Measuring the economic value of museums and galleries digital offers: an exploratory use of contingent valuation techniques

Published 28 June 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/measuring-the-value-of-the-digital-offer-of-galleries-and-museums/measuring-the-economic-value-of-museums-and-galleries-digital-offers-an-exploratory-use-of-contingent-valuation-techniques

Authors and acknowledgements:

Simetrica Jacobs and Creative Industries Policy Evidence Centre: Dr Madeleine Arber, Hasan Bakhshi, Hazel Cranmer, John Davies, Dr Daniel Fujiwara, Daria Incarnato, Augustin Lagarde, Dr Ricky Lawton and Peter O’Donovan

1. Executive summary

As part of its programme of research on how arts and cultural organisations can use economic valuation techniques to better demonstrate their social and cultural value to the wider public, Arts Council England (ACE) has recognised a need to explore their applicability to digital culture, such as the online content offered by cultural institutions on their websites. This timely research comes as the public’s behavioural engagement with culture has shifted in the face of the coronavirus (COVID-19) pandemic.[footnote 1] For this report, ‘digital offer’, or ‘digital content’, is defined as any online content offered by art galleries and museums specifically, which may include audio and visual imagery, games, videos, social media posts and more. Primary research was conducted to estimate the value the digital offer of art galleries and museums in England, using the same economic valuation techniques that the authors have applied for Arts Council England to the traditional ‘offline’ offer, or the in-person experience, of a variety of cultural institutions.[footnote 2]

The authors understand that the research in the economic valuation of digital offering is still in its infancy. The research undertaken in this report is therefore exploratory. In particular, it seeks to establish whether a contingent valuation methodology can be implemented, acknowledging that other approaches such as the price sensitivity meter[footnote 3] or time use[footnote 4] may also provide monetary estimates of the benefits to users derived from the digital offers of museums and art galleries in England. The research undertaken in this report uses methods that are consistent with HM Treasury Green Book (2022) guidance on Social Cost Benefit Analysis (SCBA). It explores the applicability of these methods to digital offers, and thereby adds to the growing body of evidence on the value of cultural institutions. It also contributes to the Culture and Heritage Capital (CHC) Programme launched by the Department for Digital, Culture, Media and Sport (DCMS) in January 2021 which aims to put public investment in culture and heritage on more rigorous footing.[footnote 5] ACE and DCMS aim to create publicly available statistics and guidance that will allow for improved articulation of the value of the culture and heritage sectors in decision-making. The valuation of benefits and costs plays an important role in deciding how the government should spend taxpayers’ money.

There is increasing recognition of the benefits of applying HM Treasury Green Book (2022) endorsed techniques from welfare economics to value the non-market as well as market benefits of culture and heritage.[footnote 6] The outputs of the CHC Programme will not only be applicable to publicly funded organisations but will also be useful resources for assessing the public benefit of private assets. Therefore, the CHC Programme should be of interest to any cultural or heritage institution that wants to measure the benefits it bestows on society. Alongside the research reports, ACE has published a series of guidance documents to help organisations in different sectors apply the value estimates.[footnote 7]

Millions of people each year access the digital offer of England’s art galleries and museums. Even more so than for their traditional in-person offering, the majority of these digital offers are free of charge. Partly for this reason, users of these ‘intangible’ services may struggle to estimate a clear monetary measure of their value in their minds. Even if the gallery or museum has a paid membership scheme, it is not at all clear the extent to which the members are willing to pay in any way reflects the benefits they may derive from the gallery or museum’s digital offer (Noehrer, Gilmore, Jay and Yehudi, 2021).

As such, estimates of the value to the public of the digital offering of arts and cultural organisations are necessarily more tentative than for estimates of their traditional offline offers. In this study, users were asked about their willingness to pay (WTP) having first interacted with online content from four galleries/museums based in England.

The survey was designed for each of the following four sites in question:

-

The Derby Museum and Art Gallery.

-

The Bristol Museum and Art Gallery.

-

The Foundling Museum.

-

The Great North Museum.

Fieldwork was conducted between 22 June to 3 September 2021 whereby respondents were asked to complete the survey questionnaire. Initial survey questions asked respondents about their attitudes to culture, their previous visits to museums within the past three years, and their experiences of engaging with culture online. After asking respondents their WTP, questions were then asked to determine the motivation behind their responses, whether the respondents felt that the COVID-19 pandemic had impacted on their access to and consumption of digital content and their WTP for it, and lastly to gather standard demographic information. A monthly subscription fee payment vehicle was chosen to elicit respondents’ WTP. The respondent sample was made up of repeat users (i.e., those who had used the website before) and first-time users (i.e., those who had not). As a result, non-use values were not able to be collected as all survey respondents had engaged with the digital offer when answering the questions. Each person surveyed gave an individual maximum WTP for the site in question, providing a range of WTP values across the sample, including for those people who indicated that they would not be prepared to pay anything at all (i.e., had a WTP value of £0). An average WTP value was calculated for each site.

The main research findings are as follows:

The WTP a monthly subscription fee for a household to continue accessing the digital offer and supporting in offering digital content ranged from £3.27 for the Derby Museum and Art Gallery to £4.93 for the Foundling Museum. This is slightly lower than what respondents were willing to pay to physically visit an art gallery (£5.40).[footnote 8]

The WTP for a household to access the site’s digital offer was positively associated with some socio-demographic factors and cultural engagement history. Specifically, household income was found to be positively and significantly associated with WTP a monthly subscription fee for their household’s access to the digital offer for users who had physically visited or digitally accessed the good prior to the study (Foundling Museum, Great North Museum and Pooled Museum models). The authors have found similar validity testing results with respect to the WTP for in-person experience for art galleries and local museums, whereby WTP is significantly and positively associated with household income and cultural engagement history.[footnote 9] In respect to in-person visits to local museums, the authors only found the higher income bracket to be significantly associated with an increase in WTP an entry fee.

| Derby Museum and Art Gallery | Bristol Museum and Art Gallery | Foundling Museum | Great North Museum |

|---|---|---|---|

| £3.27 | £4.37 | £4.93 | £3.92 |

The WTP estimates were statistically robust: the distribution of the 95% confidence intervals for the average WTP per site was not wide:

- Derby Museum and Art Gallery: £2.64 - £3.89

- Bristol Museum and Art Gallery: £3.35 - £5.39

- Foundling Museum: £3.68 - £6.17

- Great North Museum: £2.34 - £5.51

This finding is in line with the authors’ previous findings with respect to in-person visits to galleries and local museums. However, we must heavily caveat the estimates for reasons of survey design, the uncertainty in users’ minds about their valuations, and the heterogeneity of the digital offer across the four sites studied. We detail these caveats in the report.

Analysis of respondents’ answers suggests that users do not think that the digital offering of galleries and museums will replace the in-person experience any time soon. That is, their (current) digital offer is not a direct substitute for the physical offer. When providing their WTP for the digital offer, however, users also consider the added value created from these cultural institutions, such as community outreach programmes or educational work. This suggests there is a strong overlap between the ‘physical’ and digital offers of arts and cultural institutions in the minds of the public. As such, when individuals are asked to value the work of galleries and museums, they may struggle to separate the two.

Taken together, these results tentatively suggest that contingent valuation techniques may carry across to digital cultural contexts though qualitative work needs to be done to understand the bounds of what users are in fact valuing. An additional consideration is that the public’s expectations of what a typical digital offer should be is likely to be in flux as rapid technological progress creates new opportunities for online experiences. It cannot also be ruled out that the estimates are affected by the public’s experience of the lockdowns, which had preceded the survey data collection, and which had limited their traditional access to galleries, museums, and other venue-based forms of cultural engagement. Future research recommendations include cognitive testing of the WTP questions (and repeating the exercise over time) to probe their robustness.

2. Introduction

2.1 Background

Arts Council England (ACE) commissioned Simetrica-Jacobs and the Creative Industries Policy and Evidence Centre, led by Nesta to enhance its, and the wider arts and cultural sector’s, knowledge and use of economic techniques to measure the value of cultural activities and institutions. The results of this project contribute to the Culture and Heritage Capital (CHC) framework launched by DCMS in January 2021 which aims to create publicly available estimates and guidance that will allow for improved articulation of the value of the culture and heritage sectors in decision-making. The outputs of the CHC Programme will not only be applicable to the public sector but can also act as a useful tool to assess the public benefit of privately held assets.

There is increasing recognition of the benefits of applying HM Treasury Green Book (2022) endorsed techniques from welfare economics to value the non-market as well as market benefits of culture.[footnote 10] ACE have published evidence and guidance[footnote 11] to help organisations in the arts and museums sector which are consistent with the Green Book. The Green Book’s welfare approach aims to capture the Total Economic Value (TEV) of public policies and interventions. Despite being referred to as “Total Economic Value”, the aim of ACE’s programme is not to measure the benefits to the economy, such as the Gross Value Added (GVA) and employment, but rather to value the benefits of cultural and heritage attractions to society, for example in terms of welfare or wellbeing, education, and local pride. Valuing these benefits is challenging as they are personal to the people who receive them; however, public economics methods allow for their value for the public good to be estimated. Without estimates of this value, it is not possible to consider the benefits to people and society on the same monetary basis as costs, which is important for sound public decision-making.[footnote 12] Gathering this evidence is particularly important in cases where SCBA is required for cultural or heritage institutions, but where market values (e.g., entry fees) do not exist or where there is a strong case that the value of an institution is greater than the collective price people are willing to pay for individual access. Valuation approaches can also be used to make internal resource decisions within institutions (the British Library study being a commonly cited example in the cultural sector, see Pung et al.).

The Mendoza Review (2017) highlighted more broadly the importance of museums having and using consistent and statistically robust methods to measure economic and social impact.[footnote 13] It also indicated that local authorities have a role in helping museums to measure their impact and deliver the evidence of this impact. The DCMS Tailored Review (2017) concluded that ACE should be a sector leader in developing a rigorous methodology to assess the outcomes and impact of its funding portfolio (i.e., beyond just measuring inputs and outputs).[footnote 14] More recently, the DCMS have published their Culture and Heritage Capital Framework (2021) as noted earlier, setting out an ambition to produce supplementary guidance to the HM Treasury Green Book (2022) specifically for the Arts, Culture, and Heritage sector. It is also worth noting that materials being produced to support this Framework have been recommended by the Department for Levelling Up, Housing and Communities (DLUHC) as part of their application guidance for programmes like the Towns Fund and Levelling Up Fund.

While progress has been made to evidence the value of larger (regional and national) museums and art galleries,[footnote 15] theatres[footnote 16], and smaller museums[footnote 17], the value of the content published by arts and cultural institutions online is yet to be considered. For the purpose of this report, ‘digital offer’, or ‘digital content’, is taken to mean as any online content offered by galleries and museums, which may include audio and visual imagery, games, videos, social media posts and more.

There are many reasons why it may be important to consider the value of the online content of galleries and museums.[footnote 18] These include:

- this type of art and culture is widely, and in most cases, freely available for everyone to access, but costly to digitise, store and curate

- online content is not constrained by the physical space of the venue and so it has the potential for much greater access, at least by users who have an adequate internet connection

- digital content has the potential to enrich the public’s engagement with the gallery or museum’s collection through providing additional information and content, which may be enjoyed by users in their own time and location[footnote 19]

- digitisation helps to preserve cultural heritage for future generations

- it is a resource for researchers as it provides them with easier access to the museum or gallery’s collections in the same way it enhances access for the general public

- as the COVID-19 pandemic has shown, museums and galleries have pivoted their offering from physical to digital, in order to retain an offer to users even when physical access is constrained[footnote 20]

However, valuing this type of digital cultural offer is difficult for a number of reasons. Foremost, in the vast majority of cases, the digital content is built on physical artworks or artefacts which are the underlying source of the value, and users may struggle to conceive of this value separately from that of the online content. At the same time, invariably the type of online gallery and museum content considered in this report is available for free so the public may have no ‘anchor’ for their stated valuations. The latter is likely exacerbated by the high degree of heterogeneity of online content that is typically on offer – podcasts, virtual tours, and workshops, all relating to different collections – to name but a few. An implication is that estimates of the value of the digital content offered by galleries and museums might be expected to be noisier than is the case for their traditional physical offer. The exploratory nature of the analysis, therefore, as well as the heterogeneity of the digital offer means that the willingness-to-pay (WTP) estimates presented for the four study sites in this report should not be transferred to other galleries or museums.

2.2 Values for ‘non-market’ institutions

Millions of people visit art galleries and museums annually in England. People may value their visit more than any entrance fee they pay; indeed, entry is often free. Typically, not everything is on display in exhibitions, with sometimes the great majority of items being held in storage to preserve for future display, and in other cases artefacts being lent to other venues for exhibition. The digitisation of the items making up a gallery or museum’s collection and online publication of the images allows the public to engage with items that are not currently on display, and this is also typically free. Furthermore, in many cases education outreach and research work make up a substantive part of a gallery or museum’s offer to the public, the value of which may not be fully reflected in (any) entrance fees.

More generally, the benefits that arts and cultural institutions like galleries and museums provide to society tend not to be fully mediated by market mechanisms. They are termed non-market goods or services because they are often not tradeable and so are not reflected in market prices. Consequently, they often are not quantified in SCBA, meaning that they are not fully considered when appraising investment in comparison with more quantifiable economic benefits. An evaluation that focuses only on market prices therefore underestimates the full public value of a cultural institution. Valuing these benefits can be very challenging as they are personal to the people who receive them, however economic techniques from public economics are available to allow them, under some assumptions, to be estimated. This approach has been successfully used in other sectors, such as in the Natural Capital Approach developed by The Department for Environment, Food and Rural Affairs (DEFRA) which allows the value and sustainability of the environment to be included more completely in decision making.[footnote 21]

Government guidance in the UK Treasury’s Green Book (2022) and DCMS’s Culture and Heritage Capital Framework recommends that non-market goods like culture be valued in monetary terms, and often this requires the use of Stated Preference (SP) surveys.

2.3 Stated Preference (SP) valuation: Putting prices on non-market goods

SP surveys present relevant groups (e.g., visitors, users, residents, the public) with information about an asset. A WTP value is determined from how much respondents state they would be willing to pay to continue to enjoy the asset in a hypothetical scenario where access is no longer free of charge (or in the case of willingness to accept, WTA, stating how much they would be willing to accept by way of compensation were access to be restricted or lost).[footnote 22] This method is used by several public bodies, such as the Department for Transport, in policy-making decisions around the value of travel time[footnote 23] and impacts of construction projects on iconic heritage sites.[footnote 24]

This SP research technique is known as Contingent Valuation (CV), because it involves the design of surveys asking respondents directly to report their values contingent on there being a hypothetical market. Implementing the CV methodology is challenging but over a few decades of application, a range of best practice techniques have been developed to improve the robustness and welfare consistency of the values elicited.[footnote 25] These values are:

- a maximum willingness to pay (WTP) for a positive change — for example, what would be the maximum value that the respondent would be willing to pay to have extended opening hours for a gallery, or how much they would be willing to pay to attend an online workshop hosted by a museum.

- a minimum willingness to accept (WTA) in compensation for a negative change or to forego a beneficial outcome — for example, how much money the public would require to compensate them for the removal of online content from a museum website

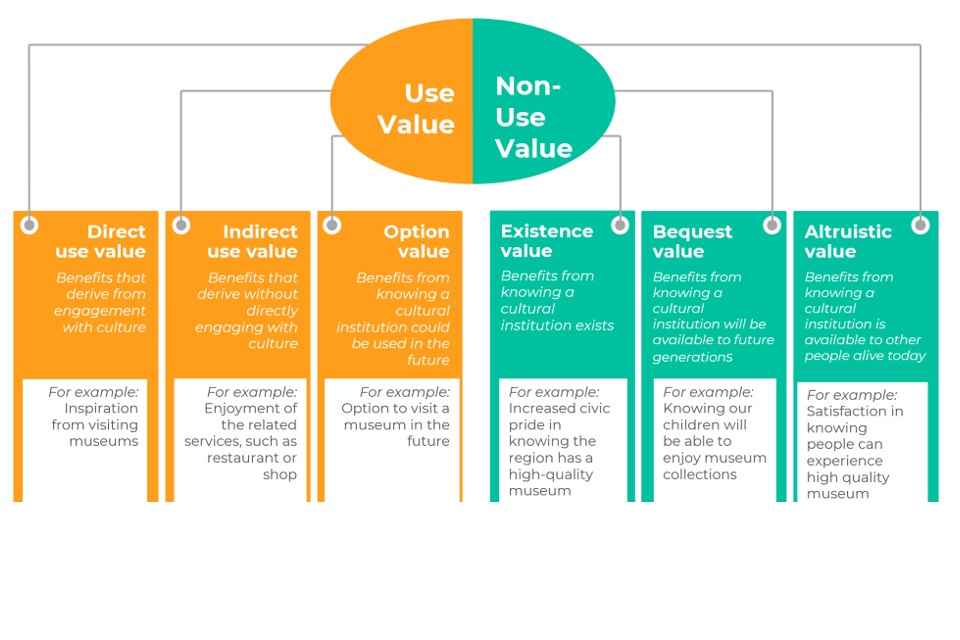

The advantage of the CV method is that it can estimate the values that visitors, or users, obtain from an institution or an institution’s online content (see Textbox 1), including:

- direct use value, regarding the individuals actual or planned use of the institution’s online content, and

- indirect use value, the benefits that derive without directly engaging with the digital offer

This is in addition to the benefits that individuals who do not use the institution’s services may in principle enjoy:

- non-use value, regarding the value held for the institution’s continued existence and provision of its services to others, and

- optional value, that both users and non-users may get from being able to use it in the future

As CV surveys rely on respondents to state their willingness to pay, one disadvantage is that respondents may ‘launder’ or omit their true preferences. This can be because they are answering in the way they believe they would want to answer (e.g., meta-preferences) or answering in a way that looks more socially desirable by ‘cleaning’ their answers and/or making them appear ‘more consistent’ in their eyes. The risk that respondents may launder their preferences in these ways can be partly mitigated in the design of the survey instrument through consistency checks and data cleaning.

A significant shortcoming of the CV method is that the WTP/WTA values elicited may not be incentive compatible. That is, because the payments/acceptances are hypothetical there is no reason why they would necessarily correspond with what survey respondents would actually pay/accept if the market did exist. There is also a question as to whether CV surveys are appropriate within sectors such as health or culture, as this method relies on an individual’s willingness to pay and generally does not account for an individual’s inability to pay due to financial constraints. This may then mean that cultural services that have disproportionate numbers of higher socioeconomic group users who can pay for them, may make a stronger case for funding than cultural services with disproportionate numbers of lower socioeconomic group users who cannot pay for them. In practice, the best practice techniques as mentioned above include truth-telling devices within the survey to try and minimise the bias arising from incentive incompatibility, and those devices are employed here.[footnote 26] A question exploring whether ability to pay because of financial constraints influences the WTP elicited is also included in the survey to better understand the groups that benefit from the cultural service.

Another feature of the CV method is that the WTP/WTA values elicited are dependent on how the good or service is defined within the survey. Those using WTP values for SCBA purposes should pay close attention to how the good or service is defined in the survey, what kind of payment it relates to (e.g., tax, entry fee, or donation), and the payment term (either an annual payment for a fixed period or a one-off payment for the life of the good or service). It is important to provide realistic valuation scenarios that reflect the nature of the good or service being valued (e.g., a subscription fee for a video streaming service). Compulsory payment vehicles (e.g., a state tax, an entry-fee, or a fee to access a service) may reduce the risk of free-riding (i.e., respondents not willing to pay because they do not believe they have to pay) that is problematic with CV surveys. Follow-up questions are best placed to investigate whether respondents found the payment vehicle and scenario to be realistic.

To account for these disadvantages, a minimum sample of 200 respondents is advised with advanced survey design, including presenting payment options (e.g., payment cards or dichotomous choice), with appropriate consistency checks and data cleaning to reduce any survey biases that may still be present.

Textbox 1: Overview of values

Use value refers to the WTP stated by those who have visited or otherwise engaged with the gallery or museum within a designated time-period. While these are expected to be primarily use values, it is acknowledged that visitors may also hold non-use values for the preservation and maintenance of collections. Use value within this study refers exclusively to the WTP values held by visitors (i.e., users) for accessing the digital offering, the online content, of the art gallery or museums.

Non-use value refers to the WTP stated by those who have not visited or engaged with the gallery or museum within a designated time-period. While these are expected to be primarily non-use values, it is acknowledged that non-visitors may hold elements of use value, such as the option value to access the art gallery or museum’s online content in the future.

Table 1.2 Total Economic Value

To estimate the value held for the digital offer, a CV survey was designed that asks respondents to report their willingness to pay (WTP) for selected cultural institutions’ online content. In this report, ‘physical site’ refers to only the physical site of the institution (the gallery or museum), whereas ‘digital offer’ is the online cultural content valued and offered. ‘Site’ in this report refers to the four institutions selected for the survey, and which refers to either their physical or digital offer.

3. Review of literature

Most art galleries and museums now have some form of online presence of their collection. For example, in Arts Council England and Nesta’s 2019 Digital Culture survey, as many as 70% of museums in England surveyed reported that they were currently publishing content on free platforms, 69% were engaging in digitising their collection and 20% were providing online interactive tours of real-world exhibitions.[footnote 27] The ‘digital offer’ considered in this report may include audio and visual media, games, social media posts, online research resources and digitised exhibits. The term ‘digitisation’, in contrast, refers to the process of ‘uploading’ exhibitions online for public display, as well as creating a private digital repository (which could include the object’s storage location, barcode, and relevant metadata) to support the institution’s internal processes.[footnote 28] Previous research suggests that this digital content appears not to compete with the physical offering of the museum in the eyes of the public; rather, it allows potential visitors the chance to connect with and experience the museum’s offer in different and potentially complementary ways.[footnote 29]

This literature review sets out to survey the different methodologies that have been previously applied in valuing the digital offer of arts and cultural organisations. However, we find surprisingly few such studies (Bakhshi and Throsby’s study of the online offer from Tate Liverpool’s Colour Chart exhibition and of the National Theatre’s NT Live broadcasts in 2009 is an early exception). This is likely in part a reflection of the challenges in applying techniques like contingent valuation to experiences that are novel to consumers. Compounding this is the fact that online content from galleries and museums is almost always free to access, making it inherently difficult to value and it is difficult in research valuation purposes for respondents to provide a value for something they widely access for free. In such cases, some analysts suggest alternative SP techniques to WTP such as Van Westendorp’s price sensitivity meter[footnote 30] might be preferable.

Yet, empirical evidence on the value of gallery and museum digital offers would be timely given the significant numbers of individuals that engaged with the collections of galleries and museums during the recent lockdowns when physical access to venues was prohibited. In a cohort study of adults in the first UK-wide lockdown in 2020 by the Creative Industries Policy and Evidence Centre and the Intellectual Property Office, as many as 13% - 17% of individuals reported to be looking at art, paintings, and photographs online on a weekly basis.[footnote 31]

The extent of the ‘pivot’ of cultural institutions towards engaging with the digital audience in lockdown was largely dependent on the organisational culture, acceptance, and preparedness of institutions.[footnote 32] While some institutions were already digitally ‘switched on’ so to speak, the largest shift in thinking was required of those institutions that were less prepared.[footnote 33] Museums and galleries became more data-driven with a greater emphasis placed on understanding these new digital audiences. One study[footnote 34] interviewed museum and gallery digital leads around the UK and reported a widely held belief that digital audiences were not demographically dissimilar to traditional in-person audiences. There was little suggestion that institutions’ digital offering had increased the diversity of audiences; families were identified as a particularly difficult audience to reach using digital platforms. These beliefs were shared by institutions - even those that had consciously tried using their digital presence to reach new audiences, including younger generations, which were thought to be a more difficult audience to sustain over the long term. This study also reported some trends seen in the digital offer that more successfully engaged the public. Blog posts, podcasts, some social media, and online shops were popular, with some institutions finding online donations as a reliable income stream, but downloadable resources were not popular according to the institutions interviewed. Some institutions intuitively experienced a reduction in web traffic on pages relating to visitor information and physical collection pages. A common theme identified was the challenges institutions face in providing a cultural offering online in a financially sustainable way when other such cultural content is freely and widely available.

In 2018, the UK-based economics consultancy, Oxford Economics, was commissioned by the Canadian Museums Association (CMA) to undertake a national study that looked at the value of galleries, libraries, archives, and museums (GLAMs)[footnote 35], part of which focused on the value of GLAMs’ online offerings. The value of online services was framed as a value for information, and the cost associated with this information was expressed in terms of time. The expectation being that if the online services did not exist, then online users would face higher (physical) access costs and, consequently, may be deterred. A demand curve for GLAMs content was created by asking respondents to estimate time spent on GLAMs’ websites and supplemented by responses to a national survey on digital engagement and also analytics shared by GLAM institutions. These estimates were subsequently combined with Canadian ‘values of time’ to produce a time cost of online usage per session. Utilising Canadian Heritage and CULC data on the number of online sessions and sensitivity to the cost of time online, the consumer surplus of GLAMs’ online services was estimated at $1.6 billion Canadian dollars per annum.

Outside the immediate area of focus on galleries and museums, valuation research has been undertaken elsewhere in the digital economy. Brynjolfsson and colleagues[footnote 36] estimate the value of social media platforms like Facebook and WhatsApp, through a series of discrete choice experiments. For this, respondents were given the option to keep access to the social media platform in question or give up the access for one month and receive a (randomly allocated) payment as compensation. To ensure respondents stuck to their commitments, their Facebook accounts were monitored remotely. These experimental design features aimed to make the stated valuations incentive compatible. In their sample of 2,885 participants who were 18 or older and lived in the United States (US), the average WTA value for one month of no Facebook access turned out to be US$42.17. A second study[footnote 37], conducted in the UK, estimated WTA values for a range of free online goods, such as online grocery shopping, online learning, WhatsApp, and Netflix. The survey was first undertaken in February 2020 (ahead of the UK lockdown) and then repeated in May 2020 (before any easing measures had begun). The research found that valuations for free online goods generally increased between February and May 2020, although there were declines in the valuations for some of the online goods, such as LinkedIn and personal emails. For example, WhatsApp elicited an annual WTA median average of £1,588 in February increasing by 11.8% to £1,774 in May. Conversely, Google maps elicited an annual WTA median average of £1,307 in February decreasing by 21.4% to £1,027 in May. A further study estimated WTA values for free social media platforms (Facebook, Instagram, Snapchat, Skype, WhatsApp, digital Maps, LinkedIn, and Twitter) in a sample of university students within the Netherlands. Respondents were again asked how much they would be willing to accept for giving up each of the social media platforms for one month. To ensure participants committed to the program, their passwords were changed and protected in a sealed envelope. Thereby, a broken seal revealed the respondent had accessed their social account. WhatsApp elicited the greatest WTA median average of €535.73 per month as respondents reported this was their main communication format with friends and family. The research has a number of important research design challenges, but it shows that although difficult, respondents are able to provide a monetary value for content even if they have always considered it to be free.

Consistent with this, in a gallery and museum context, previous research from Arts Council England surveying those who engaged with digital cultural content, although falling short of a full CV study, found that while 63% of respondents believed that online cultural content should be free, 32% agreed with the statement “I am willing to pay for online arts and culture if I get something extra (e.g., exclusive content or access offline)”[footnote 38] (ACE, 2010). When asked what these digital culture users would be willing to pay for various categories of digital content, WTP ranged from £3.04 for a phone app that provided location-based information regarding archives to £7.89 for viewing an online theatre performance.

As part of the British Film Institute’s (BFI) digitisation process, the Britain on Film (BoF) programme prepares, stores, and maintains film collections. The BoF programme also provides a national archival online collection of digitised British film and television, with the majority free-to-watch for the UK public. Lawton et al.[footnote 39] conducted a CV study to estimate the non-market value of a free-to-view digital service and the wider Unlocking Film Heritage archive programme. Respondents were asked their monthly WTP for a subscription fee to access the online content if they were users or a donation if they were from the wider UK public. Users were found to be willing to pay a median monthly subscription of £3.21 to access the BoF content with a median monthly donation of £2.26 for the BFI’s archival work. The wider public, who had not used the BoF, were willing to pay £4.68 on average as an annual donation to the BoF digital content and £3.44 for BFI’s archival work.

While both experiential and authenticity considerations suggest that the physical offer should be valued more greatly than the digital offer, it should be noted too that the digital offer may in fact be valued greater by some users. Digital offer may be valued highly due to its ‘on demand’ nature, lack of congestion effects, which are known to reduce the value of visits,[footnote 40] and content features which deepen the experience. While the research presented in this report does not attempt to estimate the degree of substitutability between the offline and online offer, survey questions are used to generate insights on the differences in value to different users.

4. Methodology

This section provides details of the contingent valuation of the digital offer from four art galleries/ museums located in England.

4.1 Site selection

Four digital offers were selected based on the size of the physical sites: the sites were each based in English towns or boroughs of at least 200,000 inhabitants which had an art gallery or museum with a digital offer that met the definition of digital offer outlined below. The number of annual visits and regional significance match broadly those of the sites studies in previous research undertaken by Simetrica-Jacobs and the Creative Industries Policy and Evidence Centre for consistency.[footnote 41]

For the purposes of this study, ‘digital offer’ is defined as the free-to-access online content offered by art galleries and museums, which includes:

- image albums and slideshows

- audio (including audio description, podcasts)

- games

- illustrated essays (webpages with text and images)

- maps

- social media posts

- timelines

- turn-the-page presentations

- videos

- virtual visits (360° explorations)

- visible storage (including online collections on display and out of display)

The following four sites and their digital offers were selected:

- The Derby Museum and Art Gallery in the East Midlands presented a ‘make and create’ drawing workshop directed at children and families.

- The Bristol Museum and Art Gallery in the South-West of England presented 3D imagery and renditions of their Pliosaurus specimen, alongside audio and text.

- The Foundling Museum in Greater London presented a series of talks delivered by video around the history and notable persons of the site.

- The Great North Museum in the North-East of England presented some of its collections online alongside some virtual tours.

4.2 Sampling approach

Survey respondents were sampled based on the region that they reported living in. Those respondents who identified that they were from one of the regions (East Midlands, South-West of England, Greater London, and North-East of England) that the four sites are located in (the Derby Museum and Art Gallery, the Bristol Museum and Art Gallery, the Foundling Museum, and the Great North Museum[footnote 42] were directed to the respective site’s questions (e.g., if a respondent was from the East Midlands they were allocated the Derby Museum). Those who identified they were not from one of the four regions were randomly allocated one of the four sites that they may or may not have physically visited. This sampling approach assumes that respondents are more likely to have visited the physical site located within their region and possibly engaged with the digital offer online or were at least familiar with the physical site. Follow-up survey questions determined whether respondents had indeed (physically and digitally) previously visited their allocated site. Only 36% had physically visited one of the four sites within the past three years. Of those who had previously visited the website and engaged with the digital offer, 10% reported that they had not visited the digital site within the past 12 months (see Section 4.2). Further, 78% of the total sample had said that they had not visited any art gallery or museum at all within the past 12 months. This result is to be expected given the restrictions around physical visits and reopening of UK museums and galleries during the COVID-19 pandemic. In this study, the focus is restricted to the use value of the digital offers; non-use values are not estimated. Attempting to estimate the latter would seem to be particularly challenging given that access to a website (‘use’ in this context) is so straightforward, assuming that users have a reliable internet connection and a device to access the digital offer.[footnote 43]

Specifically, this study focuses on repeat users (i.e., those who report to have visited the website before) and first-time users (i.e., those who claimed not to have visited the website before but who did so now as part of the study). It should be acknowledged for the latter group particularly that the WTP for the digital offer may be influenced by having interacted with the digital offer immediately beforehand. Any biases that may arise as a consequence of this were not able to be controlled for. The authors recommend that possible cognitive biases arising from this feature are explored in future research.[footnote 44]

Lastly, the sample was recruited to be representative of that of the general population (based on region, gender, and age from Census data). However, it should be acknowledged that users of digital content are likely to be different to users of the physical site and to that of the general population in terms of demographics. In other words, the sample may not be reflective of digital cultural content users. There is some evidence to this effect within the DCMS Participation Survey October 2021 to March 2022.[footnote 45] Respondents located in and around London were more likely to have ‘taken a virtual tour of a museum or gallery in England’ or have ‘engaged with text, image, audio, video, or animation, games, or podcast content from museums in England’ than respondents elsewhere in England.

4.3 Survey design

A third-party panel provider, Toluna,[footnote 46] was used to recruit the sample for the online survey. For this, Toluna advertises the online survey and potential survey respondents self-select into the survey. Survey respondents who complete the survey receive a monetary reimbursement for their efforts. This method may elicit survey biases:

Because survey respondents self-select into the survey, respondents may have a greater interest in culture, which may result in the WTP values being inflated due to a disproportionate number of culture consumers. Questions around respondents’ attitudes towards arts and culture and previous visits to physical and digital sites allow the sample to be compared to that of the national population (by benchmarking these answers against the DCMS’s Participation Survey for example).

As survey respondents are paid for their completion of the survey, some respondents may be inclined to complete the survey for monetary gains without providing accurate answers. Steps have been taken to exclude spam (those responses not believed to be human), speedsters (survey respondents who completed the survey in a short period of time), and those respondents who provided unreliable answers (their answers contradicted earlier answers). Further details are provided in the Appendix (Section 6.1.1).

An online survey instrument was designed on the survey platform Qualtrics to value the digital offers of each of the four sites in question (the Derby Museum and Art Gallery, the Bristol Museum and Art Gallery, the Foundling Museum, and the Great North Museum).

Reflecting both what published research is available and the payment models used by popular streaming platforms in the market (e.g., Spotify, Netflix) a subscription-based payment vehicle was used in the contingent valuation scenario. This is because digital paywalls are how most media and content organisations - be they news services or SVOD video platforms charge for “entry” as it were to access their content, sometimes with options to pay-per-use or pay for a set period (e.g., pay-per-month) (Ruβell, et al. 2020). Another reason for opting for subscription as the preferred payment vehicle for the present research is that a subscription paywall should in principle reduce free-riding within the survey. Specifically, a subscription-based payment vehicle is more incentive compatible than other options, such as a voluntary donation, whereby payment is optional, and individuals may hold that belief that they do not have to pay as others will instead.

Sites: The Derby Museum and Art Gallery, the Bristol Museum and Art Gallery, the Foundling Museum, and the Great North Museum

User WTP: to access the digital content from one of the four galleries/museums.

Good valued: Access to digital content of the gallery/museum.

Payment vehicle: Subscription fee (monthly on behalf of their household). A payment term, such as one year, was not specified. This is more in line with realistic subscription fees for popular streaming payment models on the market, whereby users review their fee to access content monthly but are free to cancel at any time. This means that while the payment vehicle is realistic, it is also weaker as the valuation scenario does not specify exactly how long respondents should consider this reoccurring monthly payment for. The WTP results should therefore only be considered for one month and should not be aggregated beyond this. Any findings are caveated with this in mind.

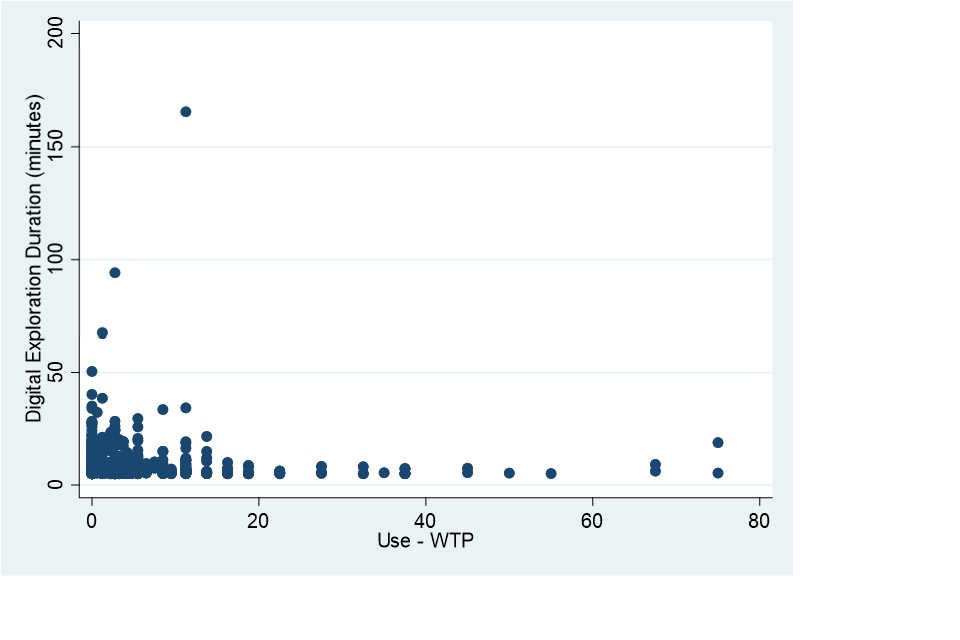

Use valuation scenario: Respondents were given information about one of the four sites they had physically visited (or were randomly assigned to one if they had not previously visited). This included information about when the gallery or museum first opened, its collections, awards won, and about the nature of its digital offer. Attention was drawn to the fact that the digital content provided by the gallery or museum was free. Photographs of both the interior and exterior of the gallery, alongside snapshots of the website content were presented. In order to value the good, respondents were asked to explore the digital offer of the site for at least five minutes. As an interaction bias check, the analysis tested to see whether longer interaction time with the digital offer (in minutes) increased the amount that respondents were willing to pay for the digital offer. In the event there was no consistent evidence of this source of interaction bias.

Contingent scenario: After approximately five minutes[footnote 47] of exploring the digital offer, respondents were reminded that the digital content was free-to-access online and told that most of the institution’s funding comes from a government grant. They were asked to imagine a scenario where the difficult national financial situation meant that many galleries and museums in England had suffered cuts in funding. As a result of which, the institution would have to start charging for the digital content they offered. The valuation explicitly outlined that any cuts in funding would not have any impact on the physical gallery or museum itself and that it would continue to remain open and running. Respondents were further told that the digital offer would be updated with new digital content and added to on a regular basis. The frequency of the digital offer updates was not specified further, as the digital offer and the updates to the digital offer vary widely over time (e.g., aligning with exhibition dates, monthly posts for new workshops, etc).

Follow-up scenario: As a follow-up valuation, respondents were asked how much they would be willing to pay for entry to the physical site itself on a future visit. This scenario was only presented to respondents who had indicated that they had previously visited the gallery or museum.

Initial survey questions determined which respondents were arts and culture consumers, respondents’ attitudes to culture, their previous gallery and museum visit history (the past three years), and their past experience of engaging with culture online. Questions following the valuation itself determined the motivation behind respondents’ WTP (or not), whether the COVID-19 pandemic had had any impact on their access and consumption of digital content and their WTP, and standard demographic information.

The four sites (see below) each provided free of charge an aspect of digital offer that met the definition in Section 3.1.

The Derby Museum and Art Gallery

The Derby Museum and Art Gallery offers a range of online content, including a range of workshops and activities that are suitable for children and families to complete at home, such as building your own board games, making pinhole cameras, and creating paper sculptures.

The Bristol Museum and Art Gallery

One of The Bristol Museum and Art Gallery’s digital exhibitions offers detailed insights into “Doris” the eight-metre long Pliosaurus, discovered in Wiltshire in 1994 and on permanent display at the site. The digital exhibition contains statistics and facts on Doris, including 3D fossil imagery and also provides visitors with background audio of deep ocean sounds whilst interacting with the digital content.

The Foundling Museum

The Foundling Museum’s online talks, including the “Dr Hunter’s Secret Delivery” talk, goes into the Foundling Museum archives and reveals stories, such as those of a noble lady whose twins were secretly taken to the Foundling Hospital.

The Great North Museum

The Great North Museum offers a range of virtual tours and online exhibitions, such as the artworks by Atomhawk, an art and design studio which has visualised the look of world-famous franchises such as Harry Potter, Star Wars, and Marvel.

Pilot survey: A pilot survey was conducted to establish an appropriate range of WTP values.[footnote 48] Pilot survey debrief questions confirmed that the survey was functioning correctly and debrief responses provided sufficient confidence to proceed into the field. The results from the pilot survey identified that no changes were required to the survey before sampling.

4.4 Data cleaning

In total, 1,726 respondents completed the survey. The survey included pre-screening questions at the start that filtered out respondents who were flagged by the Qualtrics online survey design platform as being spam[footnote 49] (n=4), being under 16 years of age (n=1) or having duplicate responses (n=1).

After cleaning, we excluded some responses from the final data set, as detailed in Section 6.1.2 and below:

- Those with unreliable responses.[footnote 50] (These responses were given a minor flag and individuals were removed from the final data set if they received multiple flags.[footnote 51] respondents received at least 1 minor flag and of these 23 respondents received a major flag. Note that these groups are not exclusive.)

- Those who said they chose a WTP amount because they did not believe they would really have to pay (n=12). Because the stated WTP for these individuals did not reflect their financial constraints, this is an indication that they did not answer the question in a realistic way.

- Those who completed the survey in an unrealistically fast time (n=495). Removal of so-called ‘speedsters’ is recommended practice in CV analysis. A threshold time of 10 minutes was set as the minimum period in which all the information provided in the survey could realistically be read and a compulsory five-minute session to explore the digital offering could be used to make informed preference decisions. The average survey completion time was long, at approximately 38.6 minutes, which provides some confidence that survey respondents explored the digital offer for at least five minutes and took time to consider their survey responses.[footnote 52] Excluding respondents such as these left 1,177 valid responses. While the exclusions reduced the survey sample, it was preferable to have a more robust set of responses that provide greater confidence that the WTP estimates were accurate reflections of the value respondents attached to their experience. It should be acknowledged, however, that the exclusion of these respondents could introduce some bias if they result in the systematic exclusion of certain type of respondent from the sample. To address this, ex post analysis (logistic regression) was performed and found no evidence of significant selection effects.

Table 3.1 Reasons for removal of response from final sample

| Reason for removal | ||

|---|---|---|

| First stage cleaning | Spam | 0.2% (4/1726) |

| Second stage cleaning | Follow-up: Would not pay in reality | 0.7% (12/1720) |

| Speedsters | 28.8% (495/1720) | |

| One major flag | 1.3% (23/1720) | |

| No valid WTP | 1.5% (25/1720) | |

| Final respondent sample | 68.4% (1177/1720) |

Note: The second stage cleaning process groups are not exclusive. One removed respondent could have been removed for various reasons and can fall into multiple categories.

Note that 140 respondents gave a WTP that was outside the scope of the valuation scenario but otherwise gave valid responses (i.e., ‘My willingness to pay is not just for visiting the [digital content], but also an expression of my support for all the work that [site] does’) were included in the final sample. While these respondents may have had willingness-to-pay valuations that were inflated compared with others, given that they valued more than just a digital visit, it was considered a valid reason for being willing to pay for the digital offer. The final WTP values are nonetheless caveated as they may be inflated due to the inclusion of these respondents. This potential distortion is quantified by presenting average WTP values with and without these individuals included (these results are presented in Figure 6.1 in Appendix 6.1.2).

4.5 Weighting

To ensure that the survey results were more representative of the population of digital visitors, calibration weights were applied to the data. To do this, website analytics were collected for visitors to each site and, where not readily available, their social media analytics were used instead.[footnote 53] Further details are provided in the Appendix (Section 6.2). While the use of social media analytics may not reflect the true population of website visitors, the authors suggest that those engaging with the museums’ social media offerings are also likely to engage with the website, so using weights derived from social media analytics are better than not weighting at all.

The survey data was weighted by employing iterative proportional fitting, more commonly known as raking. This methodology weights the data one variable at a time to give precedence to those under-represented in the survey. The weights used are the inverse of the selection probabilities, which are calculated as:

Where, refers to the share of the population meeting a certain weighting criterion (i.e., from a certain age group or gender) and is derived from website analytics, and refers to the share of the sample meeting that criterion and is derived from the survey. For example, if females represent only 50% of the survey respondents but made up 60% of the population of interest (i.e., a site’s website visitors), females will be given a weight of 1.2 (and non-females would be given a weight of 0.8). Similarly, if 35–54-year-olds represent 30% of the survey respondents but made up 20% of the population of interest, 35–54-year-olds would be given a weight of 0.67. That is, 20% divided by 30%. This process is then repeated iteratively for all variables that are being weighted over, in this case gender and age.

Raking is a popular method used by the Office of National Statistics and other public pollsters and is a recommended approach to weighting survey data (Valliant et al., 2018). Unlike post-stratification, which is another common approach to calibration using information on the cross-classification of the categories to be weighted on, raking has the advantage that it does not require information on the cross-classification but only the marginal population counts. In other words, it does not need the information from crossing several variables (e.g., gender split by age from a certain region). Rather, the data can be provided individually (i.e., gender split, age split, etc.). This allows for all the information available on the site demographics to be leveraged, even if it is sparse, and provides confidence that the estimation is as robust and efficient as possible.

4.6 Learnings and challenges

In the context of the digital offer of cultural institutions, market values (e.g., in the form of fees to access digital content) do not always exist. In this case, the digital offer valued is widely and freely available for all to access on the internet (including those who do not live in the United Kingdom) at any time of the day. Even where market values exist, they may not capture the full extent of value created. This is because, on one hand, for some fee-paying users the benefit may exceed the amount they pay, and on the other hand, some benefits may also accrue to those who do not digitally visit the museum (such as if it has option value or existence value, as outlined in Figure 1.2).

Stated preference (SP) studies in principle allow, through careful survey design, a means of eliciting WTP values from different groups (e.g., users and non-users). However, for this approach to work properly, the survey questionnaire needs to be tailored specifically to the features of the gallery or museum and the public it serves. As there is little precedent in the literature, this research should be read as an exploratory attempt to estimate the public’s value for the digital offer of art galleries and museums in England.

Valuing the digital offer specifically provides a set of distinctive valuation challenges:

- In practice, use values only are readily elicited: to be confident that survey respondents have engaged with the specific online content in question they are required to view the content immediately ahead of completing the questionnaire; see Figure 1.2 Any use value findings are therefore caveated by acknowledging that the WTP for the digital offer has likely been influenced by having only recently interacted with the content.

- The digital offer is highly heterogenous between and within sites. Due to the large variation in digital offerings available, all values obtained in this research are caveated and should not be transferred between sites. That is, these values should not be pooled or used in a benefit transfer. Reflecting this heterogeneity, the four sites studied in this report are vary greatly in their digital offer. For example, the Great North Museum presents a virtual tour of one of their exhibitions whereas the Derby Museum and Art Gallery which runs family-orientated ‘make and create’ online workshops.

- A monthly subscription fee (on behalf of their household) was the payment vehicle employed, however, to provide a realistic payment scenario no payment term (such as one year) was specified. To be conservative WTP results should therefore only be considered for one month and should not be aggregated beyond this.

- The final sample included those survey respondents who gave a WTP that was outside the scope of the survey (i.e., ‘My willingness to pay is not just for visiting the [digital content], but also an expression of my support for all the work that [site] does’). These respondents (n = 140) considered the value generated beyond the digital visit, nonetheless the authors believe this remains a valid WTP reason. But if that is wrong, the final WTP values may be slightly inflated due to the inclusion of these respondents.

- Lastly, the small sample sizes for some of the groups of respondents means further research is required before any strong conclusions can be drawn.

5. Results

The digital offer survey ran from 22 June to 3 September 2021. During this period, the COVID-19 vaccination programme was well underway with roughly 66% of adults in England having received their second dose by 19 July.[footnote 54] Restrictions on events had eased and cultural institutions had reopened for visits. Survey sampling was designed to elicit the views of users of the digital offer for each of the four museum sites.

5.1 Sociodemographic characteristics

Sociodemographic information was elicited from survey respondents, as is common practice in CV surveys (see Table 4.1). As noted earlier, a caveat to the research design is that all survey respondents were required to ‘use’ the digital offering and were deemed a cultural user, even though they may not typically visit and interact with arts and cultural organisations more generally (i.e., some respondents may have been what we call ‘first-time users’). Users of digital content may also be different to users of the physical site and to that of the general population in terms of demographics. Therefore, to derive more robust estimates of the value to users, the sample was weighted as below.

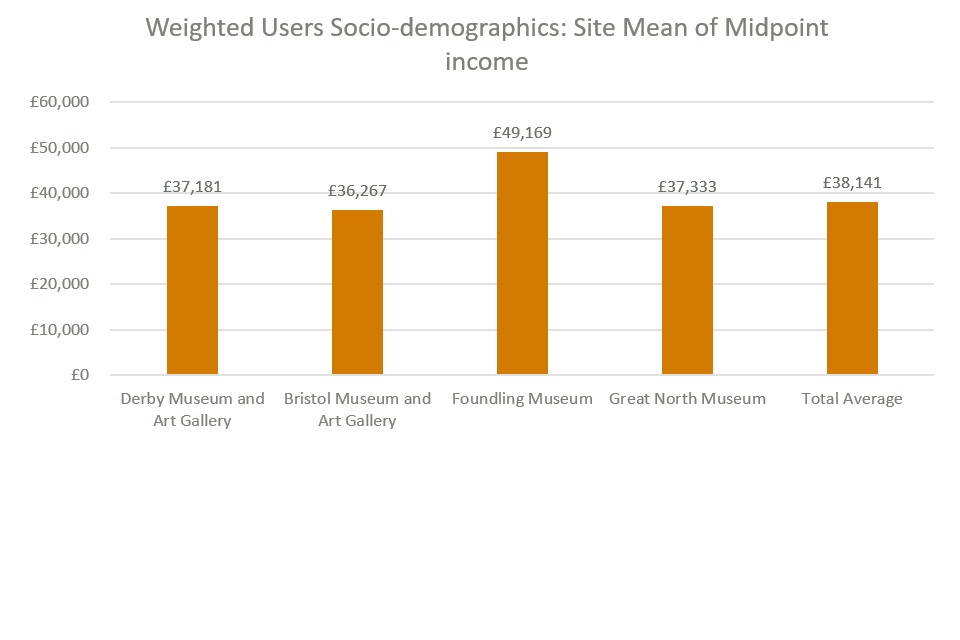

Table 4.1 shows a comparison between the unweighted responses and those implied by the weighted responses using sociodemographic breakdowns of web analytics data (and social media traffic in the case of the Great North Museum) using the procedure described in Section 3.5. It shows that there are some differences between the weighted and unweighted samples. The weighted sociodemographic data based on website analytics was notably a younger and more female group, with a higher percentage reported they had dependent children, were university educated and employed. For example, the unweighted responses for the Bristol Museum and Art Gallery are 57% females with an average age of 49 years old compared to the weighted responses (based on the web analytics) which are 60% females with a younger average age of 39 years old.

Table 4.1 User socio-demographic characteristics

| Derby Museum and Art Gallery | Bristol Museum and Art Gallery | Foundling Museum | Great North Museum | |

|---|---|---|---|---|

| Users | ||||

| Female: % (n/N) | 55.9% (181/324) | 57.1% (186/326) | 59.5% (188/316) | 51.7% (107/207) |

| Female: % (Weighted) | 56.7% | 60.0% | 64.4% | 60.0% |

| Age: mean (se) | 46.9 (0.90) | 49.3 (0.96) | 42.6 (0.94) | 54.1 (1.21) |

| Age: mean (Weighted) | 43.4 | 39.3 | 38.8 | 39.7 |

| Household annual income (£): mean (se) | £36,234 (1472.28) | £35,119 (1398.71) | £48,002 (1969.63) | £33,264 (1645.98) |

| Household annual income (£): mean (Weighted) | £37,181 | £36,267 | £49,169 | £37,333 |

| Has dependent children under 16 years: % (n/N) | 33.4% (109/326) | 27.2% (89/327) | 38.0% (120/316) | 19.9% (41/206) |

| Has dependent children under 16 years: % (Weighted) | 37.0% | 34.5% | 43.2% | 37.2% |

| Married/Civil Partner: % (n/N) | 46.7% (151/323) | 47.7% (155/325) | 45.2% (142/314) | 48.8% (100/205) |

| Married/Civil Partner: % (Weighted) | 44.7% | 40.0% | 44.4% | 37.6% |

| University education % (n/N) | 39.0% (126/323) | 41.6% (136/327) | 60.8% (191/314) | 44.1% (90/204) |

| University education % (Weighted) | 40.8% | 44.4% | 63.9% | 48.1% |

| In employment (full-time, part-time, self-employed): % (n/N) | 63.0% (204/324) | 58.0% (189/326) | 67.9% (214/315) | 55.3% (114/206) |

| In employment (full-time, part-time, self-employed): % (Weighted) | 65.4% | 65.5% | 71.5% | 72.3% |

Note: Smaller sample sizes feature throughout the tables in this report due to respondents opting out of questions (e.g., selecting the “Don’t know/Rather not say” option) or due to survey logic.

5.2 Attitudes to culture and heritage

Of the pooled user sample, 23% had visited a museum or art gallery in the past 12 months (see Table 4.2). Note that this research took place shortly after the reopening of museums and galleries following the COVID-19 lockdowns in England, accounting for the very low figure of recent visits (compared with the pre-COVID-19 figure of 67% as collected in the 2019 ACE survey of gallery visitors[footnote 55] and 51% as collected in the 2019/20 ONS Taking Part survey of museum or gallery visitors[footnote 56]. Similarly, the DCMS Participation Survey October to December 2021[footnote 57] found physical attendance at a museum in the previous 12 months to be 23% (during the period the DCMS Participation Survey reviewed, there were several prolonged periods of museum closures on account of COVID-19 regulations).

When asked what top five areas should be prioritised for public funding, 23% of pooled respondents listed arts and culture.[footnote 58] While this percentage accounts for less than a quarter of the sample, it is important to note that there were other areas of significant concern and political focus at the time the survey was conducted. For example, intuitively 79% listed public health as one of their top five areas for public funding. However, most respondents had been taken to art galleries and museums by their parents, guardians, or school before they turned 15 years old (82%) suggesting the respondents had had some long-term engagement with arts and cultural organisations.

-Table 4.2 User attitudes towards arts and culture

| Derby Museum and Art Gallery | Bristol Museum and Art Gallery | Foundling Museum | Great North Museum | Pooled | |

|---|---|---|---|---|---|

| User agreements | |||||

| Visited a museum or art gallery in the last 12 months (%) | 18.4% | 23.4% | 35.4% | 23.7% | 23.1% |

| Arts or culture amongst the top 5 priorities for public spending (%) | 23.4% | 21.4% | 24.6% | 27.9% | 23.1% |

| Introduced to art under 15 years old (%) | 79.1% | 83.9% | 86.0% | 81.0% | 82.2% |

| Member of a cultural, heritage, conservation, or environmental organisation (%) | 3.9% | 4.8% | 12.3% | 7.4% | 5.6% |

Most respondents agreed that preserving museums and art galleries for current and future generations was important (73%, see Table 4.3). Furthermore, most agreed that museum digital content should be free for all to access (68%). This suggests perhaps that the sample derives some non-use value from the digital offering of museums (though as noted earlier, this is not a possibility we analyse in this study). Only between 22% and 29% disagreed that ‘there are more important things than museums to spend my money on’, though as noted above these responses may have been influenced by the extraordinary priority attached to public health in the minds of most respondents at the time of fieldwork.

When asked whether they believed ‘digital content will replace in-person museum experience’, only 34% agreed, suggesting a clear distinction between the value of the physical and digital offer of museums and art galleries for most survey respondents. Following the contingent valuation scenario, respondents were asked if they were likely to continue to engage with digital cultural content in the future, to which 58% of all respondents agreed (Agree and Strongly Agree). Of these, 68% had not physically visited the museum or gallery in question in the previous 12 months. In the Audience Agency’s Digital Audience Survey (Summer 2021) of digital audiences for cultural institutions,[footnote 59] they found that 74% of digital visitors to organisations in their sample had never physically visited the organisation in person. These findings are suggestive that there may be a market for non-users of cultural institutions who are perhaps willing to engage with their digital offer, regardless of whether they have or have not yet visited in person.

Table 4.3 User agreements towards arts and culture

| Derby Museum and Art Gallery | Bristol Museum and Art Gallery | Foundling Museum | Great North Museum | Pooled | |

|---|---|---|---|---|---|

| User agreements | |||||

| Agree and Strongly Agree | |||||

| Preserving museums for the appreciation of current and future generations is important to me. (%) | 72.6% | 73.0% | 74.0% | 69.9% | 72.6% |

| Digital content will replace in person experience. (%) | 33.3% | 34.6% | 39.0% | 26.5% | 33.9% |

| Museum digital content should be free for all to access. (%) | 66.3% | 69.6% | 65.6% | 69.9% | 68.0% |

| Disagree and Strongly Disagree | |||||

| There are more important things for me to spend my money on than museums. (%) | 25.3% | 23.5% | 22.4% | 29.3% | 24.5% |

5.3 Visits

Previous visits

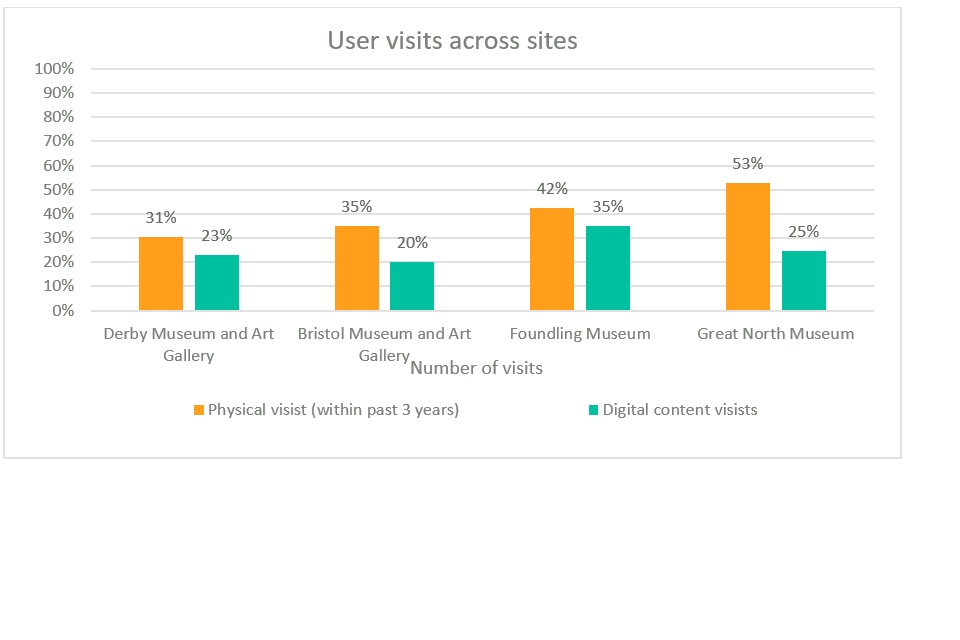

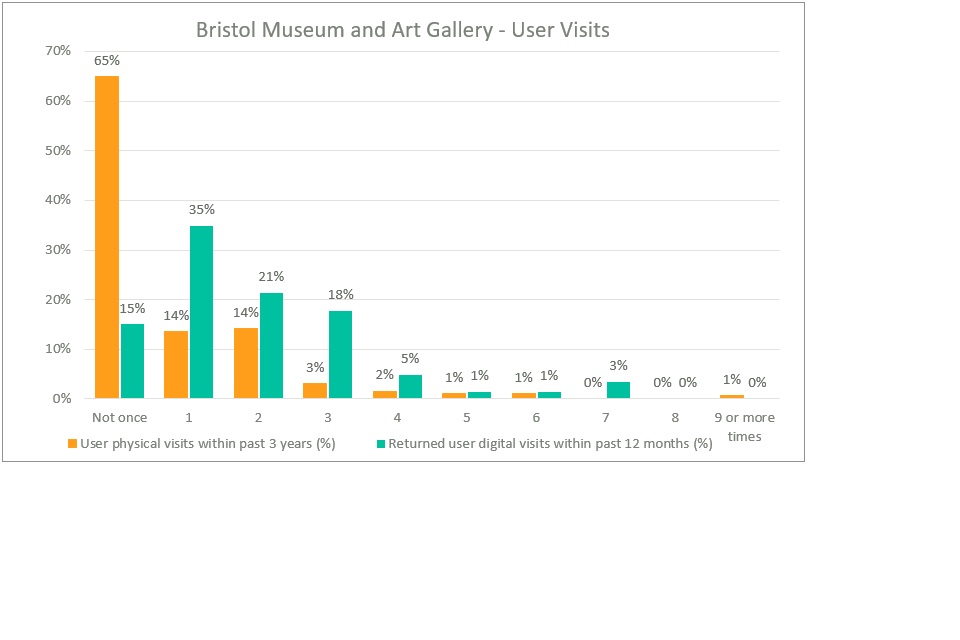

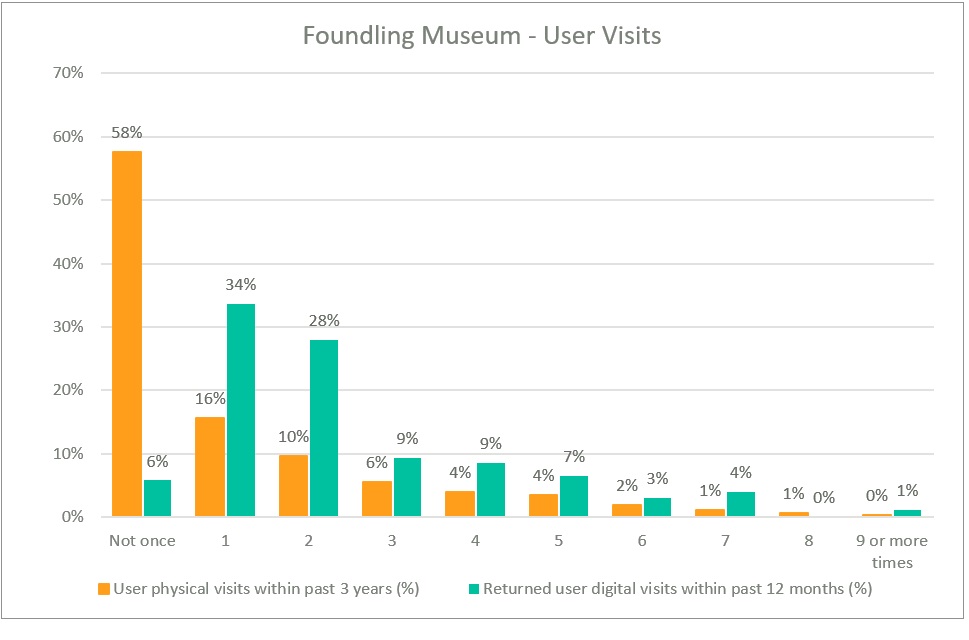

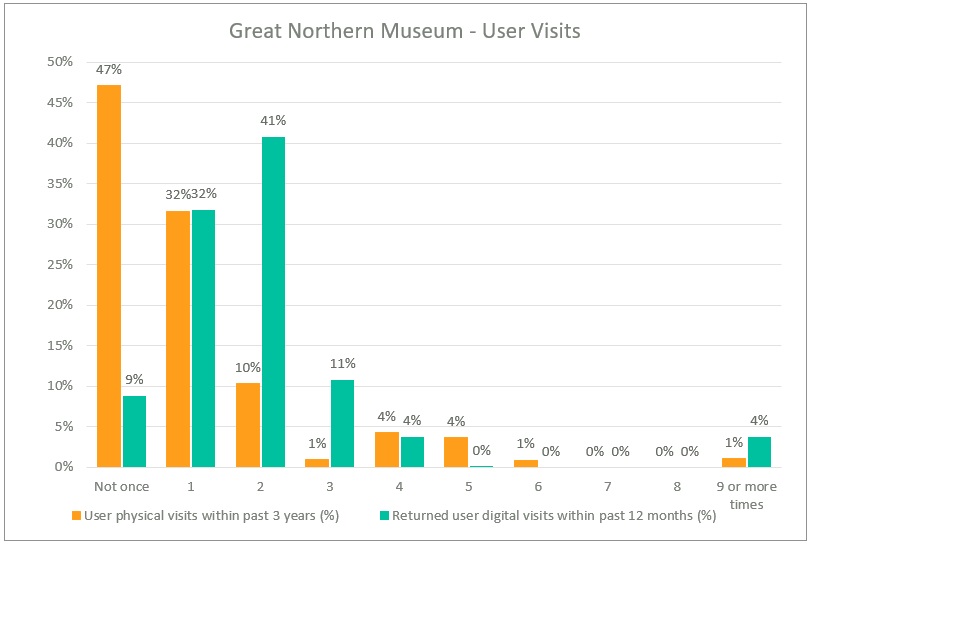

Figures 4.1 and 4.2 presents respondents’ self-reported physical and digital visits across the four galleries and museums. Respondents were first asked about their physical visits over the past three years. Three years was our preferred time period to use (compared with, say, one year), given that so many arts and cultural organisations had been closed for large periods in this time. Of the pooled sample, only 36% had visited the physical site in the past three years. 23% had browsed and accessed digital content from the institution in the past (Figure 4.1 for institution-by-institution figures).

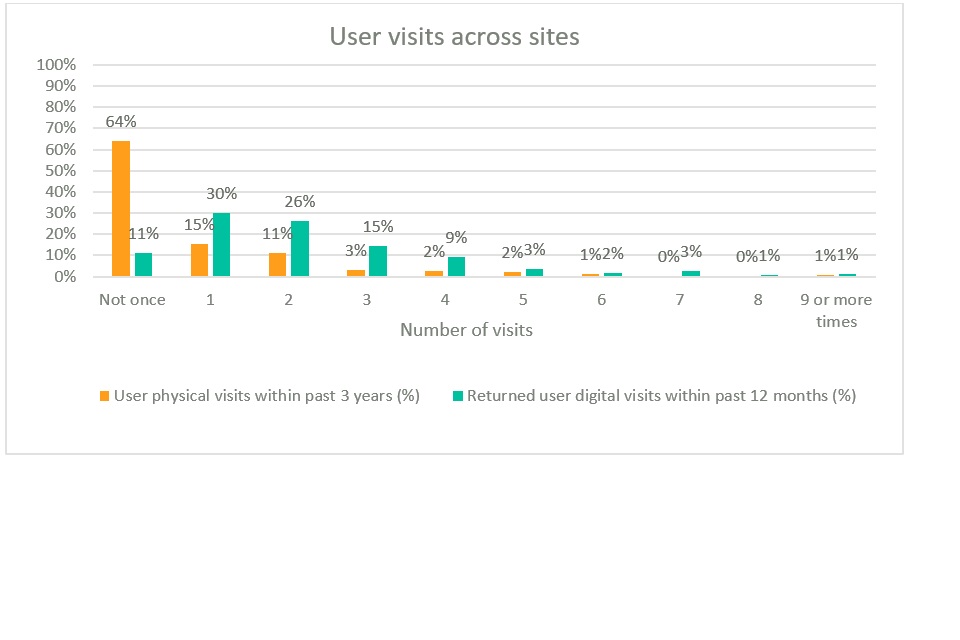

Figure 4.2 shows that 89% of respondents of those who had previously visited the website and engaged with the digital content, claimed to have had visited the institution’s website within the past 12 months on at least once occasion – a far greater than the equivalent number for even three years of physical museum visits. However, the comparison is not like with like, as a digital and physical ‘visit’ typically involve very different time commitments, with digital visits perhaps naturally resulting in more frequent but brief visits. Consistent with this, Visit Bristol[footnote 60] reports two hours as an approximate visit length to the Bristol Museum and Art Gallery, whereas website analytics suggest that digital visitors to the main website spend on average under 2 minutes on the site. This does not, however, allow for the possibility that some users download website content and engage with it offline.

Figure 4.1. Physical visitors (within the past three years) and digital visitors (no time period) across sites

Figure 4.2 Frequency of physical visits (within the past 3 years) and digital visits (with respect to returned digital users) average across sites

Future visits

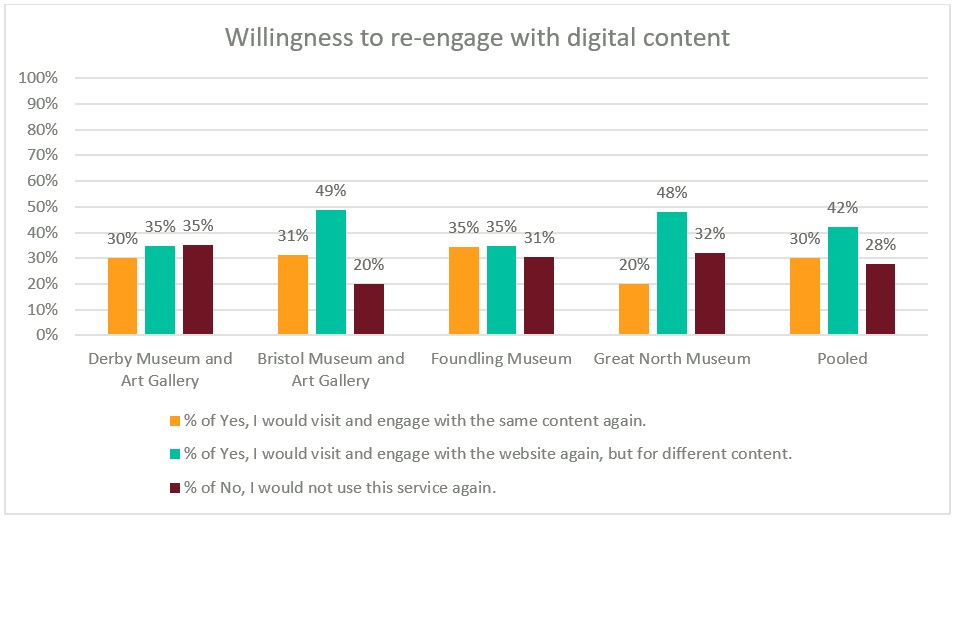

Following the contingent valuation scenario, survey respondents were asked if they were willing to revisit the digital site in the future. In total, 30% of users reported they would revisit the site and engage with the same content again, whereas 42% of users reported that they would revisit the site but would prefer to engage with different digital content (see Figure 4.3). The latter aligns with the popularity of digital subscription service market offerings, whereby new and different content is published to keep users returning to the service. Willingness to re-engage with either the same or new content was apparent across all four sites (ranging from 20% - 49%). Of the pooled sample, 28% were not willing to engage with the digital offer again regardless of whether new content was offered. This may conceivably have been due to a lack of interest in the digital offer topic (consistent also with the finding that the majority of users saying they were unwilling to pay for a physical visit to the gallery or museum said so because they were not interested in the digital content - see Table 4.16 in Section 4.5.4). It should be noted in this context that users did not select the digital offering they valued but were free to explore the website more widely.

Figure 4.3 Likelihood of digital Users re-engaging with the digital offer

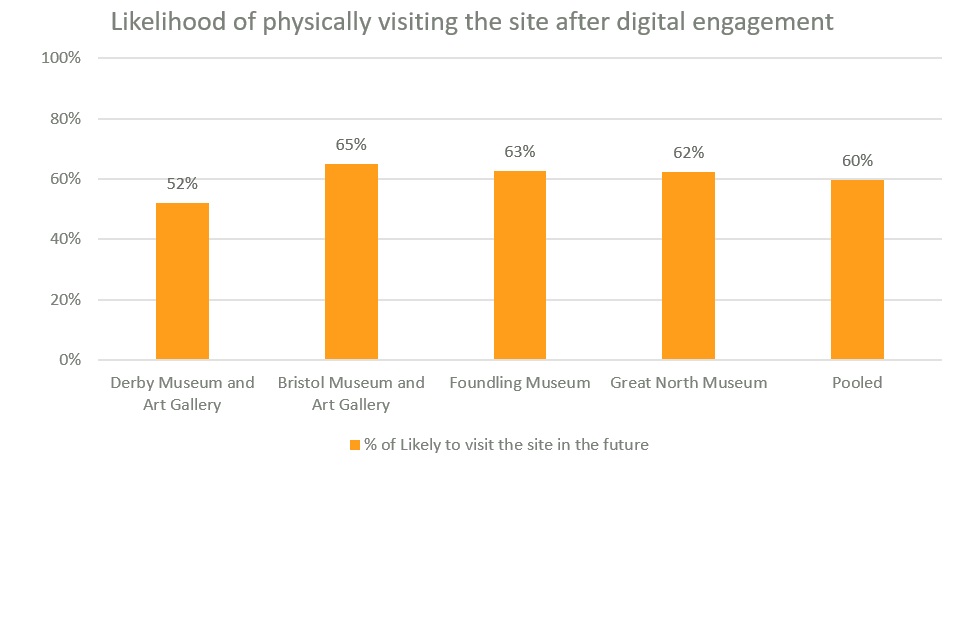

When asked whether they would be willing to physically visit the gallery or museum after engaging with and valuing the institution’s digital offer, 60% of users were willing to do so (ranging from 52% - 65% across institutions, see Figure 4.4). This is particularly notable given that 64% of the total sample had not previously visited the gallery or museum in question in the past three years and 23% of the total sample had not visited any art galleries or museums in the past 12 months. This is suggestive that the digital offering may perhaps act as a marketing opportunity for in-person visits to museums and art galleries.

Figure 4.4 Percentage of Users willing to physically visit the site in the future

5.4 WTP in theory

Using multivariate regression analysis, this research explored how individuals’ willingness-to-pay figures are associated with drivers of value, such as income and general attitudes towards arts and culture, in ways that accord with prior expectations and previous findings from the literature.[footnote 61] The following regression model was used:

WTPi = α + βXi + εi

where WTPi is the amount the individual i has stated they are willing to pay (mid-point), α is the deterministic factor and ε is the error term containing unobserved factors that determine willingness to pay. In Xi, the observed determinants of willingness to pay are controlled for, with β representing the corresponding regression coefficients.[footnote 62]

A series of multivariate regressions, reported in section 4.3.2, explore the following factors on respondent’s stated WTP:

- standard socio-demographic factors known in the literature[footnote 63] to influence WTP, including gender, age, household income, and the number of dependent children

- lifestyle and attitudinal factors, such as museum memberships, sentiments towards arts and culture (e.g., preserving museums for the appreciation of current and future generation is important), and respondent certainty about their stated WTP for the digital offer

- engagement with the good, such as the number of previous in-person visits to the gallery or museum and the number of previous visits to the digital site

- socio-economic factors, to assess the impact of broadening of audience across cultural backgrounds or ethnic groups and social classes (e.g., respondent’s school education (state funded or run), respondents’ parental educational qualifications (no degree), and respondents’ parental occupation while growing up (lower-level job class)

- COVID-19 impact factors, by exploring if the pandemic had not occurred, what impact would this have had on respondent’s WTP

WTP in principle

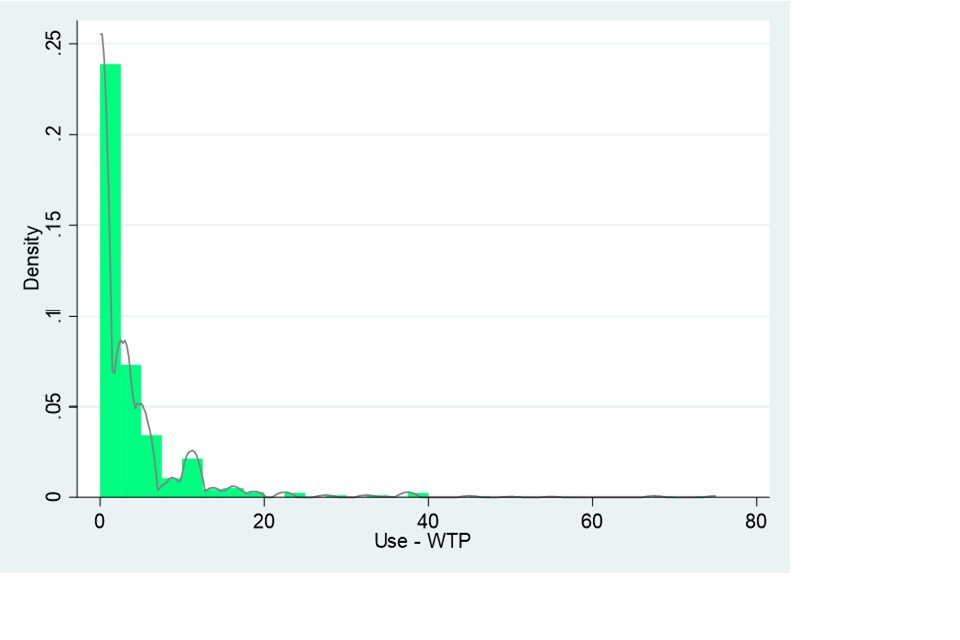

As best practice in CV surveys, a pre-selected group of values[footnote 64] were provided to survey respondent by payment cards, which elicited WTP values for the valuation scenario. Values elicited from payment cards are lower bounds of respondents’ actual WTP value for the good. Therefore, mid-points of the payment card value were chosen, and the next ascending payment card value was used to determine respondents’ actual WTP. From these mid-points, the mean WTP was calculated for the sample. The subscription fee was presented as a payment on behalf of their household as digital content is typically offered on a family subscription or household subscription. This payment vehicle of a subscription fee has been used in previous valuation research.[footnote 65] Zero as well as positive values were considered as WTP estimates as best practice in CV surveys. This ensures that the average values computed are representative of all users’ preferences. Specifically, survey respondents were presented with a series of payment values to select from if they were willing to pay in principle (i.e., ‘Yes’ or ‘Maybe’), or assigned a £0 bid if they were not willing to pay in principle.

When asked if they were prepared in principle to pay a monthly household subscription, 58% responded ‘Yes’ or ‘Maybe, and 42% were not willing to pay (see Table 4.4). This broad 50/50 split for those willing to pay and those not willing to pay is common in CV surveys. The preponderance of zero bids should not be surprising, given that so much digital content is widely and freely available on the internet. It is also a feature in the contingent valuation of the BFI’s Britain on Film’s online content mentioned earlier.[footnote 66]

Table 4.4 Monthly household subscription fee: WTP in principle

| Museum | Derby Museum and Art Gallery | Bristol Museum and Art Gallery | Foundling Museum | Great North Museum | Pooled |

|---|---|---|---|---|---|

| Yes | 18.1% | 16.7% | 19.8% | 19.2% | 17.8% |

| Maybe | 35.1% | 46.4% | 36.4% | 30.9% | 39.8% |

| No | 46.7% | 36.9% | 43.9% | 49.8% | 42.4% |

Validity testing

Validity testing, as per best-practice in CV studies (Bennett et al. 1998), includes:

- construct validity: whether the value estimates correlate in expected ways with known drivers of WTP (e.g., income, demographic factors, cultural engagement).

- content validity: whether the respondents’ answers are aligned with the key characteristics of the value that the survey is designed to elicit.

- external validity: whether the estimates align with what is known from other contingent valuations of other institutions.

Construct validity and external validity are discussed in Section 4.4.2, whereby the determinants of WTP for the digital offer for the four art galleries and museums are explored and compared with previous findings of CV of (physical) cultural goods.

Follow-up questions investigated how certain users were that they would be willing to pay for the digital offer and how consistent they believed their responses would be if they were asked the same questions in the following month. Overall, certainty was high across respondents with 56% of the sample certain they would be willing to pay their stated WTP for the digital offer. If they were asked again, 77% of users said they would provide the same answers in the following month (Table 4.5). These results provide some confidence that the users took the survey seriously and, to the best of their knowledge, provided considered responses.

Table 4.5 Users certain their responses would be consistent if asked the same survey the following month

| Museum | Derby Museum and Art Gallery | Bristol Museum and Art Gallery | Foundling Museum | Great North Museum | Pooled |

|---|---|---|---|---|---|

| Certain they would provide the same answers if asked again in one month | 79.2% | 76.0% | 72.3% | 76.6% | 76.8% |

Note that those respondents who were not certain they would have to pay (i.e., those who selected ‘I don’t believe that I would really have to pay’ as the reason behind their WTP value) were flagged for potential screen-out (see Section 6.1.2).