarily serve the general public with, for example, domestic gardening or cleaning services.

5. Construction

5.1 Companies undertaking comparable activities considered as ‘Construction’ are expected to deliver services in relation to the construction of buildings or other structures at fixed locations. Companies could provide such services either on a contract basis with designs and specifications received or using their own designs. Comparable companies may be responsible for the management of the construction project, and are likely to bear contract risk, procurement risk, staff risk and some quality control risk in respect of these activities. They are not expected to bear any significant property price risk in respect of these activities.

5.2 Buildings would include industrial buildings such as factories, warehouses, plants, and public, commercial or residential buildings of steel-frame or concrete construction (not individual houses) and may include the associated design services. Civil engineering works in the form of the erection of structures in a fixed location, for example in metal and concrete, would also be considered comparable. To the extent that civil engineering works relates to the assembly of a structure at a fixed location then it is more likely to be considered as ‘Construction’. To the extent that companies engage in tunnelling, pipe-laying, highways maintenance or river and coastal work, these activities are not expected to extend beyond what might reasonably be required to support the delivery of a structure. Speciality trade contractors, such as outfit contracting services (plumbing, ventilation, electrical installation and windows) must be demonstrably of an industrial nature and be active in the construction of the building.

5.3 The value added, cost base or profits of the business are expected to principally derive from the construction activities described above. Comparable companies are not expected to hold land for long-term appreciation purposes and as such those who engage primarily in real estate development would typically be excluded. It may be acceptable for comparable companies to engage in some loosely comparable activities in the delivery of their core construction work (for example manufacturing or procurement of construction inputs, earthworks, provision of construction labour, building preservation, site clearance and recycling of reclaimed items from demolition). However these activities should not be the focus of their business. Significant involvement in activities which are obviously noncomparable in nature (for example toll-road operation, property investment, interior design services) is grounds for rejection.

5.4 The end customers for the services provided by comparable companies are expected to be other businesses, institutions or governments. Comparable companies are not expected to primarily serve the general public and as such domestic building services, roofing, flooring and general building maintenance contractors would not be considered comparable.

Appendix B – Industry codes and text search terms used in activity type search strategies

1. Develop and make

1.1 The ‘Develop and Make’ activity type NACE Rev 2 codes were selected as they were considered to be the most appropriate given the activity characterisation.

1.2 Companies are selected as potential ‘Develop and Make’ activity type comparators if they have:

-

at least one manufacturing sub-activity NACE Rev 2 code AND at least one manufacturing sub-activity text search term in either their trade description or primary business line description or full overview description; OR

-

at least one R&D NACE Rev 2 code AND at least one text search term from each of the two R&D sub-activity text search terms groups in either their trade description or primary business line description or full overview description.

Table B1: The ‘Develop and Make’ activity type NACE Rev 2 codes and text search terms

| Sub-activity | NACE Rev 2 code | Description | Text search terms |

|---|---|---|---|

| Manufacturing | 2511 | Manufacture of metal structures and parts of structures | (manuf *, produc *, fabric *, build *, defense *, defence *, militar *) |

| 2529 | Manufacture of other tanks, reservoirs and containers of metal | ||

| 253 | Manufacture of steam generators, except central heating hot water boilers | ||

| 254 | Manufacture of weapons and ammunition | ||

| 2599 | Manufacture of other fabricated metal products n.e.c. | ||

| 2630 | Manufacture of communication equipment | ||

| 2651 | Manufacture of instruments and appliances for measuring, testing and navigation | ||

| 28 | Manufacture of machinery and equipment nec | ||

| 29 | Manufacture of motor vehicles, trailers and semi-trailers | ||

| 301 | Building of ships and boats | ||

| 302 | Manufacture of railway locomotives and rolling stock | ||

| 303 | Manufacture of air and spacecraft and related machinery | ||

| 304 | Manufacture of military fighting vehicles | ||

| 3099 | Manufacture of other transport equipment n.e.c. | ||

| Research and development (R&D) | 749 | Other professional, scientific and technical activities nec | (research *, develop *, design *) AND (test *, equip *, machin *, militar *, vehic *, defense *, defence *) |

| 749 | Other professional, scientific and technical activities nec | ||

| 721 | Research and experimental development on natural sciences and engineering | ||

| 741 | Specialised design activities | ||

| 712 | Technical testing and analysis |

*denotes a part word. For example, “develop *” includes “develop”, “develops”, “developed”, “developing”, “developer” and “development”.

2. Provide and maintain

2.1 The ‘Provide and Maintain’ activity type NACE Rev 2 codes were selected as they were considered to be the most appropriate given the activity characterisation.

2.2 Companies are selected as potential ‘Provide and Maintain’ activity type comparators if they have

- at least one capacity provisioning sub-activity NACE Rev 2 code;

OR

- at least one text search term from each of the two capacity provisioning sub-activity text search terms groups in either their trade description or primary business line description or full overview description;

OR

- at least one upkeep and maintenance sub-activity NACE Rev 2 code;

OR

- at least one text search term from each of the two upkeep and maintenance sub-activity text search terms groups in either their trade description or primary business line description or full overview description.

Table B2 - The ‘Provide and Maintain’ activity type NACE Rev 2 codes and text search terms

| Subactivity | NACE Rev 2 code | Description | Text search terms |

|---|---|---|---|

| Capacity provisioning | 7735 | Renting and leasing of air transport equipment | (rent , leas *, hir) AND (container *, truck *, tank *, trailer *, aircr *, aviation *, industrial *, defence *, defense *, militar *) |

| 7739 | Renting and leasing of other machinery, equipment and tangible goods nec | ||

| 7712 | Renting and leasing of trucks | ||

| 7732 | Renting and leasing of construction and civil engineering machinery and equipment | ||

| 7734 | Renting and leasing of water transport equipment | ||

| Upkeep and maintenance | 33 | Repair and installation of machinery and equipment | (repair *, maint *, upkeep *, update *, training *) AND (equip *, vehic *, aircr *, defense *, defence *, militar *) |

3. Ancillary services

3.1 The ‘Ancillary Services’ activity type NACE Rev 2 codes were selected as they were considered to be the most appropriate given the activity characterisation.

3.2 Companies are selected as potential ‘Ancillary Services’ activity type comparators if they have:

- at least one of the ‘Ancillary Services’ NACE Rev 2 code;

AND

- either their trade description or primary business line description or full overview description contained at least one ‘Ancillary Services’ text search terms from each of the two sets of the text search terms.

Table B3: The ‘Ancillary Services’ activity type NACE Rev 2 codes and text search terms

| NACE Rev 2 code | Description | Text search terms |

|---|---|---|

| 6311 | Data processing, hosting and related activities | (outsourc *, support *, maint *) AND (clean *, maint * facil *, industr *, upkeep *) cleric *, IT! , office *, data *, admin *, defence *, defense *, militar *) |

| 811 | Combined facilities support activities | |

| 8121 | General cleaning of buildings | |

| 8122 | Other building and industrial cleaning activities | |

| 8129 | Other cleaning activities | |

| 821 | Office administrative and support activities | |

| 8299 | Other business support service activities n.e.c. | |

| 802 | Security systems service activities |

! denotes where the search is case-sensitive.

4. Construction

4.1 The ‘Construction’ activity NACE Rev 2 codes were selected as they were considered to be the most appropriate given the activity characterisation.

4.2 Companies are selected as potential ‘Construction’ activity type comparators if they have:

- at least one ‘Construction’ activity NACE Rev 2 code;

AND

- at least one ‘Construction’ activity text search term in either their trade description or primary business line description or full overview description.

Table B4: The ‘Construction’ activity type NACE Rev 2 codes and text search terms

| NACE Rev 2 code | Description | Text search terms |

|---|---|---|

| 41 | Construction of buildings | (construct *, build *, engineer *, architect *, defense *, defence *, militar *) |

| 42 | Civil engineering | |

| 43 | Specialised construction activity |

Appendix C – Orbis data fields and calculation steps for the underlying profit rates

1. Data fields

1.1 The following data is downloaded from Orbis to calculate the baseline profit rate:

- OPPL: Operating P/L [=EBIT] – the most recent year

- OPRE: Operating revenue (Turnover) – the most recent year

- TFAS: Tangible Fixed Assets – the two most recent years

- CUAS: Current Assets – the two most recent years

- CULI: Current Liabilities – the two most recent years

- CASH: Cash and Cash Equivalent – the two most recent years

- LOAN: Loans – the two most recent years

2. Calculation steps

| Step indicator | Financial indicator | Data source/calculation |

|---|---|---|

| A | Operating revenue (turnover) | Orbis data [Orbis code OPRE] |

| B | Operating profit (EBIT) | Orbis data [Orbis code OPPL] |

| C | Cost of production | A - B |

| D | Profit level indicator (net cost plus) [percentage] | B / C |

| E | Fixed capital (the two year average) | Orbis data - ‘Tangible Fixed Assets’ [TFAS] |

| F | Working capital (the two year average) | Orbis data – current assets [CUAS] - cash [CASH] - current liabilities [CULI] + shortterm debt [LOAN] |

| G | Capital employed (average) | E + F |

| H | Positive working capital | F (when F is positive) |

| I | Negative working capital | F (when F is negative) |

| J | Cost of production: capital employed ratio | C / G |

| K | Fixed capital ratio | E / G |

| L | Positive working capital ratio | H / G |

| M | Negative working capital ratio | I / G |

| N | Fixed capital servicing rate [percentage] | Bloomberg data – 7-year average of C40515Y INDEX |

| O | Positive working capital servicing rate [percentage] | Bloomberg data – 3-year daily rates’ average of C4051Y INDEX |

| P | Negative working capital servicing rate [percentage] | 3-year monthly rates’ average of Bank of England statistics on monthly interests for short term deposits [CFMB132] |

| Q | Fixed capital servicing allowance | K x N |

| R | Positive working capital servicing allowance | L x O |

| S | Negative working capital servicing allowance | M x P |

| T | Capital servicing rate | Q + R + S |

| U | Capital servicing adjustment [percentage] | T / J |

| V | Capital servicing adjusted PLI [percentage] | D - U |

-

As of September 2019. ↩

-

The current version is revision 2 and was established by Regulation (EC) No 1893/2006 ↩

-

SSRO, Allowable Costs guidance (2019) ↩

-

Monthly average of UK resident monetary financial institutions’ (excl. Central Bank) sterling weighted average interest rate - time deposits with fixed original maturity <=1 year from private non-financial corporations (in percent) not seasonally adjusted. ↩