Guidance on the undertaking of Reviews of Public Bodies

Updated 25 April 2024

© Crown copyright 2024

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/public-bodies-review-programme/guidance-on-the-undertaking-of-reviews-of-public-bodies

Ministerial Foreword

Arm’s Length Bodies (ALBs) are vital organisations which underpin the delivery of key public services. They build transport infrastructure, inspect prisons, collect taxes, issue patents, champion our space industry, and so much more.

Just like central Government departments, the taxpayer rightly expects ALBs to deliver these services not only effectively, but efficiently as well. We must ensure that these public bodies are productive or they will be trapped in an unsustainable cycle of spending increases. Through the use of novel technologies like artificial intelligence and automation, we can unchain public and civil servants from time-consuming admin, freeing them to better help the taxpayer and deliver the best customer outcomes.

Reviews are one of our most effective levers to meet this end, helping to drive improvement and ensure public bodies deliver value for the taxpayer.

It is essential that reviews continue to identify cashable savings and go further in ensuring that we deploy best practices from across government and the private sector. This is all to ensure ALBs operate effectively; have the right governance structures in place and are fully accountable for delivering the government’s priorities. At the same time, where a body is providing first-class public service, reviews should consider how lessons can be learned from this and deployed across government.

As we progress further into the Public Bodies Review Programme, I remain grateful to review teams and lead reviewers for your hard work. I trust the programme’s updated guidance will clarify our expectations and assist you in your delivery.

The Rt Hon John Glen MP

Paymaster General and Minister for the Cabinet Office

1. Introduction

1. Arm’s length bodies (ALBs) are an important element of departmental delivery chains. There now exists a complex landscape of public bodies, with the most recent public bodies directory listing 295[footnote 1] classified ALBs, accounting for over £220 billion of taxpayers’ money.

2. Reviews are one of the principal levers by which ministers, departments, and ultimately the public can influence, and be informed about, ALBs and their sponsorship teams. While the Cabinet Office, together with HM Treasury, owns the overall governance framework for ALBs, it is for Secretaries of State to manage their ALBs, account for them to Parliament and ensure that they deliver outstanding public services.

3. ALBs are distinct from their departments, with varying levels of independence across the landscape. Despite the different degrees of independence of ALBs, permanent secretaries typically remain the Principal Accounting Officer. As set out in Managing Public Money,[footnote 2] they are responsible to Parliament for their use of public funds.

4. Ultimately, ministers are accountable to Parliament for the performance and policy framework of their ALBs and exercise control through a range of measures, including appointments to ALB boards, the sign-off of corporate and business plans, and Framework Documents. It is essential that ministers and permanent secretaries are assured that ALBs are operating effectively.

Lessons learned

5. The government’s approach to public body reviews builds on the 2010 to 2015 Public Bodies Reform Programme and the 2015 to 2020 tailored review programme. Departments reported that benefits of the tailored review programme included:

- greater flexibility and closer working between the department and the body being reviewed;

- the focus on governance, and related recommendations, strengthened internal assurance; and

- the reviews served as a health check for their organisation, to help support departmental findings and actions being taken to resolve issues.

6. However, the tailored review programme had a number of weaknesses that are addressed in the new programme. These included:

- an overly narrow focus on governance as opposed to wider priorities, such as efficiency and effective delivery;

- a tendency to focus on the ALB’s features, rather than the nature of the relationship between the ALB and the sponsor department;

- the raising of issues already identified by the departments, rather than adding value by diagnosing unforeseen risks and issues; and

- only 34%[footnote 3] of the planned ALB reviews were undertaken between 2016 and 2020.

7. This reviews programme is designed to meet the government’s vision of public bodies that are accountable, effective, efficient, and aligned to the government’s priorities. It features several distinct differences to the tailored review programme:

- Broad focus with clear expectations: With new requirements covering governance, accountability, efficacy, and efficiency of ALBs — setting minimum expectations. These reviews are expected to address both the ALB and how the department sponsors it.

- Proportionate and flexible by:

- focusing on those bodies of highest risk as determined by their Principal Accounting Officer (PAO) and ministers; not ‘reviews for reviews’ sake’;

- allowing the review to reflect the distinct characteristics of the body through a methodology and approach that can be adapted;

- utilising a new self-assessment tool to help departments determine the depth of their review; and

- departments, who are expert, will lead reviews. This will inject greater pace by removing the Cabinet Office from unnecessary process, such as the sign-off of terms of reference.

- Independent challenge: Each review will be led by an independent lead reviewer. The Cabinet Office’s Public Bodies Team maintains a pool of lead reviewers to support departments.

8. Departments are also encouraged to both utilise data and consider their delivery system as a whole:

- Data: It is important that decision-making is informed by robust, high-quality data. Reviews should be evidence rich in themselves and where possible, recommend improvements to enable public bodies to better use data.

- Systems thinking: The department should map its delivery system in order to assure itself that the changes it makes through a review improve the system as a whole for the public.

- Shared best practices: Reviews should provide an opportunity to ensure public bodies are following best practices from within a department and across Whitehall. Likewise, where there are lessons to be learned from a public body, reviews should seek to disseminate these more widely across government.

2. Purpose of this Guidance

9. The Cabinet Office has developed this guidance to provide information to sponsor departments, ALBs, review teams, and lead reviewers.

10. The guidance has been developed with the understanding that the public body landscape across the UK government is varied. Specific elements of the guidance may need to be adapted accordingly.

11. Departments are strongly encouraged to use this guidance when reviewing public bodies outside of the formal ALB classification[footnote 4]. Such bodies should be reviewed by departments with the aim of identifying an appropriate administrative classification where possible. Departments should set out why any high-risk unclassified bodies have not been reviewed.

12. Reviews are likely to vary in size and scale and the approach outlined in this guidance supports such proportionality and flexibility. The reviews can range from light-touch exercises largely undertaken via a self-assessment to a team of people working to support a lead reviewer on full-scale review.

13. This guidance should be read in conjunction with the:

- Requirements for Reviews of Public Bodies; and

- Self-Assessment Model.

14. Departments and ALBs should refer to these documents, published separately, when undertaking a review.

3. Purpose of ALB Reviews

15. An ALB review must first and foremost assure the public, ministers, and the Principal Accounting Officer (PAO) that the ALB’s function remains useful and necessary.

16. Secondly, a review should assess whether there are more efficient and effective alternatives to deliver the government’s objectives. This can include merging the body with a similar body and closing the body and bringing its functions back to the department.

17. A review should provide an opportunity for departments to ensure they are satisfied that the ALB is operating with a clear purpose and using an appropriate delivery model.

18. Reviews should consider whether decisions are appropriately being taken by the ALB or whether those decisions would be best taken by ministers in the department. When answering these questions, reviewers should at all times bear in mind the government’s ‘three tests’ for the existence of a public body[footnote 5].

19. An ALB review should result in recommendations that address these questions. Recommendations should be tangible and provide assurance to ministers and the public that the ALB is best placed to deliver the government’s objectives.

20. Where it is agreed that an ALB should be retained, the following must be reviewed:

- the ALB’s capacity to deliver more effectively and efficiently, including identifying the efficiency savings;

- When conducting a review, lead reviewers are required to identify where savings to Resource Departmental Expenditure Limits (RDEL) of more than 5% can be made.

- It is expected that this target is met where there is not an equivalent pre-existing efficiency savings target set for the body in question.

- Actions to meet the efficiency target must be reflected in the review recommendations and recorded and quantified in the published review report.

- As with all review recommendations, ministers are able to accept or reject the recommendation.

- Where agreed as a recommendation, the target of more than 5% should be achieved by the body within 1-3 years.

- When conducting a review, lead reviewers are required to identify where savings to Resource Departmental Expenditure Limits (RDEL) of more than 5% can be made.

- the performance of the ALB, including its contribution to the government’s objectives, and the processes in place for making such assessments;

- the control and governance arrangements in place to ensure that the ALB and its sponsor are complying with recognised principles of good governance and meeting their legal requirements; and

- further details on this efficiency requirement can be found at paragraphs 86 to 92.

21. It is for departments to consider how best to structure and carry out these reviews and act on their recommendations, in accordance with the principles set out in this guidance.

Role of the Cabinet Office in ALB reviews

22. The Cabinet Office will provide advice and challenge to departments by:

- overseeing the overall programme of reviews, setting direction for it, and monitoring its effectiveness;

- challenging departments if it believes that high-risk bodies are not being prioritised for review;

- maintaining tools and guidance to support departments in undertaking their reviews, including the Cabinet Office’s lead reviewer pool;

- looking for systemic issues by monitoring data gathered from reviews. For example, departments will share Self-Assessment Models; and

- requiring departments to keep it updated on the commencement and progress of reviews and the implementation of recommendations.

4. Scope and Approach

23. The public bodies directly in scope for this guidance are those that have been administratively classified by the Cabinet Office[footnote 6] as ALBs:

- Non-Departmental Public Bodies (NDPBs);

- Executive Agencies (EAs); and

- Non-Ministerial Departments (NMDs).

24. However, departments can apply the principles within this guidance to any and all of their public bodies that they may wish to review.

25. When conducting a review of a public body classified to the Central Government sub-sector by the Office for National Statistics (ONS) but not administratively classified as an ALB, the departmental review must consider the appropriate administrative classification for the body.[footnote 7]

26. Departments should engage the Cabinet Office on the appropriate classification and approval process. The Cabinet Office expects departments to carefully consider if currently unclassified bodies should be classified as ALBs, in line with the Public Bodies Handbook - Part 1, Classification of Public Bodies: Guidance for Departments (PDF, 888KB).

27. If departments review a public body that holds more than one administrative classification, such as NMDs that are also EAs, departments should consult with the Cabinet Office’s Public Bodies Team to examine if the body still requires more than one classification given actual business practices and if it causes any governance or funding problems. A single classification should be adopted where possible.

28. In limited cases, departments may wish to review public bodies that are awaiting classification by the ONS. In such cases, departments should engage HM Treasury and the Cabinet Office.

Timing

29.Proportionality is a central part to this programme and department’s ministers and their Principal Accounting Officer (PAO) should determine the most appropriate frequency of review of their ALBs.

30. The government recognises the National Audit Office’s (NAO’s) criticism[footnote 8] that previous review programmes have not been sufficiently proportionate and have failed to meet their ambition of reviewing every ALB within a Parliament. That is why this reviews programme requires departments to confirm to the Cabinet Office and HM Treasury a prioritised list of ALBs for review, based on factors including their assessment of risk that the body poses (see paragraph 133). The government wants to invest scarce resources in reviews that will deliver impactful change for the citizen, not reviews for reviews’ sake.

31. The Cabinet Office and HM Treasury reserve the right to challenge the department’s proposed prioritisation of reviews. For example, a low-risk ALB must not be prioritised for review over a major delivery body with significant risks in the belief that doing so demonstrates swift progress.

32. The Cabinet Office recognises that ALBs may also be subject to other forms of scrutiny, in which case the PAO and minister(s) may wish to take that scrutiny into account when prioritising their bodies for review.

33. It remains government policy that a new ALB should be reviewed between 18 to 24 months after the start of full operations. New bodies should be subject to a full-scale review (see paragraphs 129 to 131 for further details).

34. Departments may consider clustering reviews and reviewing more than one body at the same time. Clustering reviews can be more efficient and are one way that Departments can reduce duplicative work.

35. The clustered bodies should be related in some way. Departments have previously clustered bodies that deliver similar services. For example, the Ministry of Defence reviewed the National Army Museum, the National Museum of the Royal Navy and the Royal Air Force Museum as a cluster. Departments may also wish to cluster bodies that contribute to a shared system or bodies that are being considered for merger. Departments must, however, ensure cluster reviews remain proportionate to the body or bodies in question and that the reviews do not become unwieldy and cause unnecessary delays to the progress of the reviews.

36. It may also be appropriate to consider the timing of the review with regard to any forthcoming relevant public appointments.

Pace

37. Reviews should be completed thoroughly and rigorously, but also as quickly as possible to minimise the disruption to a department’s business. The review of a smaller public body could be completed within a month, and even major reviews should aim to take no more than six months.

38. In order to complete the reviews at an appropriate pace, departments should allocate sufficient resources to them to enable them to be delivered within the agreed timeframe. Investing in sufficient capable resources can lead to recommendations that far outweigh the cost of the review.

39. The Cabinet Office will no longer approve the terms of reference and final report prior to publication, to both empower departments and increase pace.

Inclusivity

40. Reviews should be open and inclusive. The department and ALB should welcome the opportunity for independent challenge and support the lead reviewer and their team in accessing the data they need. Establishing a positive ‘one team’ culture during a review can help to ensure that recommendations, and their implementation, have buy-in.

41. In addition, key stakeholders, including the public in the case of some reviews, should have the opportunity to provide input to the review where relevant and appropriate (see paragraphs 163 to 167).

42. When conducting a review, the sponsor department and review team must comply with the Public Sector Equality Duty, in line with guidance from the Equalities Hub and the Government Equalities Office. This means:

- Lead reviewers should have due regard to the equality impact of any recommendations of the review on the staff of the body or the customers who benefit from the public services that the body delivers.

- Review teams should seek legal advice where appropriate and necessary when considering equality impacts.

- Review teams should include an acknowledgement that an equality impact assessment (or such other record of compliance with PSED as appropriate) has been done in the review’s final report

- The sponsor department should retain a record of the equality impact assessment, including any associated data analysis

- Sponsor departments and review teams should ensure that complying with the Equality Duty should not lead to disproportionate burdens on the public sector or their private sector or voluntary sector contractors. The cost of disproportionate burdens ultimately falls on the taxpayer.

43. Departments should also consider whether and, if so, how, they might involve Parliament in the review process. They may wish to announce the start and conclusion of the review by way of a written ministerial statement (WMS) and alert the relevant committee(s) when starting the review.

44. Departments may wish to limit the number of statements they lay by making an annual announcement setting out the reviews they propose to deliver throughout the financial year.

45. In keeping with the core principles underpinning all reviews, engagement should be proportionate, timely, and provide clear value for money for users and taxpayers.

Relationship with existing guidance

46. The tools provided for departments to undertake these reviews do not replace existing guidance for ALBs, unless this is specifically stated. The Public Bodies Review Programme’s tools and guidance primarily aim to consolidate and collate existing guidance and departments should consult all relevant existing guidance where appropriate for the review in question. This might include:

- Managing Public Money

- Arms Length Body Sponsorship Code of Good Practice

- The Government Efficiency Framework

- Public Value Framework (PDF, 766KB)

- The Orange Book: Management of Risk – Principles and Concepts

- Public Bodies Handbook – Part 1. Classification of Public Bodies: Guidance for Departments (PDF, 888KB)

- Public Bodies Handbook – Part 2. The Approvals Process for the Creation of New Arm’s-Length Bodies: Guidance for Departments (PDF, 843KB)

- Public Bodies Handbook – Part 3. Executive Agencies: A guide for departments (PDF, 843KB)

- Non-Departmental Public Bodies: Characteristics and Governance

- 12 Principles of Governance for all Public Body NEDs

- Code of Conduct for Board Members of Public Bodies (PDF, 437KB)

- Charity Commission guidance

- The Financial Reporting Council’s UK Corporate Governance Code (PDF, 269KB)

- Corporate governance in central government departments: Code of Good Practice

- Accounting Officer System Statements: Guidance (PDF, 477KB)

- Shared Services Strategy for Government

47. This list will be kept under review by the Cabinet Office.

Functional Standards

48. Functional standards exist to create a coherent, effective, and mutually understood way of conducting business within government organisations and across organisational boundaries. The functional standards outline the requirements for each type of functional work, covering governance, roles and accountabilities, and the practices required for the specific function.

49. There are 14 functional standards, covering the following areas:

- GovS 001: Government functions

- GovS 002: Project Delivery

- GovS 003: Human Resources

- GovS 004: Property

- GovS 005: Digital

- GovS 006: Finance

- GovS 007: Security

- GovS 008: Commercial

- GovS 009: Internal Audit

- GovS 010: Analysis

- GovS 011: Communication

- GovS 013: Counter Fraud

- GovS 014: Debt

- GovS 015: Grants

50. These standards provide a stable basis for assurance, risk management, and capability improvement in order to support value for money for the taxpayer. Further information can be found in the guide to functional standards.

51. A review should look to ensure that the requirements within the functional standards are in place within the ALB and then look to highlight areas where these practices can be strengthened. To do so, the department and ALB will need to take into account where the functional standards apply to the ALB.

52. Questions that should be considered when using the functional standards include:

- Does the ALB have a clear understanding of how well it is meeting the functional standard?

- How well defined are the areas to be prioritised for improvement?

- How effective are the plans to drive continuous improvement against the standards?

53. When undertaking a review, departments will want to consider how any assessment of the ALB against the functional standards can be used as part of the evidence base for the review. Functional leads in the department should have undertaken assessments of the ALB against these functional standards and will be able to provide important evidence to support the review.

54. For further information on each individual functional standard and how to apply them, please refer to this page. If you have any comments or questions, please contact standards@cabinetoffice.gov.uk.

Public Sector Research Establishments (PSREs)

55. Public sector research establishments (PSREs) are a diverse collection of public bodies carrying out research. This research supports a wide range of government objectives, including informing policy making, statutory and regulatory functions, and providing a national strategic resource in key areas of scientific research. They can also provide emergency response services. They interact with businesses around a wide array of innovation-related functions.

56. When conducting reviews of PSREs, departments should consult the PSRE Value Framework. This is a tool developed by the Government Office for Science through consultation with PSREs, departments, and external organisations that will support departments in conducting effective reviews of PSREs. It will enable departments to understand a PSRE’s performance and value for science and technology, and to think critically about how they could be better utilised. This framework should be used during the review process to ensure a consistent standard of reviews of PSREs across government.

57. This framework is to be used alongside the methodology described in this review guidance and other Cabinet Office guidance. Given the nature of work conducted by PSREs, reviewers should consult departmental Chief Scientific Advisors (CSAs) when scoping the review to ensure the right aspects of PSRE activity are considered.

58. The Government Office for Science can advise review teams on conducting reviews of PSREs. For more information, please contact rdstrategy@go-science.gov.uk.

Scientific Advisory Councils (SACs)

59. Scientific Advisory Committees or Councils (SACs) help government departments (and other executive public bodies) access, interpret, and understand the full range of relevant scientific information and to make judgements about its relevance, potential, and application. Such committees give advice on a very wide range of issues, ranging from the food we grow and eat, to the quality of our environment, the safety of our roads and transport, and the design of buildings we live and work in. They review, and sometimes commission, scientific research and offer independent expert judgement, including highlighting where facts are missing and where uncertainty or disagreement exists. SACs may be required to provide advice on the state of current knowledge, the application of information to specific issues, or both.

60. Those SACs that are NDPBs are subject to review. The Government Office for Science should be consulted as part of reviews of such advisory NDPBs, at a minimum, as part of the development of the terms of reference of the review and then later in the process once emerging recommendations are in place.

61. Further advice on the operation of Scientific Advisory Councils is available in guidance maintained by the Government Office for Science, including the principles of scientific advice to government and the Code of Practice for Scientific Advisory Committees.

Shared Services (PDF, 1,632KB)

62. The Shared Services Strategy brings together the core functions of a business into a single simplified centre to save time, cut back-office red tape, and offer better value for money to the taxpayer. This new streamlined approach allows for higher productivity and standardisation of business needs at a lower cost and with a better user experience and accessibility.

63. ALBs are within the scope of the Strategy and are expected to join their sponsoring department’s Shared Service Centre, as set out in the Shared Services Strategy for Government.

64. ALBs not joining the Shared Service Centre in the immediate future, for example, due to contractual commitments, are expected to progress with alignment to Strategy workstreams in preparation for joining their Centre. These workstreams include alignment to global processes and standards, data convergence, process transformation, and performance and quality.

65. Reviews should consider ALB alignment to the strategy and roadmap for the ALB to join its Shared Service Centre.

Devolution and strengthening the Union

66. It is essential to have fully considered the extent to which an ALB’s functions are directly or indirectly delivered in a devolved context.

67. In the government’s response to Lord Dunlop’s review of how the UK government and devolved administrations can work more effectively together on behalf of all citizens, the government committed to helping public bodies work in a way that represents and strengthens the UK.

68. Review teams can draw upon support from the UK Governance Group (UKGG) or the Northern Ireland Office to better understand devolution issues in the policy and delivery areas in question. They can also access the Devolution Toolkit.

69. Understanding the remit and reach of the body, dependencies, and stakeholders within each of the UK’s nations should be a fundamental part of scoping and undertaking the review.

5. Key Principles

70. As described earlier, this new programme of reviews has learnt lessons from the previous review programmes and, therefore, has been designed to meet the following principles:

- Useful to both the sponsor department and ALB.

- Informed by relevant expertise.

- Proportionate.

- Constructively critical, rigorous and open.

- Realistic.

71. Useful to both the sponsor department and ALB: Reviews should generate benefits for the ALB, department, central government, and ultimately the public and end users of the service. They should identify where elements need strengthening and put in place constructive means to do so.

72. The review should not be seen as a punitive measure or an exercise with predetermined aims, but rather a collaborative exercise to ensure that the ALB and the department are working effectively together.

73. Informed by relevant expertise: Reviews should be led by suitably qualified lead reviewers and supported by departments. Departments will need to ensure that the relevant spending team at HM Treasury is engaged when appropriate. Departments may wish to consider the merits of bringing in independent expertise, for example, from the private sector. In particular, departments should look to include audit experience in their review teams. Full details of the skills needed in a review team can be found at paragraphs 121 to 124.

74. Departments should ensure they have the right expertise to drive efficiency within the ALB. Even if the review itself does not drive monetised savings, it should identify processes and structures that could.

75. In the case of clustered reviews, where bodies are sponsored by different departments, consideration should be given to which department should lead and how best to involve the other department(s).

76. Proportionate: The new review programme provides a set of consistent requirements that set a minimum benchmark for all ALBs and departments to meet. Beyond that, reviews should be proportionate to the ALB.

77. Reviews should be aligned to wider policy or strategic reviews and support commitments set out in the government’s manifesto, Outcome Delivery Plans[footnote 9], and the Spending Review.

78. Constructively critical, rigorous, and open: Reviews should be constructive and challenging, surfacing issues and probing for solutions. It is expected that, where a review identifies the need for change, recommendations are transformative and bold where they need to be. Reviews should solicit input from stakeholders — including the public, where appropriate.

79. The ultimate aim of the review is to focus on delivering tangible recommendations that provide assurance to ministers and the public that the ALB is best placed to deliver public services and goods.

80. Realistic: The reviews should be focused on issues the ALB/department can control and put right, rather than comment on wider issues. This principle should manifest itself in realistic and proportionate recommendations set within an achievable timeline.

6. Requirements That Underpin ALB Reviews: Governance, Accountability, Efficacy and Efficiency

81. The new review programme is underpinned by a set of requirements for use in reviews which outline the minimum expectations for departments and ALBs, and some indicators of good practice. They are split into the following quadrants:

i. Efficacy: This quadrant outlines the expectations on form and function, thereby ensuring that the ALB meets the conditions to be an ALB, with a clear purpose, in the correct delivery model. It also sets out the expectations that the ALB performs effectively and delivers services that meet the needs of citizens.

ii. Governance: This quadrant sets out the expectations to be met by ALB boards and their supporting committees.

iii. Accountability: This quadrant sets out expectations on the lines of accountability and communication between departments and ALBs, and the support and challenge offered to ALBs via the critical ‘sponsoring’ relationship departments have with their ALB.

iv. Efficiency: This quadrant sets out the expected financial management processes in line with current guidance, and outlines the expectations for the identification of cashable efficiency gains that can be made through a change in practices, for example, by digitisation.

82. The requirements include the fundamental expectations ALBs and departments are expected to meet. They are in place to ensure that ALBs are operating in accordance with guidance and legal requirements.

83. These requirements should be used by departments to drive improvements in ALBs and departments. The requirements should also inform the terms of reference of the review. The requirements will be managed by the Cabinet Office and will be reviewed as appropriate.

84. The Self-Assessment Model (SAM) has been designed to align with these same quadrants and should be undertaken at the beginning of each review. Paragraphs 142 to 154 provide more information and should be read alongside the SAM itself.

85. There is additional guidance for using the requirements when undertaking a full-scale review of an ALB at the end of the Requirements document.

Further Guidance and Clarification on Efficiency

86. As per paragraph 20, when conducting a review, lead reviewers are required to identify where savings to Resource Departmental Expenditure Limits (RDEL) of more than 5% of 2022/23 budgets in nominal terms can be made for an average review.

87. Where a body has an existing RDEL savings target from Spending Review 2021 (SR21) this may be counted towards the review’s savings target, as long as this figure is stated explicitly at the review’s outset.

88. This target applies to a body’s RDEL budget net of any non-exchequer income. The target does not explicitly include Annually Managed Expenditure (or ‘AME’) or Capital Delegated Expenditure Limits (or ‘CDEL’), but lead reviewers should explore the potential for savings where bodies’ operating expenditure is classified as AME or CDEL and more generally seek to maximise organisational efficiency regardless of the accounting classification of expenditure.

89. Real-terms effects on budgets due to inflation do not count towards the target.

90. Savings must be cashable to count towards this target with the following principles applying:

- They should be accurately calculated. The calculation is likely to be based on baseline cost information and a counterfactual spending profile (involving estimates and assumptions).

- They should release cash, net of costs. Savings must elicit cash from a body’s budget without causing consequential costs elsewhere in the body, its parent department, other government departments, local or devolved government.

- They should be sustainable and should not be reallocating or deferring costs to future years.

- The nature and calculation of savings should be readily understood, calculated with quality data, and likely to be seen as reasonable and robust by an impartial third party (such as the NAO and GIAA).

- The nature of the saving should be clear, for example identifying savings that relate to procurement, or pay. The underpinning information should have robust data and evidence.

91. This target applies to each review individually and only to full-scale (not SAM-only) reviews. However, review teams should assess existing efficiency and savings commitments as part of the SAM and consider this when deciding whether to take a body to full-scale review (paragraph 155 onwards).

92. Departments should use the proceeds from any savings to support the delivery of departmental priorities, either within the body under review or in the wider department. Departments should notify their HM Treasury spending teams about the size of savings identified and how any resulting proceeds will be used.

7. People: Ministers, Principal Accounting Officers, ALB Leadership, Lead Reviewers, and the Review Team

93. It is the responsibility of departments to resource reviews appropriately. While departments will be responsible for reviews, the review leadership will be external to the ALB under review.

94. Reviews will be led by an independent lead reviewer and will be supported by a departmental review team, who are independent from the team sponsoring the ALB.

Ministers

95. Ministers are ultimately accountable for their departments’ public bodies and will want to define their role in the review process. Generally, this will involve:

- deciding which bodies are reviewed and when by writing an annual prioritisation letter to the Minister for the Cabinet Office and Chief Secretary to the Treasury;

- deciding on and appointing the lead reviewer;

- deciding whether a body merits a full-scale review or not;

- sending out to the lead reviewer the commencement letter ahead of a full-scale review setting out the need for and focus of the review (this may instead be done by the PAO or senior sponsor);

- reviewing the terms of reference of a review;

- requesting a challenge panel is established;

- nominating members to the challenge panel, alongside the PAO and lead reviewer;

- approving all challenge panel members from outside the Civil Service;

- accepting or rejecting the recommendations suggested; and

- holding the department and public body to account for the implementation of the recommendations.

Principal Accounting Officers

96. Principal Accounting Officers (PAOs) are responsible for managing public money and risk. While they delegate these responsibilities to the ALB’s Accounting Officer, they retain ultimate accountability. The PAO’s role in the review process is to advise their ministers:

- on which bodies should be prioritised for review;

- of suitable lead reviewer candidates;

- on the depth of review required;

- whether to accept recommendations or if to reject with good reason, with particular regard to value for money; and

- to ensure timely implementation of recommendations.

97. The PAO will ensure there is suitably skilled resource to support the lead reviewer via the review team and support from the functions. Lastly, the PAO is encouraged to ‘set the tone’ for the review so that the department and ALB work constructively together to support the lead reviewer.

Senior sponsors of an ALB

98. Senior sponsors are normally appointed by and act on behalf of the PAO. They are responsible for the routine oversight of an ALB and are normally supported by a team. The senior sponsor’s role within the review process is to:

- engage with the chair and board of the ALB to inform them of any forthcoming review and its rationale;

- draft the commencement letter ahead of a full-scale review setting out the need for and focus of the review;

- comment on any proposed terms of reference for the review to ensure areas for consideration are captured accurately;

- take a proactive approach in ensuring there is dialogue between sponsor team, review team, and ALB, facilitating proper engagement by all during the review process;

- if needed meet with both the ALB and lead reviewer to discuss any issues or where there may be a delay with the provision of evidence in a timely manner and support a resolution to this;

- review the report and recommendations, working closely with the PAO and minister to provide a response to the lead reviewer (paragraph 187 to 191); and

- work with ALB as ‘one team’ after the review in ensuring that recommendations are implemented in a timely manner.

ALB leadership

99. The chair of the ALB’s board should be informed about any proposed review. In particular, the chair and their board (including the executive, where the board has one) will have the opportunity to:

- ensure a collaborative and open approach is taken towards the review and that the lead reviewer and the review team are provided with all the information they need and ensure proper resource on the part of the ALB to facilitate this in a timely manner;

- comment on the proposed terms of reference for the review;

- meet regularly with the lead reviewer and ensure their board is supportive and open in any interviews the lead reviewer requests;

- comment on the proposed recommendations from the review; and

- work with the department as ‘one team’ to implement recommendations in a timely manner.

Lead reviewers

100. Lead reviewers are responsible for ensuring a proportionate and rigorous review of the ALB is conducted and are ultimately accountable for the report and recommendations of the reviews they lead.

101. It is important for lead reviewers to be both objective and perceived as objective. They will provide assurance to ministers, the department and the ALB that a review has been conducted with a level of independence and that, as a result, recommendations are produced that will facilitate the continuous improvement of the ALB where necessary. Whilst retaining independent ownership of reviews and reports, lead reviewers should engage openly and transparently with departments and ALBs.

102. The department should assure itself that the lead reviewer is suitable for the role.

103. The lead reviewer should be sufficiently independent to enable objective analysis of the ALB and department during the review. This is best ensured by the lead reviewer being external to both the sponsor department undertaking the review and the ALB being reviewed.

104. The independence and objectivity of the lead reviewer are ultimately a matter for the judgement of the reviewing department’s ministers, and it is for departments to manage this risk appropriately.

105. Lead reviewers can be sourced from a pool held by the Cabinet Office (see below for more details).

106. Departments can also appoint a lead reviewer independent of this pool in order to use particular skills or experience which may be pertinent to the review of a specific ALB. Departments should submit possible candidates to their ministers, who will have the final say on who should be appointed as lead reviewer.

107. Departments may appoint more than one lead reviewer. This approach can broaden the skills and experience available to the review team. If a department appoints multiple lead reviewers, it must ensure that it is clear which reviewer is ultimately responsible for ensuring that the review is proportionate and rigorous and will be accountable for the final report and recommendations.

108. Departments should ensure that lead reviewers are appointed using an appropriate mechanism. As it is for the minister to decide who to appoint, and because the lead reviewer is appointed to fulfil a short term advisory role, a direct ministerial appointment is often used. However, this is not necessarily the most appropriate mechanism in every case. For example, a direct ministerial appointment cannot be used to move civil servants between departments. Other possible mechanisms include loan, fixed-term contract, and informal personnel sharing between departments. Departments should seek advice from their HR function on the best mechanism to use in a particular situation. They should seek advice from their public appointments team if they are considering a direct ministerial appointment.

Cabinet Office lead reviewer pool

109. The Cabinet Office’s Public Bodies Team holds a pool of potential lead reviewers. Individuals in the pool are willing to undertake this role. They have been nominated by other government departments as suitable against the criteria set out by the Cabinet Office in the role specification.

110. When a department wishes to use the pool to select a lead reviewer, they should contact the Cabinet Office Public Bodies Team at publicbodiesreform@cabinetoffice.gov.uk for access.

111. The pool will contain the names and relevant details of the potential lead reviewers and contact details of the department that nominated them. When selecting reviewers from the pool, the reviewing department will coordinate contact with the lead reviewers via the nominating department.

112. It is then advised that the reviewing department conduct any further conversations or checks on shortlisted lead reviewers ahead of advising on the appointment. It is the reviewing department’s responsibility to ensure they have an appropriate lead reviewer.

113. The Cabinet Office Public Bodies Team will seek to ensure that the pool is kept up to date annually and will, as part of the annual prioritisation process outlined in paragraphs 131 to 140, ask departments to confirm if they would like any individuals to be removed from the pool and to submit new candidates.

114. As the Public Bodies Review Programme progresses, the Cabinet Office will invite feedback from departments on the pool and on the role of lead reviewers.

Review team

115. The lead reviewer will be supported by a review team. It is the responsibility of departments to adequately resource their reviews and to ensure the review team has the appropriate level of experience to identify efficiencies.

116. Departments will select their own review team, and the size of the review team will therefore be dependent on the nature of the ALB under review. While there is no one-size-fits-all model for resourcing a successful review team, non-exhaustive options for this may include via dedicated standing resource, project-based temporary resource including functional specialists, and secondment from ALBs (though not the body under review).

117. At the outset of a review, lead reviewers should discuss with the sponsoring department the support that is available to them beyond their review team, including the use they can make of departmental expertise in carrying out a review.

118. If a lead reviewer identifies a skills or experience deficit in their team, either before or during a review, they should work with the sponsor department to source relevant resource. Where possible, departments should accommodate reasonable requests for additional support, including through the deployment of experts from within the departmental experts and recruiting additional lead reviewers. Review teams should work with the Cabinet Office’s Public Bodies Team where they believe central functional expertise is required to address a question emerging from a review.

119. The departmental review team should be independent of the ALB and its sponsoring team. This independence will allow for the review to consider the sponsor relationship between the ALB and the department more objectively.

Roles within the review team

120. The capacity and capability of the review team is for the department to decide based on the complexity and level of risk posed by the body. However, for a medium-sized body that poses medium risk, the standard roles expected in the review team may include:

- head of the review team;

- analysis; and

- secretariat.

Capabilities of the review team

121. For a high-profile body, the review team may be led by a senior civil servant. They would support the lead reviewer to manage complex relationships with senior officials within the department and the ALB, as well as ministers. For lower-risk and less high-profile bodies, the Principal Accounting Officer may be satisfied that a smaller and less senior review team is sufficient.

122. The capabilities needed within the review team are likely to include:

- an understanding of public finance / Managing Public Money and the Public Value Framework;

- analysis and the understanding of complex evidence bases (for example, to review-relevant ALB data);

- legal issues (if the body has a statutory footing) or other legal duties it must discharge;

- an understanding of good governance principles; and

- strong stakeholder management skills.

123. The review team should be supported by the department’s functions as appropriate.

Responsibilities of the review team

124. The responsibilities of the review team will vary depending on the review but may include the following:

- accessing the lead reviewer pool and shortlisting lead reviewers;

- seeking approval for the different stages of the review via submissions to ministers, for example, for lead reviewers;

- supporting the handling of the review within the department, ensuring that the PAO, ministers, and the ALB are engaging, as needed, with the review;

- onboarding the lead reviewer (for example, arranging IT if needed);

- ensuring the lead reviewer is briefed on the background and context of the ALB;

- ensuring appropriate engagement between the lead reviewer and public body, key stakeholders, and other key officials;

- arranging interviews for the lead reviewer with relevant stakeholders and collating input from stakeholders, including the public, where relevant;

- ensuring that the review is done in a timely manner and following the Cabinet Office’s public body reviews guidance;

- supporting the lead reviewer in identifying opportunities for savings;

- evidence gathering and analysis and, if required, supporting the mapping of the wider delivery system; and

- assisting with the writing of the final recommendations and report.

Review team’s relationship with the ALB and sponsor team

125. The review team should build a trusting and effective relationship with both the ALB sponsor team and the ALB itself. It is important that there is open, two-way discussion between the department and the ALB. The review team must be open and transparent with the ALB, explaining the rationale for its requests and actions, and should expect the same in return.

Role of the ALB in relation to the review team

126. The ALB should work in an open and transparent manner with the review team to ensure all relevant data is shared in an ‘open book’ approach to its performance and finances.

Further information on the review team

127. Reviews will vary considerably in terms of scope and scale. Departments will want to consider the role of the review team, and the roles within it, in line with their ambition for the review (for more information on this, see paragraph 115 onwards).

8. Process and Methodology

128. This section outlines the guidance for how to undertake a review. For guidance on timing, pace, and inclusivity of engagement, please refer to Chapter 4: Scope and Approach (paragraph 23 onwards).

Recommended review process

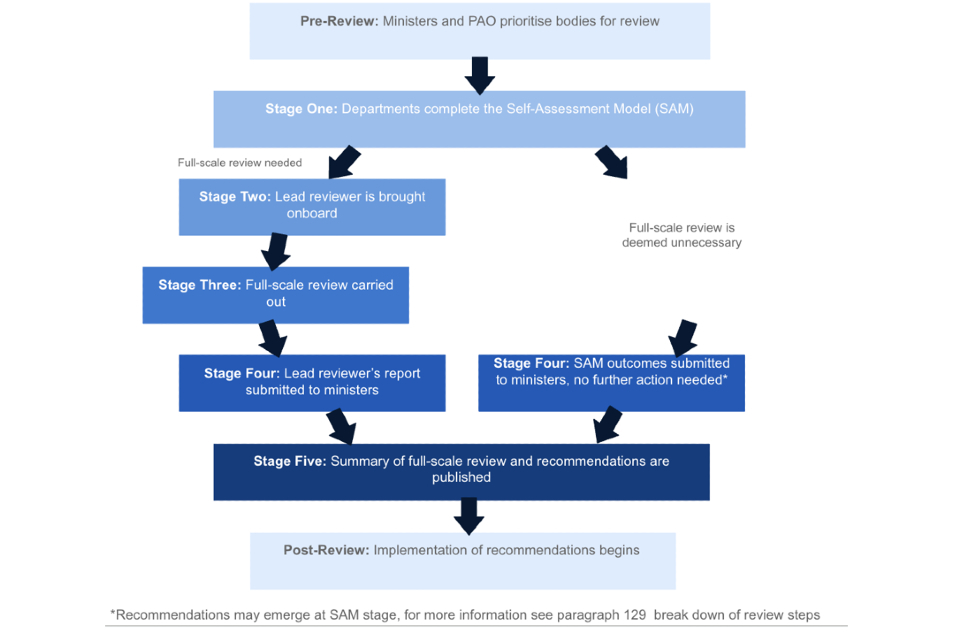

129. Departments should review this guidance and consider the best process for setting up a review of an ALB. The Cabinet Office suggests the following five stage outline. This outline may be adapted as appropriate:

130. The stages can be carried out as follows, along with indicative timescales:

Stage 1 — Self-assessment:

A self-assessment should be conducted. Depending on the outcome of the self-assessment and any other relevant factors, a decision will be taken by the responsible sponsoring minister, with a view from the Principal Accounting Officer (PAO), on whether:

i. to move to Stage 2 and appoint a lead reviewer; OR

ii. to move straight to Stage 4

Stage 1 should take no more than a month.

Stage 2 — Appointment of lead reviewer and evidence gathering:

Appointment of a lead reviewer by the department, direction set for review, and agreed in the terms of reference. Evidence gathering and analysis begins, undertaken by the lead reviewer and review team. Departments should aim to appoint a lead reviewer within two months of a review starting.

Stage 3 — Full-scale review:

External research/inspection/interview is led by the lead reviewer and supported by the review team. Stage 3 should be concluded within four months of the appointment of a lead reviewer.

Stage 4 — Either a submission of the lead reviewer’s report to ministers

Detailed review report produced by the review team and the lead reviewer submitted to the PAO for review, followed by submission to the relevant minister for final approval.

OR a submission of self-assessment outcome showing no need for a full-scale review. After Stage 1 the team conducting the self-assessment determines that either the ALB and the department are in sufficiently good health or that any identified issues can be managed through proportionate actions short of a full-scale review. In this case the outcome of the self-assessment should be submitted to ministers alongside any further information in the case against review; this submission should include any recommendations coming from the self-assessment stage. Outcomes from a review concluding at self-assessment stage should be published, implemented, and reported against in the same manner as those emerging from a full-scale review (see paragraphs 192 to 194). Ministers may decide to ignore this conclusion following self-assessment and request a full-scale review.

Stage 5 — Publication:

Publication of the recommendations alongside a departmental response and a summary of the review by the department. Departments should aim to publish outcomes of reviews as soon as possible and no more than three months after the conclusion of a review.

Post-Review:

Implementation of recommendations by the department. The Cabinet Office will request updates on progress to provide assurance that departments are implementing recommendations.

131. Once a review is completed, the department should notify the Cabinet Office Public Bodies Team to support their oversight of the departments’ progress.

Annual prioritisation

132. Ahead of the start of this programme, departments were asked for their rolling three-year plan for reviews.[footnote 10] This process will be repeated at the end of every calendar year for the duration of the programme. These annual prioritisation letters and subsequent responses from the departmental minister, should be copied to the Chief Secretary to the Treasury.

133. Departments, as agreed with their ministers and Principal Accounting Officers (PAO), should use this letter to prioritise reviews of their public bodies. Departments should prioritise reviews based on the risk carried by their ALBs and the changes they have experienced since their last review. Prioritisation should also consider such factors as:

- Views of ministers and PAO: Departmental assessment of the risks and opportunities presented in their public body landscape, including ministerial and permanent secretary views.

- Financial: Significant changes to expenditure and number of full-time employees, findings from Spending Reviews, National Audit Office reports, and Public Accounts Committee reports.

- HM Treasury and Cabinet Office views: The relevant HM Treasury Spending Team should be consulted.

- Timing: The length of time since the ALB’s last review.

- Delivery: The centrality of the body to the delivery of wider government objectives.

- Changes in context: A change in external context and/or any events that have significantly affected the ALB’s delivery, performance, or operations (for example, COVID-19) or a ‘trigger event’, such as a leadership change.

- Users: Views of the body’s users, the public, and Parliament.

- Founding legislation: If appropriate, how the body is, or is not, complying with its original purpose enshrined in legislation.

- New bodies: It is a requirement to review a new body in line with the approval conditions set when it was established. This is usually within 18 to 24 months of the commencement of full operations.

- Functional views: Functional leads within the department should be asked for their view.

- Shareholding: If appropriate, views from UK Government Investments.

134. The team prioritising reviews should consult relevant departmental functional leads on the ALB’s risk profile.

135. Departments should write back promptly to the minister responsible for public body policy in the Cabinet Office and Chief Secretary to the Treasury with their plan outlining what reviews are scheduled to take place during the life of the programme, with the following degrees of commitment:

- Plans for the year ahead: Reviews that will take place; and

- Plans for subsequent years: Reviews planned to take place.

136. It is for the PAO, in partnership with relevant ministers in the department, to decide on the ALBs they prioritise for reviews each year. This prioritisation may be amended during the annual update to reflect changes in circumstances.

137. Departments are no longer required to review all of their ALBs over the course of a Parliament, although departments with a small number of ALBs are likely to meet this aim.

138. Additionally, the Cabinet Office and HM Treasury reserve the right to comment on the decisions made by departments on their prioritisation plans, and will consider the new bodies that have been formed by departments in the last 18 to 24 months.

139. The Minister for the Cabinet Office and/or the Chief Secretary to the Treasury may respond to the prioritisation and review plans outlined by departments as required.

140. At the end of each calendar year, the Minister for the Cabinet Office will write to departments reflecting on the reviews completed and request an updated plan for the remainder of the programme. It will also provide an opportunity for the Cabinet Office to consider whether any adjustments need to be made to the review programme.

141. The annual prioritisation letter should also be an opportunity for ministers and the PAOs in departments to update the Cabinet Office on progress over the last year and outline how the department is implementing recommendations.

Self-assessment

142. The Self-Assessment Model (SAM) underpins the proportionate principle of the review programme. The SAM consists of a set of questions for departments and ALBs to use as a desk-based ‘health-check’ of the ALB and to review the relationship with the sponsoring department. The SAM contains guidance for the department to complete it in partnership with the ALB.

143. The SAM has been designed to be used for those bodies prioritised for review by the department. Departments should use the SAM as a factor when considering whether a prioritised body merits a full-scale review.

144. What the results of the SAM say about the ALB and the sponsorship of the ALB will be for the department to interpret.

145. It is expected that the SAM should be completed with the support of both the sponsor team and the ALB. The ALB and the department may decide to each complete the SAM, as this may support the self-assessment to help the ALB and department identify differences in conclusion and work to resolve them. Responses must be consolidated when returning them to the Cabinet Office.

146. A review team may not be in place by this point, as some departments will only set one up for full-scale reviews. In this instance, departments will need to consider how to resource the completion of the SAM and take into account that they must be assured that the conclusions are factually accurate and objective. For example, the sponsorship team should not complete questions regarding their own capability.

147. During this process, the department will need to align its research with the Requirements for Reviews of Public Bodies. It is also important to consider if and where the results of the SAM identify ‘triggers’ for a full-scale review. Further information on conducting evidence gathering and stakeholder engagement can be found in paragraphs 163 to 167.

148. The SAM, in combination with departmental knowledge informed by the considerations listed in paragraph 133, will help to determine whether the department and ALB recommend a further full-scale review. Departments should also make use of existing sources of information, including the body’s annual report and accounts (ARAs), past reviews from the tailored review programme, and reports from the National Audit Office. The SAM is not intended to provide a final and authoritative view on the need for a full-scale review, but rather provides an indication of performance against a number of baseline performance indicators from the requirements. When deciding whether to proceed to full-scale review, departments should take a holistic view of the body’s performance, including consideration of factors that determine the prioritisation of reviews as set out in paragraph 133.

149. The analysis will also help the ALB and its sponsor department to identify the scope of the review. It is possible that the self-assessment is deemed a sufficient and adequate review of the ALB and no further work is required.

150. Once a SAM is completed, the department will determine and follow an appropriate internal clearance process to conclude this stage — both the PAO and responsible ministers in the sponsor department must be engaged. The conclusion should outline either:

- the need for a full-scale review and its scope; or

- an explanation as to why a full review is not required.

151. Where the department is satisfied that a full-scale review is not required following a self-assessment, recommendations can still be produced to improve any identified concerns. Such recommendations should be agreed, implemented, published, and reported on in the same manner as a full-scale review.

152. If a department determines a high-priority review ought to stop at the SAM stage and not proceed to a full-scale review, the department should engage the Public Bodies Team to discuss their rationale and the outcomes from the self-assessment stage.

153. If it is determined that a full-scale review is required, this should be agreed in partnership with the ALB and relevant teams within the departments. It is recommended that both ministers and the PAO are involved in the decision to move to a full-scale review.

154. Please refer back to paragraphs 129 to 131 to see the role of the SAM in the context of the review steps. Conclusions from the SAM should be submitted to the Cabinet Office via publicbodiesreform@cabinetoffice.gov.uk.

Commencing a full-scale review

155. The self-assessment will be one way of identifying the need and scope for a full-scale review of an organisation. However, paragraph 133 also highlights other factors that a minister, PAO, and department will need to consider when making this decision. Departments should consult functional experts and HM Treasury spending teams on the decision whether to proceed to full-scale review. Where a newly established body has been included in a department’s plans, it is expected that this should proceed to full-scale review within 18 to 24 months of establishment.

156. Once the decision is made to move to a full-scale review, the department will ensure that there is a review team in place and will appoint a lead reviewer to undertake the review (see paragraph 100 to 108).

157. To commence a review, the PAO, relevant minister, or senior sponsor in the department should consider writing to the lead reviewer with an explanation of the need for the review and a justification for its scope. This letter should reference the findings of the self-assessment, and any additional factors outlined in paragraph 133.

158. The PAO, department, and ministers should ensure that the ALB being reviewed is engaged in the commencement of a full-scale review. The senior sponsor should be proactive in ensuring there is dialogue between the department and ALB. It is recommended that the ALB chair is consulted regarding the review and its aims.

159. The review team should draft terms of reference in consultation with the ALB; the sponsor department, including ministers; and the lead reviewer. In the interests of expediting the start of a review, review teams should begin work on terms of reference before the appointment of the lead reviewer. However it is essential that the lead reviewer is content with the terms of reference before the review is launched, and so these should not be finalised until the lead reviewer is appointed.

160. The review team must invite the responsible minister an opportunity to sign off on a review’s terms of reference. Review teams may also wish to share terms of reference with the Minister for the Cabinet Office for comment.

161. Template 4 must be used when drafting the terms of reference. Departments should discuss amendments to this template with the Public Bodies Team at the Cabinet Office.

162. Departments are strongly encouraged to consult with their relevant HM Treasury spending team and the Public Bodies Team when considering the terms of reference. For high-priority reviews, departments must share terms of reference with the Public Bodies Team for consultation. The Cabinet Office does not need to formally approve the terms of reference in any review.

Evidence gathering and stakeholder engagement

163. Evidence to support the review should be gathered both at the self-assessment stage and a full-scale review, if one takes place. As the department will determine the depth and scope of any review, it will be for the department to clearly outline in the terms of reference (see Template 4) who they will be collecting evidence from and why.

164. Departments must ensure that the ALB has a clear role in the gathering of evidence. The ALB should support the department in undertaking the review by proactively engaging throughout the process and providing all required evidence in a timely manner. If this does not take place, the senior sponsor or PAO should meet with both the ALB and lead reviewer to discuss.

165. In addition and where relevant and appropriate, key stakeholders should have the opportunity to provide input into the review. Departments and lead reviewers are strongly encouraged to consider whether users or customers are considered in this. Review teams may consider approaching key stakeholders directly. This should be noted in the terms of reference and can also be reflected in the review report and recommendations.

166. If the organisation directly provides services to the public, the sponsor department and lead reviewer should consider launching a call for evidence or, if appropriate, a consultation. If launching a consultation, this should be carried out with regard to the Cabinet Office’s consultation principles.

167. Similarly, if the ALB partners with specific entities (for example, sector-based groups, suppliers, delivery partners), due consideration should be given to how evidence should be gathered and analysed from these. Review teams should consider informally or formally consulting with the ALBs’ auditors as part of the review to understand any existing financial or governance concerns with the ALB.

Challenge panels

168. A department may wish to consider the establishment of a challenge panel. A minister may request a challenge panel be established. The panel should have a chair who is independent of the review. Other members of the panel may be nominated by the lead reviewer, the department’s ministers, and the PAO. The panel could include external representation, for example, when a department wants to bring in sectoral expertise. The responsible minister should be informed when a challenge panel is created and of its panel membership. A department must seek ministerial approval to nominate a challenge panel member from outside the Civil Service.

169. The chair is responsible for ensuring their panel has sufficient expertise that it can fully engage with the areas under review, including the efficiency target.

170. The panel’s role would be to hear from the lead reviewer, understand the evidence base, and challenge emerging thoughts and recommendations in a rigorous and constructive manner.

171. The sponsor department’s ministers and PAO may wish to include representation of ministers from the sponsor department and, for example, ministers from other departments.

172. Challenge panels with ministerial representation perform the same role as those without.

173. Both of these panels can provide additional scrutiny and potentially lead to better informed recommendations, however both will add cost, time, and complexity to the review. Ministers and the PAO will want to carefully consider this trade-off before pursuing either option.

Engagement on high-priority reviews

174. Review teams should engage regularly with the Public Bodies Team. For high-priority reviews, review teams must engage with the Public Bodies Team and HM Treasury at a number of key milestones during the review, as set out below. This engagement is designed to serve as an opportunity for the centre to be consulted on the progress and direction of travel of reviews. Departments remain responsible for the delivery of their programmes of reviews with lead reviewers retaining accountability for their individual reviews.

175. For the purposes of this guidance, high-priority reviews are those concerning bodies with a total net expenditure of over £150 million p.a. or those of interest for wider reasons, for example, the delivery of a function central to a department’s objectives. The list of high-priority reviews will be set out by the Cabinet Office’s Public Bodies Team.

176. Where a department proposes to end a high-priority review after the self-assessment stage, the review team must consult the Public Bodies Team to discuss whether the SAM and its outcomes sufficiently address issues facing the body, including efficiency. The final decision on whether to take a body to full-scale review is for the relevant departmental ministers.

177. As set out at paragraph 162, review teams must share terms of reference for high-priority reviews with the Public Bodies Team for comment.

178. High-priority reviews must engage the Cabinet Office and HM Treasury in one of the following ways whilst in train:

- Challenge panel: Departments making use of challenge panels may invite Cabinet Office and HM Treasury officials to these. Review teams and the Public Bodies Team should discuss the most appropriate representatives on these panels. Full guidance on the use of challenge panels is set out at paragraphs 168 to 173.

- Mid-review update: At the mid-review point a review has largely completed its information gathering and draft recommendations for the review have begun to emerge. However recommendations should not yet have been finalised. The format of this engagement will be a short written briefing to Cabinet Office and HM Treasury, setting out findings and draft recommendations against the areas for review as set out in the terms of reference. This may be followed by a discussion between the Cabinet Office, HM Treasury, and the review team as needed.

179. Draft reports for high-priority reviews must be shared with the Cabinet Office and HM Treasury for comment before they are finalised and presented to ministers. This does not constitute a sign off procedure, but rather an opportunity to engage on the outcome of the review and the way its recommendations reflect its ToRs, findings, and any other concerns around the body. Reports should be shared at a stage once their content and recommendations are no longer expected to undergo material changes.

Drawing conclusions and developing recommendations

180. Delivering specific, measurable, realistic, evidence-based, and time-bound recommendations from the findings of the review is key to instigating change. Previous reviews have occasionally resulted in long lists of unachievable recommendations. Furthermore, a lack of tracking of the implementation of recommendations has prevented benefits from being realised.

181. It is the lead reviewer’s role — with the review team — to develop and draft the review’s conclusions. As with the rest of the review, the lead reviewer should be supported — but not unduly influenced — by the department and empowered to deliver evidence-based findings and recommendations.

182. The lead reviewer should ensure that the ALB is informed of, and has the chance to comment on, the findings and recommendations of the review.

183. The lead reviewer may wish to draw attention to how the ALB contributes to a wider outcome delivery system — where multiple public bodies and departments need to work in partnership to deliver an outcome for the public — and how changes can positively influence that system. In particular, the lead reviewer may wish to draw attention to issues that could not be resolved within the scope of a review.

184. The lead reviewer’s findings should clearly lead on to their recommendations. Recommendations should be:

- Strategic: Recommendations should not be unnecessarily numerous and should focus on the fundamental issues affecting the ALB rather than minor logistical issues[footnote 11];

- Targeted: The recommended solution should be tangible and actionable;

- Measurable: It should be clear if and how the recommendation has been implemented; and

- Time-bound: A target date should be given for implementation.

185. Some changes may require legislation to be implemented, and in considering the feasibility of draft recommendations, review teams should give thought to this. Any recommendations with primary or secondary legislative implications must be discussed, and agreed, with the Parliamentary Business and Legislation Secretariat (PBL) and may require collective agreement. Review teams should familiarise themselves with the Guide to Making Legislation (PDF, 3.6MB) when considering recommendations requiring primary legislation. The aims and objectives of any such legislation should always be clearly articulated to allow any post-legislative scrutiny to make an effective assessment of how such legislation works in practice (set out in chapter 40 of the Guide to Making Legislation (PDF, 3.6MB)).

186. The actual format of the final review and any annexes are not prescribed here, as they will be determined by departmental ministers, based on the nature of the review undertaken.

Agreeing and implementing recommendations

187. The lead reviewer should provide their report and recommendations to the department (that is the minister, PAO, and senior sponsor), who will then consider the report and respond to it.

188. If the department rejects a recommendation or pledges to complete it in a different way or to a different timescale, it should set out why it has done so.

189. While the department has the final decision on whether to accept or reject a recommendation, it is critical that it engages the ALB in this process to ensure that both the department and the ALB are ‘one team’ in delivering the review’s recommendations.

190. The process of responding to recommendations should be as follows:

- The report and recommendations are provided to the department and shared with the ALB’s leadership.

- The department carefully considers the findings and recommendations, and discusses them with the ALB.

- Ministers will then consider the recommendations. The department should provide justifiable reasons for not accepting recommendations. The department should aim to adjust recommendations if this will help them to be implemented, for example, the target date for a recommendation may be revised. Where adjusting recommendations, departments should discuss the implications of this with the lead reviewer, noting that the lead reviewer cannot compel a department to accept a recommendation in whole or in part. Where a recommendation has been adjusted by a department this should be noted in the departmental response to the review.

- The recommendations and the department’s responses should be published, with guidance on publication set out at paragraphs 192 to 194. The publication should clearly set out whether the recommendation is accepted and if accepted when it will be implemented, and if it is rejected the rationale for why.

- The department should track its implementation of the recommendations, keeping the PAO and ministers informed.

191. As part of the annual communication between Cabinet Office ministers and the minister in the sponsor department, departments will be expected to provide updates on the implementation of recommendations.

Publishing the report and recommendations

192. Transparency is vital to improving the trust and confidence in public bodies, and regular reviews are one way of contributing to this goal. There is an expectation that the department will publish the following:

- the review’s recommendations (including departmental responses to these);

- terms of reference (or a summary of these); and

- a narrative summary of the review and its findings.

193. Reviews that conclude at the SAM stage are expected to publish recommendations and a narrative summary of the review as with a full-scale review. Publications at the end of a SAM-only review may be shorter than those resulting from a full-scale review. Departments should inform the Cabinet Office’s Public Bodies Team once a report has been published.

194. Where there are sensitivities around the publication of reports and recommendations, departments should discuss a proposed approach with the Cabinet Office’s Public Bodies Team.

-

The Approvals Process for the Creation of New Arm’s-Length Bodies: Guidance for Departments (PDF, 843KB) ↩

-

Classification Of Public Bodies: Guidance For Departments (PDF, 888KB) ↩

-

While it is acceptable for plans for years 2 and 3 to be subject to change, the plan for year 1 should be adhered to, so far as is practicable. ↩

-

If there are numerous minor issues that the lead reviewer identifies, these should be grouped into a broader recommendation with the specific elements to be addressed annexed. ↩