Incorporating performance fees within the charge cap

Updated 14 March 2023

Applies to England, Scotland and Wales

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/incorporating-performance-fees-within-the-charge-cap/incorporating-performance-fees-within-the-charge-cap

Introduction

This document contains, amongst other things, the government’s response to Chapter 3 ‘Diversification, performance fees and the default fund charge cap’ of the 2020 consultation ‘Improving outcomes for members of defined contribution schemes’ and a further consultation on proposed regulations informed by the responses. The draft regulations would help facilitate occupational defined contribution (DC) schemes used for automatic enrolment investing in illiquid investments like private equity and venture capital. The government’s intention is that regulations on performance fees would come into force in October 2021.

‘Improving outcomes for members of defined contribution schemes’ consultation

We received 60 responses to the consultation ‘Improving outcomes for members of defined contribution schemes’ which contained regulations on net returns, consolidation, costs and charges, default Statements of Investment Principles (SIPs), wholly-insured schemes and property-holding costs.

This consultation is the next step – it contains the government response to the performance fee section (Chapter 3) of the September 2020 consultation and consults on consequential draft regulations. The government aims to publish a response to this consultation alongside a response to the remainder of the September 2020 consultation, ‘Improving outcomes for members of defined contribution schemes’, including final draft regulations and final statutory guidance, in June 2021.

This consultation also seeks views at this stage on the current position on look-through in relation to charge cap compliance, as a potential barrier to investment in alternative asset classes, particularly venture capital and growth equity. The government’s June 2021 response will include a summary of responses we receive and next steps on this issue.

About this consultation

Who this consultation is aimed at

- pension scheme trustees and managers

- pension scheme members and beneficiaries

- pension scheme service providers, other industry bodies and professionals

- civil society organisations

- any other interested stakeholders

Purpose of the consultation

This consultation seeks views on proposed regulatory amendments and the extent to which these achieve their stated policy intent – to facilitate investment by DC schemes used for automatic enrolment in illiquid assets such as venture capital.

Scope of consultation

This consultation applies to occupational defined contribution pension schemes regulated by the Department for Work and Pensions (DWP).

As pensions policy is a reserved matter for Scotland and Wales, this consultation applies to Great Britain. We are working closely with Northern Ireland counterparts at the Department for Communities in Northern Ireland to make corresponding legislation in line with parity principle that applies to pensions.

Duration of the consultation

The consultation period begins on 19 March 2021 and runs until 16 April 2021.

How to respond to this consultation

Please send your consultation responses via email to:

Sam Haylen, Vicky Bird, Tessa Lubrun and Andrew Blair at the shared address:

pensions.investment@dwp.gov.uk

We would also like to acknowledge the contribution of Matthew Tapley and Christopher Lord to this consultation document.

Note: When responding please indicate whether you are responding as an individual or representing the views of an organisation.

It is most useful for the government if organisations issue their response as a Word document. If respondents wish also to provide a PDF, they can do so.

Government response

We will aim to publish the government response to the consultation on the GOV.UK website in June 2021 as part of our wider response to the ‘Improving outcomes for members of defined contribution schemes’ consultation. As this response is linked to a Statutory Instrument, responses will be published at the same time as the Instrument is laid.

How we consult

Consultation principles

This consultation is being conducted in line with the revised Cabinet Office consultation principles published in 2018. These principles give clear guidance to government departments on conducting consultations.

Feedback on the consultation process

We value your feedback on how well we consult. If you have any comments about the consultation process (as opposed to comments about the issues which are the subject of the consultation), please email them to the DWP Consultation Coordinator. These could include if you feel that the consultation does not adhere to the values expressed in the consultation principles or that the process could be improved.

DWP Consultation Coordinator

caxtonhouse.legislation@dwp.gov.uk

Freedom of information

The information you send us may need to be passed to colleagues within the Department for Work and Pensions, published in a summary of responses received and referred to in the published consultation report.

All information contained in your response, including personal information, may be subject to publication or disclosure if requested under the Freedom of Information Act 2000. By providing personal information for the purposes of the public consultation exercise, it is understood that you consent to its disclosure and publication. If this is not the case, you should limit any personal information provided, or remove it completely. If you want the information in your response to the consultation to be kept confidential, you should explain why as part of your response, although we cannot guarantee to do this.

To find out more about the general principles of Freedom of Information and how it is applied within DWP, please contact the Central Freedom of Information Team:

Email: freedom-of-information-request@dwp.gov.uk

The Central Freedom of Information team cannot advise on specific consultation exercises, only on Freedom of Information issues. Read more information about the Freedom of Information Act.

Ministerial Foreword

Never has there been a better or more important time for a Defined Contribution (DC) pension scheme to consider innovating their investment strategy. Investment in emerging sectors like green infrastructure or innovative British companies fits well with the long-term horizons of DC schemes, and are vital to helping sustain employment, our communities and the environment. As the Chancellor announced at Budget 2021, we are now introducing flexibility and innovation for DC schemes to invest in such assets.

I commend schemes that are already making progress in this area but we fall behind our global partners in our commitment to these asset classes domestically and the economy as a whole suffers for it.

That is why I am bringing forward draft regulations, building on the policy proposed previously by the government, which would allow schemes to smooth the incurrence of performance fees, which are often payable on illiquid investments, over 5 years. The hope is that this will give trustees, especially those who might be unsure about investing in illiquid assets, greater confidence to make that leap, safe in the knowledge that they can deliver the best possible return for their members.

The measures, which we plan to introduce from October 2021, demonstrate the government’s commitment to removing perceived barriers to the commercial viability of innovative fund vehicles. In that spirit, this consultation also calls for views on the treatment of ’look-through’ costs. It has been raised with the government that the current position on look-through in relation to closed-ended investment structures reduces the attractiveness of such products amongst DC pension scheme trustees. I want to understand whether this a consensus view of the industry and the changes the government could consider to release investment in such products whilst maintaining the integrity of the charge cap.

With the momentum of the newly-created Productive Finance Working Group, of which the Department for Work and Pensions is a member, chaired by HM Treasury, the Financial Conduct Authority and the Bank of England, and its remit to stimulate demand and enable supply of illiquid investments, this consultation offers further easement that builds on the existing work the Department has done in this area. This includes taking forward, as part of our consultation ‘Improving outcomes for members of defined contribution scheme’, other regulatory changes in the DC market, including refocusing discussion on overall value, driving forward consolidation, and exempting costs of holding physical assets from the charge cap. I thank those who offered views on these regulations as part of the September 2020 consultation. I will respond to this consultation in June this year when confirming the relevant regulations.

I look forward to hearing your views on the regulations proposed in this consultation on performance fees, and feedback on the issue of look-through, as well as your overall commitment to meeting the challenges and opportunities we face head on.

Guy Opperman MP

Minister for Pensions and Financial Inclusion

Chapter 1: Summary

1. This document is the government’s response to Chapter 3 of the consultation ‘Improving outcomes for members of defined contribution schemes’. It also consults on additional changes to regulations designed to facilitate the diversification of DC investment portfolios.

2. It addresses stakeholder responses to the consultation proposal on performance fees within the charge cap. It consults on a legislative change to the way compliance with the charge cap is measured to give trustees flexibility to smooth such charges over a longer period in order to help facilitate investment in a diverse range of assets including illiquids. It invites views on these draft regulations.

3. Government aims to respond to this consultation, as well as all the remaining chapters of the ‘Improving outcomes for members of defined contribution schemes’ consultation, at the same time as final statutory guidance and regulations are published in June 2021. Government’s intention is that regulations will come into force in October 2021.

Developments since September 2020

Productive Finance Working Group

4. The Productive Finance Working Group[footnote 1] (PFWG) includes the Department for Work and Pensions and the Pensions Regulator, asset managers, industry groups, pension schemes and is co-chaired by HM Treasury, the Bank of England, the Financial Conduct Authority. Its mandate is to build upon work already undertaken to investigate the challenges and potential barriers to investment in productive finance assets in the UK, including the HMT’s Patient Capital Review[footnote 2] and the Asset Management Taskforce’s UK Funds Regime Working Group’s Long-Term Asset Fund (LTAF) proposal[footnote 3] - and propose concrete solutions to them.

5. The group’s work partly focuses on the UK defined contribution (DC) pensions market which is growing quickly, as a result of Automatic Enrolment (AE), and is potentially suited to long-term, diversified investment. The main solution which the group is tasked to deliver is the LTAF itself. The member organisations of the group will work together to design the new fund structure aiming to suit the needs of investors, for example, DC schemes and facilitate allocation to long-term assets. The aim is to have an LTAF set up by the end of 2021.

6. More widely, the PFWG seeks to propose other solutions to the perceived barriers to investment in productive finance that it uncovers. This consultation is however not within the remit of the PFWG nor does it address any wider barriers or potential solutions to them.

Charge cap review and charges survey

7. In January 2021, the government published its ‘Review of the Default Fund Charge Cap and Standardised Cost Disclosure’[footnote 4]. This review reaffirmed the government’s commitment to the Charge Cap as an important consumer protection which will remain at 0.75%. The Charge Cap applies to the default arrangements in schemes offering money purchase benefits for the purposes of automatic enrolment (broadly, DC schemes and hybrid schemes that provide both DC and Defined Benefit benefits).

8. The Pensions Charges Survey 2020[footnote 5], published alongside the 2021 Review, confirmed that the Charge Cap helped to drive down costs for members and ensured that they continued to receive value for money on their investments.

9. The Pension Charges Survey also revealed that actual charges are well below the level of the cap. The average large master-trust charges 0.4% on average, which provides evidence of significant headroom to the Charge Cap.

10. The Pension Charges Survey also included a section (3.5) on illiquid investments. This provided useful context as to the current level of take-up or allocation to illiquid assets. Two-thirds of providers had no direct investment in illiquids within their default arrangements. The other third had a small proportion, typically between 1.5% to 7%. The majority of these assets were property-related.

11. One of the major barriers to investment in these asset classes was perceived to be cost of the underlying investments. One provider explained that:

illiquid assets are typically a lot more expensive and what we are trying to offer, and what we have demand from our market for, is a very cost-efficient, low cost solution.

12. Other perceived barriers listed included inappropriateness for a DC default fund where members automatically enrolled may not be as alive to investment strategies, inherent riskiness which can come with some illiquid investments, requirements for daily liquidity, lack of daily pricing and the unpredictability of charges.

Chapter 2: Performance fee smoothing

Background

13. In the ‘Improving outcomes for members of defined contribution schemes’ consultation, the government consulted on changes to the treatment of performance fees in relation to the charge cap. This was based on feedback from stakeholders following the publication of the British Business Bank report[footnote 6] which suggested a change to make it easier to invest in asset classes that require the performance fees should be explored.

Performance fees

14. Traditionally, pension schemes have tended to dedicate the majority of their investment portfolio to public markets. These tend to be assets such as listed equities and bonds which are traded on a daily exchange. Such investments offer attractive advantages for DC schemes in that these tend to come at a low cost and can offer a good return. In doing so they enable DC schemes to more easily meet their fiduciary duties to scheme members.

15. However, as DC schemes mature and with more than 10 million savers now benefitting from being auto-enrolled into a DC scheme, some trustees of such schemes are looking to access a more diverse portfolio of assets including illiquid assets that have the potential of even greater return.

16. Whilst scheme trustees can and are already making such allocations without paying performance fees, for example in infrastructure or private credit, accessing the most illiquid, highest risk but highest potential gross return investments, like venture capital and private equity can often involve paying performance fees to investment managers. Whilst these structures can vary, the most common is the combination of a fixed annual management fee, paid regardless of return, and a performance-related element which is payable upon returns exceeding a certain “hurdle rate”.

17. The reason cited by investment managers for these higher fees is that such investments can often involve specialist active management which might include extensive research, niche expertise and greater ongoing engagement with business managers. Moreover, performance fees can act as an incentive to the investment manager to achieve higher returns for their client, as this will trigger a more profitable pay-out for themselves.

18. The most common type of performance fee is ‘carried interest’. This type of fee is charged to the investor, i.e. crystallised, at the end of the life of a fund but accrued at intervals across the investment period. This is a positive feature of such an arrangement which fund managers tell us encourages long term, responsible investment practices and discourages excessive risk taking to increase fees in the short term.

Calculating performance fee charges

19. Some stakeholders also fed back that paying fees such as carried interest was complex. As part of the Charges and Governance Regulations 2015, occupational DC pension schemes used for automatic enrolment must calculate for the default arrangement only, their ‘charges regime’ i.e. the charges levied on the members’ pots in one of 2 ways.

20. The first of these options, stipulated by Regulation 7, is the ‘retrospective method’. Come the end of the charges year, a period that varies by scheme, trustees must look back on the year’s data and pick at least four intervals at which to measure the member’s pot. They must then average these figures. Multiplying this by the charge cap figure, 0.75%, when using a single charge structure, tells them the maximum level of charges that can be imposed on that member. This method has the advantage of not requiring schemes to know their charges regime in advance but has the downside of offering less certainty in-year.

21. Regulation 8 offers the ‘prospective method’. Before the charges year begins, trustees must assume no growth in the value of the member’s pot and work out whether the planned charges to the single charge regime is compliant with the cap in this, the worst case example. They do this by selecting at least four intervals, as with the ‘retrospective method’. At each of these points the effect of the charges regime on the member’s pot is calculated. Dividing the total amount by which the pot has fallen by the original pot size will then tell trustees whether the charges regime is compliant i.e. no more than 0.75%.

22. Trustees have told us that the second option is preferred in most cases. It gives trustees assurances before the year begins about the lowest level to which the member’s pot can fall for the regime to be compliant. It can also be done for all members at the same time, reducing the burden.

23. In the ‘Improving outcomes for members of defined contribution schemes’ consultation, the government acknowledged that the nature of performance fees, i.e. end of fund crystallisation, unpredictability given fluctuating performance and accrual periods, meant that calculating the performances fees payable by members can prove difficult. As a result, the consultation sought views on a proposal to introduce a third calculation option just for performance fees.

Improving outcomes for member of DC schemes consultation proposals

24. The ‘Improving outcomes for member of defined contribution schemes’ consultation did not include any regulatory solutions to the performance fee issue. The government wanted to understand the degree to which the long-term nature of illiquid investments and the resulting long accrual periods for performance fees posed a problem when calculating charges. Some stakeholders had raised with us the prospect that the charge cap prevented trustees from exploring investments that incurred performance fees. The government sought wider views on this question.

25. If trustees felt that the difficulties in paying or calculating performance fees within the charge cap or the calculation methodologies available were material, the government proposed an option to make it less likely that a charge cap breach would be incurred.

26. Rather than the performance fees occurred in a single year forming part of that year’s charges regime, schemes could instead use a moving average in its place, spanning across multiple years. This would mean that for some years where schemes may happen to exceed the 0.75% charge cap because performance is good, they would not be penalised for doing so, so long as at the end of that multi-year period the average charge to members was within the charge cap limit. The proposal was originally proposed by the British Business Bank and Oliver Wyman in their 2019 report[footnote 7].

27. The motivation behind this proposal was to ensure that trustees had a greater incentive, or less of a disincentive, to invest in performance fee-inducing illiquid asset classes, without an immediate concern that in doing so they could not accommodate the ‘ebb and flow’ associated sometimes with the performance of these assets and still remain within the charge cap. We sought views on whether this motivation would be satisfied by this new performance fee calculation methodology or whether other barriers to illiquid investments, if they were to persist, more greatly affect asset allocation.

28. Stakeholder views on this proposal and the consultation questions are provided in the following section.

Stakeholder responses

Background

29. The following section summarises responses to Chapter 3 of the ‘Improving Outcomes for members of Defined Contribution schemes’ consultation which proposed a new method for charge cap compliance to give trustees more flexibility to pay performance fees.

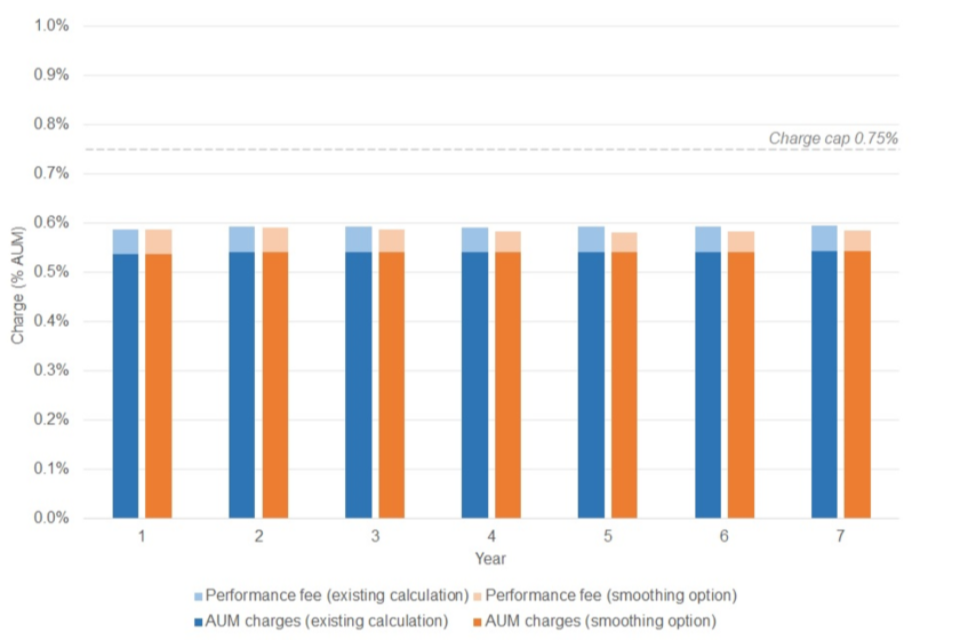

30. Here we summarise feedback and the proposed amendments to calculations within the charge cap to accommodate performance fees in order to facilitate investment in illiquid investments, as well as to put the exclusion of physical assets on a statutory footing.

Q4 – Performance fee prorating

Question 4: Do the draft regulations achieve the policy intent of providing an easement from the prorating requirement for performance fees which are calculated each time the value of the asset is calculated?

31. Of those who responded to this question, more than three-quarters supported our proposal, as set out in the draft regulations, to provide an easement to the requirement to prorate performance fees when trustees come to assessing compliance with the charge cap. This will in effect see trustees able to remove the performance fee from the charge cap calculation when they need to prorate for those members that have either joined or left the scheme during the charges year. Under the proposal, those members will only pay for the performance on the investment that they themselves have directly benefitted from during the year.

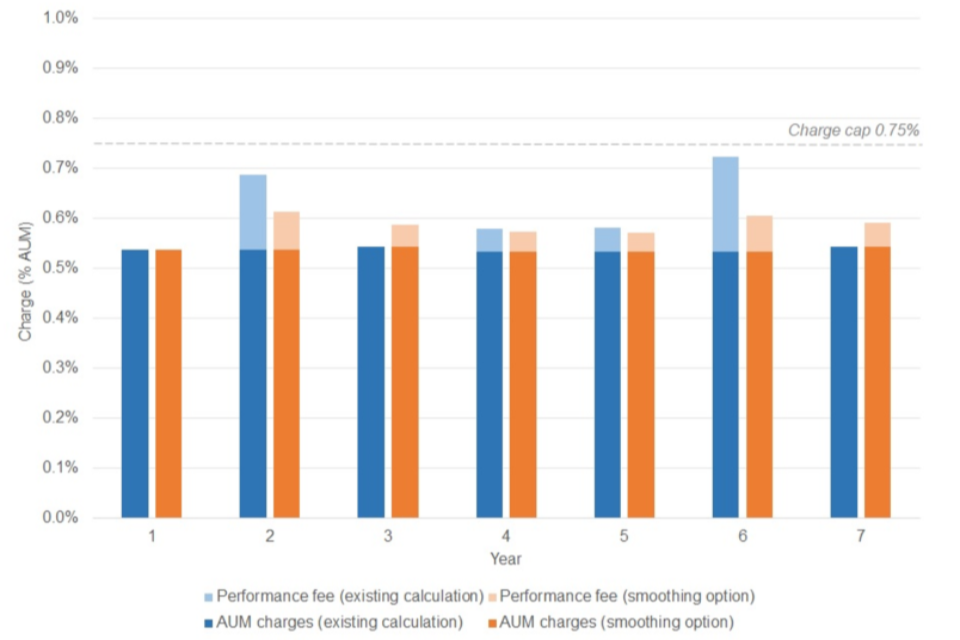

32. Respondents in support of this change commented that this would help trustees mitigate the challenge they can now face of dealing with performance fees when members join or leave the scheme during the year, specifically within an open-ended fund structure.

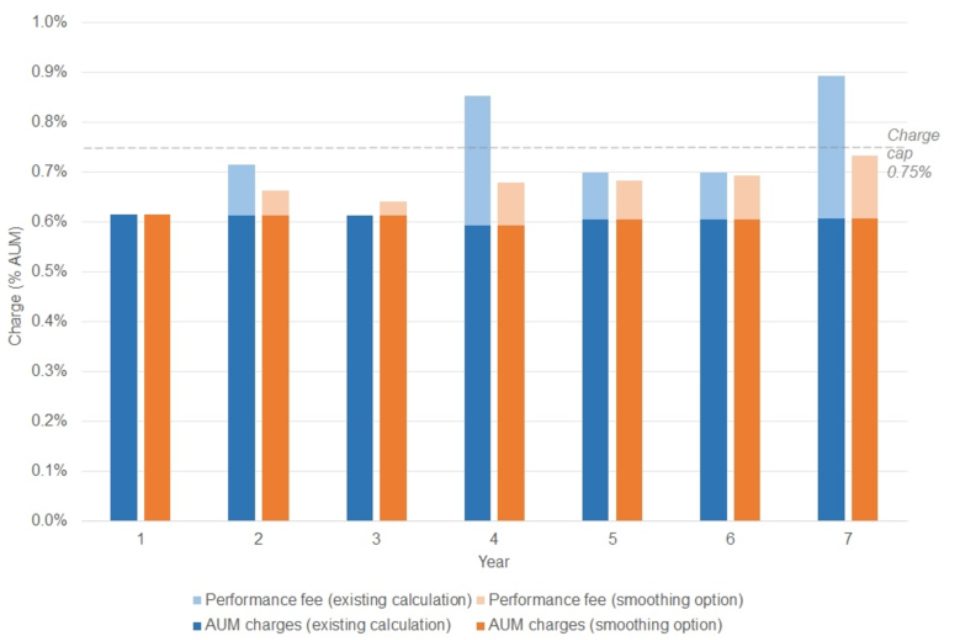

We see this as a positive step to accommodating performance fees. Essentially by only assessing full-year investors, private market funds that have a performance fee element (combined with a calendar year fund level total expense ratio cap) provides certainty that the overall charge cap won’t be exceeded on a blended basis within a default allocation.

Partners Group

We have long called for clarity and we think this proposal provides both the standardisation and clarity that is needed in one key and important area

PLSA

33. Those in support of this measure also explained that the challenge trustees currently face with performance fees is trying to ensure that the appropriate performance fee is applied to each individual member. This is because performance fees are primarily assessed by historical performance before they can be applied, and by that time, some members may have left the scheme and others may have joined. That time delay could sometimes lead to members paying higher fees for performance they did not benefit from, for instance if they joined a scheme at a period of good performance but performance did not remain consistent for the rest of the charges year.

The proposed change in regulation does help with regards to charge cap calculations: excluding performance fees from prorated calculations for members whose membership does not extend to the full year avoids scenarios where a small performance fee (in absolute terms) is artificially inflated.

Smart Pension

The proposals largely mitigate the specific challenge of dealing with performance fees when members join or leave the scheme during the year.

John Forbes Consulting LLP

34. While there was broad support for the proposal, several respondents were quick to emphasise that in their opinion even with the easement to performance fees in the charge cap, some assets such as private equity or real estate assets will remain difficult to value more frequently than annually.

35. A few respondents were of the view that the prorated approach added complication to the default charge cap, in particular when it comes to explaining this to members.

We question whether the easement goes against the intent of the charge cap. The charge cap is simple to calculate and explain, particularly to members. The easement introduces complexity which potentially undermines the protection afforded to members.

NOW: Pensions

Q5 – Design of multi-year smoothing option

Question 5: What should we consider to ensure a multi-year approach to calculating performance fees works in practice?

36. We were pleased there was broad agreement from respondents towards the multi-year approach presented, with many stating that this was a step change for the better for DC schemes looking to invest more in illiquid venture capital type investments, which it was confirmed, still predominately include performance-related fees.

37. Whilst supportive, there were a number of suggestions that came forward as to how the approach may be improved upon in practice. For example, one suggestion was to allow for averaging at the overall fund level rather than at an individual isolated investment in a broadly diversified portfolio.

The operational complexities may be too great to adopt a granular investment-by-investment approach.

Partners Group

38. We were also informed that to make a multi-year approach functional will require the inclusion of clear guidance about the permitted calculation methodologies, with one respondent setting out a possible approach to do this as follows:

One way to achieve this might be using existing, agreed calculation methodologies and bases for these methodologies that asset managers are comfortable and confident providing consistently across their client base.

Pensions and Lifetime Savings Association (PLSA)

39. One respondent suggested that when it comes to assessing performance fees using a multi-year approach, managers of funds are likely to take this into consideration alongside the progressive decline in management fees at the end of a fund’s investment period.

40. It was also explained to us that the smoothing approach would place increased dependency on investment managers to provide regular pricing information on assets to returns and on the level of performance fees being applied within the fund so trustees can ensure the cap is respected. Given the increased emphasis a few respondents believed further analysis of the investment managers performance as to whether they will be able to make the multi-year model work, or independent auditing of how they have applied this may be warranted.

Analysis should be undertaken as to whether a multi-year approach would mean that the investment managers are able to provide their strongest offering, or whether any proposed structure would mean that DC members would be receiving a diluted, lower standard, product.

Mercer Pension

41. A few respondents shared concern that to lengthen the charges cap calculation may complicate and compromise the effectiveness of the charge cap, which is generally understood now by trustees and members.

While we understand the rationale for a multi-year option, we have concerns that the lengthening of the charges calculation beyond the current annual review process could cause impact on the high quality and transparent annual fee assessment.

Lane, Clark & Peacock

42. A few respondents were of the view that in practice there would only be a small number of schemes that would actually make use of the approach. These were said to be those very largest schemes that through their fund size are more capable of absorbing higher fees.

In terms of the level of charges, this is heavily influenced by scale. With relatively small proportions of assets allocated to illiquid investments, it is mainly larger schemes that have sufficient scale to access illiquids.

Hymans Robertson

Q6 – Smoothing period

Question 6: We are proposing a 5-year rolling period. Is this appropriate or would another duration be more helpful?

43. There was broad agreement to a 5-year smoothing period with many respondents stating that 5 years was an appropriate timeframe as it coincides with the usual period over which many fund managers measure the performance of their assets, and also the minimum period to measure performance of private markets.

A 5-year rolling period would appear appropriate as this is often the period over which many funds measure their performance.

Buck

Five years is typically the minimum time period we would deem appropriate to measure performance of private markets (illiquid) assets. Given the typical holding period of such assets is 4-5 years, this would broadly be in line.

Partners Group

44. We were informed that shorter periods can present more challenges especially around practical reporting to members, and in respect of compliance with the charge cap.

45. Furthermore, it was also explained that performance fees, more commonly associated with less liquid investments, for example private equity, are types of investment that tend to lend themselves better to a relatively longer period of assessment because they traditionally have lower trading volume, may be prone to periods of some fluctuation in performance, but generally will likely mature in value over time.

A performance period which is rolling and provides a long enough time period to smooth out the ad-hoc nature of performance inherent in private equity, and thus the ad-hoc nature of performance charges, is beneficial for all parties.

Mercer

46. Whilst a rolling 5-year option was favoured, there was some support from respondents to a rolling ten-year period, or longer still to reflect that many investments often are a long term strategy with the impact of performance related fees likely to be considered over a longer timeframe too.

Ten years would be better than 5 years for reflecting the performance of a portfolio of property developments projects with varying holding periods.

Association of Real Estate Funds

Q7 – Alternative options

Question 7: We are proposing offering a multi-year option as an alternative to an in-year option for schemes. Do you have any suggestions for how to improve this offer?

47. Overall responses to this question supported the right of trustees to choose which of the 2 options they preferred to adopt.

We believe that offering both a multi-year option and an in-year option is a pragmatic solution, and would not suggest any additional changes to this offer. We propose that this be reviewed if and when this is implemented, to ensure that it is meeting the needs of all participants.

Mercer Pensions

48. A few responses we received that disagreed with the idea of offering up a choice explained that this was because they thought this may leave trustees open to criticism from members that the decision taken it may be argued disadvantaged them from receiving a better return on their investments.

As these 2 options will lead to different outcomes for members, trustees may be uncomfortable making a decision that may cause member complaints several years down the line. This may prevent trustees allocating to illiquids at all. In this case, removing choice may actually be beneficial to getting illiquids incorporated into DC investment strategies.

Aon

49. It was also explained to us that carried interest payments cannot always be accurately predicted and may end up greater than the amount of headroom available across the portfolio of investments. In those instances, fund managers were more likely to remain cautious and only seek to invest in investments that they can accurately predict will ensure they remain within the charge cap.

50. Several respondents commented that rather than strict compliance with ensuring performance fees did not exceed the charge cap, trustees of DC schemes needed more freedom around accommodating fees, which may lead on occasion to going above the charge cap. In particular, where the investment had performed well and justified the higher level of performance fee.

Given that strong performance and realised returns seem to be prerequisite to any breach of the charge cap resulting from carried interest payments, we suggest that DWP should consider giving DC schemes trustees appropriate protection against any liability by enabling them to explain any inadvertent breaches caused by performance fees or carried interest (accrued or paid).

Association of Real Estate Funds

51. In effect, rather than a smoothing of the performance fees, there were instead calls on government to work with the Pensions Regulator to offer comfort to trustees that investing in illiquid funds would not have negative consequences for them.

Q8 – Effect on allocation to illiquids

Question 8: To what extent will providing a multi-year smoothing option give DC trustees more confidence to invest in less liquid assets such as venture capital?

52. We were pleased there was broad agreement from respondents towards the option of a multi-year approach presented. Some respondents stated that this was a step change for the better for DC schemes looking to invest more in illiquid venture capital type investments, which it was confirmed, still predominately include performance-related fees.

It is true that performance fees on some asset classes (e.g. venture capital) are best assessed on a multi-year timescale.

Smart Pension

Multi-year smoothing will give DC trustees more confidence to invest in less liquid assets as concerns around shorter period increases in charges (and impact on net returns) will be allayed.

Buck

We view the main proposal of allowing the performance related element of an investment charge to be helpful in giving trustees greater confidence to use a broader range of investments. We see the approach of using a multi-year smoothing option as broadening the range and opportunities still further.

Lane Clark & Peacock

53. Several reported that a longer timeframe and agreed method for calculation would provide comfort to DC trustees that the performance fees being charged to members are smoother and more closely resemble fees charged in more traditional private markets investment vehicles. One respondent in particular summarised that where investments have delivered a higher than expected return for scheme members this should be encouraged and the multi-year approach partially mitigates this, as a longer period, and spreading generally, reduces the level of reliance on ongoing accruals of contractual fees that are based on estimates.

54. Another comment referred to this change as a positive step to reassure trustees that the likelihood of possible upward and downward trajectories in performance fees would not prohibit illiquid investment as it would allow them to ensure their charges regime remains within the cap.

When considering their illiquid fund investments, trustees could factor that into their consideration of likely spikes in management fees. Whilst not perfect, this could give some comfort to DC trustees and allow them to avoid an overly conservative approach on the charge cap and performance fees.

Pinsent Masons

A multi-year rolling calculation should give trustees more confidence that the smoothed approach will mean the possibility that the charge cap is breached over shorter periods is lessened, provided there is no requirement to include performance fees in the charge cap test for any combination of entry and exit dates within the multi-year period.

Barnett Waddingham

55. A few responses suggested that despite the efforts to provide flexibility within the charge cap, they saw little change from the status quo with trustees only looking to invest in illiquid assets if these do not have a performance fee attached.

If changes to performance fee calculation methodologies are the extent of the policy reforms, then the investment management industry would still need to drastically reduce their fees (and therefore their revenues) which most likely cannot be offset by cost-savings and economies of scale in the short to medium term.

Nest

The barriers to investing in less liquid assets for DC scheme trustees have, to date, not been the implementation or monitoring of performance fee structures. Rather, the lack of confidence stems from practicalities around managing the illiquidity and the extent of work required with the administrator, platform provider (if relevant) and other parties to implement a fund.

ACA

56. Similarly, a few respondents were of the view that the introduction of a smoothing mechanism for performance fees adds complexity surrounding illiquid investments when instead more emphasis is needed on communicating the role of performances fees to members; how and when those fees are applied in practice, how a range of hurdle rates of return are applied (where they have been adopted along with other variable charges or costs), and an overall explanation to members that performance fees could be higher or lower than average levels in any given period.

We believe that insufficient emphasis has been placed on communicating the role of performance fees (if indeed they have been adopted, and indeed other variable charges or costs) with members, prior to their investment and that these could be higher or lower than average levels in any given period.

Hymans Robertson

57. Several responses we received said the measures proposed in the consultation did not go far enough to effect a real change to pension schemes attitude to investing in venture capital. In effect, that further steps or a different approach is needed instead.

The consultation does not acknowledge that the barriers to investing in venture capital are higher than those for other illiquid asset classes, due to the higher costs. We would encourage the government to recognise this and adapt policies to ensure that savers are able to access and benefit from the full range of illiquid assets that each bring different benefits within a diversified investment strategy.

UK BioIndustry Association

Q9 – Physical assets costs

Question 9: Do the draft regulations achieve the policy intent? Do you have any comment on the definitions used?

58. The vast majority of respondents agreed with the policy intent to formalise the exclusion from the charge cap of costs of holding physical assets – including maintenance costs, business rates, insurance and management fees among others from the existing 2016 non-statutory guidance to a statutory basis.

The proposal gives legal clarity on what is included under the charge cap and what is not which is welcomed by our industry.

Association of British Insurers

We welcome the proposal to put the exclusion of the costs of holding physical assets from the charge cap on a statutory footing for the additional certainty this provides.

Investment Association

The regulations provide clarity on an issue that arose soon after the charge cap was first introduced. Having it on a statutory footing will further increase clarity across the industry and make it easier for trustees in their deliberations of allocating to such assets.

Smart Pension

59. Few responses called for further clarity in relation to why property investment funds (closed-end investment companies) are included in the charge cap, but cost of holding physical assets are not.

60. Several respondents asked for clarity regarding the requirement for “look through” for Real Estate Investment Trusts (REITs) and other investment trusts management costs, as far as these apply to fees that now form part of the charge cap in the proposed regulations.

The distinction between a closed-ended real estate fund and a real estate commercial company, in the sense of the net economics of the investment, is arbitrary; the magnitude and indeed the type of drag or leakage of underlying asset returns to the remuneration of senior management etc. is equivalent.

CFA UK

Statements regarding “look through” remain unclear and impractical in respect of certain investments. For example, we note that the Department’s suggested approach could produce seemingly arbitrary results when applied to 2 substantively similar REIT investments, one of which happens to be classified as a closed ended investment fund and the other as a commercial company.

Association of Pensions Lawyers

Government Response

Q4 – Exempting performance fees from prorating

Government Response

61. We are pleased with the level of support we received for our proposed measure to provide a prorated easement to performance fees. We did not receive any specific suggestions to re-word the regulations on prorating and so will move forward with a very similar version of these regulations.

62. On the whole, respondents agreed with the policy intent of this easement that seeks to prevent situations occurring whereby scheme members may be charged for a performance fee during a charges year which they themselves have not benefitted from because they had either joined the scheme after the performance of the asset was assessed, or left during the year and likewise would not have benefitted from subsequent performance assessment. It is crucial that this approach must be equitable across all the members, with each member only paying for the performance that they have benefitted from for the period they were exposed to the investment.

63. Feedback from this consultation reaffirmed the point made previously to us that fund managers often lack confidence to explore less liquid investments because of concern that the performance fees associated push them close to the charge cap requirement. We are therefore encouraged that stakeholders agreed the easement approach has the potential to release some headroom within the charge cap, with many confirming that this could provide an incentive for fund managers that want to utilise this potential space to access a wider range of investment opportunities.

64. We remain open to finding further ways in which we can facilitate opportunities for DC pension schemes to access private markets balanced with by the importance of the charge cap as a protection for scheme members.

65. Some stakeholders felt the prorated approach could add a layer of complexity when explaining to members the default charge cap. We do not underestimate that there will be some administrative complexity involved, especially when it comes to applying this to bigger schemes with potentially thousands of individual members invested, and also then how this is communicating to all members in the chair statement. The government wishes to avoid making chair statements unnecessarily lengthy or more difficult to comprehend. We remain confident that trustees will be able to manage this approach, and also ensure they remain transparent with their members on how costs and charges have been reached, and importantly what has been done is equitably to every member.

66. The definition of performance fees in the regulations should make it clear which charges are to be considered when prorating and which are not. Government believes that the reasons for this approach relating to the fair allocation of performance and therefore performance fees, will be reasons that members would understand. The benefit of easier prorating we believe outweighs the cost of some increased complexity in administration.

Q5-8 – Multi-year smoothing of performance fees

Government Response

67. We are equally pleased with the positive reaction we received to the idea introducing the option of a multi-year rolling/averaging period to accommodate performance fees for the purpose of the charge cap calculation.

68. Stakeholders agreed with the underlying policy intent to give trustees of DC schemes, a flexible mechanism by which they might account for performance fees attached to a wider range of investment opportunities over a slightly longer period of time, and yet still remain within the charge cap.

69. In response to points raised about the lack of flexibility in the default charge cap, government would like to draw trustees and advisers’ attention to the findings of the Pension Charges Survey 2020 which suggested there was significant headroom for most schemes.

70. Illiquid investments tend to achieve different performance levels at different stages with performance fees reflecting that, and so we believe the multi-year approach provides a flexible option for fund managers to reflect the natural ebb and flow of some investment performance yet still ensure they are not breaching the cap. In this document, we have set out some illustrations to demonstrate how we see that smoothing approach could work, showing that why the charge cap level may be breached for some years of the multi-year period, schemes will not be penalised or members disadvantaged in doing so as long as managers of schemes can ensure that they remain within the charge cap limit at the end of the period.

71. Government has noted some stakeholder’s preference for a longer rolling period of 10 or more years to reflect those illiquid investments that have a longer lifespan. However, at the present time government considers that ten or more years represents too long a period by which fund managers will be able to accurately predict the level of the performance fees. A longer period also risks exacerbating the issue of members accruing performance fees but leaving the fund before the end of the investment period when those fees are crystallised. Furthermore, government believes a longer rolling period could promote greater risk taking in early years and high levels of performance fee accrual initially in the hope of regaining losses in later years – a 5-year period strikes a better balance here.

72. With respect to concerns expressed that a 5-year approach may add administrative complexities, in particular around different cohorts of members and predicting fees over the first 4 years, the government acknowledges that this is likely to present a challenge initially, especially for larger schemes with considerably more members, but we believe this is something that schemes will embrace and make work for them in order to try to take advantage of the investments that can potentially yield greater returns for their members. It is for trustees of course to decide to what extent the benefit of their smoothing method, permitted with regulations laid out in this consultation, outweighs the increased complexity of calculation.

73. We agree with views that the multi-year approach places a greater emphasis on investment managers to provide regular information on returns and on the level of carried interest performance fees applied within the fund to ensure the charge cap is respected. Fundamentally, we see this as a positive for schemes and members.

74. We do not accept that difficulties in communicating how performance fees are applied to investments should be cited as a barrier to offering trustees the option to take advantage of a multi-year smoothing method. Trustees must ensure that they are communicating the charges regime effectively; there are established mechanisms for doing this, namely the chair’s statement and requirements the government has put in place to illustrate the compounding effect of charges on member’s pots.

75. It is important to state that the multi-year approach is not a requirement that schemes must adopt. Trustees are being provided with a choice over which method they would like to apply to the use of performance fees. The introduction of an alternative option was overwhelmingly supported in the responses we received to the consultation - it is right that trustees weigh up each approach before deciding which one best suits their investment strategy and offers best value to members.

76. Some respondents questioned the government’s intention to facilitate investment in illiquid assets, stating that many less liquid asset classes are not appropriate for the DC pensions market. Trustees have the fiduciary duty to act in the best financial interest of their members – this is their unfettered purpose. As part of this, the government encourages trustees to develop diversified portfolios that meet their members’ needs. The government does not seek to direct investment in any way - instead the role of government is to help facilitate innovative investment classes and the financial products available to schemes. Decisions around risk appetite, the trade-off with the potential for higher returns, and the sacrifice of liquidity are for trustees to make but we acknowledge that investment in illiquid assets can offer a greater return and benefit members.

Q9 – Treatment of physical asset costs

Government Response

77. Overall, the government was pleased with the support received for exemption of certain property holding costs. There were some suggested changes to the definitions used and the wording of the regulation which will be reflected in the final version of the regulations laid and published this summer.

78. A minority of stakeholders suggested that the government was creating an arbitrage opportunity in relation to REITs in relation to the way capital was raised. However, some argued, in requiring look-through in relation to all UK listed closed-ended investment funds and international equivalents, the treatment of underlying costs presentationally, i.e. whether part of the charge cap, varied simply as a result of an arbitrary difference in the way that a REIT decided to raised capital i.e. open-ended or closed-ended or whether it was listed or not.

79. The government agrees that the underlying cost to investors of investing in property either directly or indirectly does not vary based on whether look-through forms part of the charge cap or not. The government does not sense that there is a groundswell of support for removal of look-through requirements but that the concern amongst stakeholders is that this difference in treatment of costs has purely presentational impacts and that this difference may dissuade investment by DC schemes in such products. We encourage views on this later within the consultation section. Chapter 3, of this document.

80. At present, trustees should continue to look-through a REIT, indeed any open-ended or closed-ended fund, but not commercial companies. The government believes that such classifications are materially different and therefore different treatment of costs is justified. A company that has an underlying commercial purpose but holds property, for example, a supermarket chain, should not be subject to investor look-through. Funds, listed or otherwise, do not have an underlying commercial purpose and invest purely for investor return and so look-through should apply.

81. Stakeholders also suggested that the order in which look-through and the exemption of physical asset costs should occur was unclear. The government believes that trustees should carry out the exercise of looking-through all investment funds first. Then, trustees should consider whether any of these costs fall within the government’s definition of physical asset costs. The exemption of physical asset costs from the charge cap, which we are introducing in regulations, applies to all investment structures, whether direct or indirect, individual or pooled fund, closed or open-ended.

82. A reminder of these definitions below:

- physical assets are defined as: an asset whose value depends on its physical form, including land, buildings and other structures on land or sea, vehicles, ships, aircraft or rolling stock, and commodities

- within that, commodities are defined as: any goods of a fungible nature that are capable of being delivered, including metals and their ores and alloys, agricultural products and energy such as electricity, but not including cash or financial instruments

- the non-exhaustive list of costs is:

- the costs of managing and maintaining the asset

- fees for valuing the asset

- the cost of insuring the asset in question

- ground rent charges, rates and taxes incurred in relation to the asset

Proposed changes to regulations

Multi-year smoothing of performance fees

83. Given that the consensus emerging from the ‘Improving outcomes for members of defined contribution schemes’ consultation was that introducing the option of smoothing performance fee payments over multiple years would reduce the risk of a charge cap breach and could increase investment in illiquid assets, the government is bringing forward regulations. The remainder of this chapter focusses on a proposed change to regulations to permit trustees to take advantage of the option of a multi-year smoothing method for performance fees.

Amendments to the Charges and Governance Regulations

84. The policy intent is to supplement the 2 existing permitted methods for calculation of the scheme’s charges regime with an option to include a 5-year moving average for performance fees as an alternative to the in-year performance fees accrued.

85. At present, Regulations 7 and 8 of the Occupational Pensions Scheme (Charges and Governance) Regulations 2015 (“the Charges and Governance Regulations 2015”) offer 2 different methods for calculating the charges that can be imposed on members for the given charges year. Both methods require the level of charges for that year to be based on the costs and charges the scheme has paid in the given charges year.

86. The regulatory proposal the government is looking to bring forward will allow trustees and managers of relevant DC schemes to make an exception to this requirement only in respect of performance fees. Instead of being required to look back on, in the case of the retrospective method, or predict, in the case of the prospective method, the performance fees incurred over the course of the 12 months’ period, known as the charges year, trustees and managers can ‘swap out’ this figure for a 5-year moving average of accrued performance fees.

87. The section of the draft SI making amendments to the Charges and Governance Regulations 2015 is attached in Annex C with a Keeling Schedule demonstrating the changes in situ in Annex D. These amendments seek to insert new paragraphs into Regulations 7 and 8. For Regulation 7, the new paragraph 10 (inserted by regulation 1(2) of the draft regulations) is the integral provision. It states that when calculating the performance fee element of the charges regime, trustees may treat the fee as X/5 where X is the sum of performance fees incurred over at most the previous 5 years. The subsequent section, ‘How this would work for trustees’ goes into more detail as to how trustees might implement this method.

88. In order to do this, trustees will need to calculate 2 elements. The return earned by the relevant assets (those invested in performance fee-inducing investments), subparagraph (a) of inserted new regulation 7(11)[footnote 8], in order that subsection (b) of that regulation the amount of performance fee payable as a result of that return, can be calculated.

89. In order to make use of this option, the definition of ‘performance fees’ must be met as defined by regulation 6 or the draft regulations consulted on in September 2020:

performance fee” means a fee which— (a) is calculated by reference to the returns from investments held by the scheme, whether in terms of the capital appreciation of those investments, the income produced by those investments or otherwise; and (b) is not calculated by reference to the value of the member’s rights under the scheme.

90. The second condition for use, as inserted by new paragraph 9 of regulation 7[footnote 9], is that the performance fee relates to assets in the default arrangement, incurred during the investment period. In this regulation, “investment period” means the period for which the assets in the default arrangement are invested in an investment for which a performance fee is payable, otherwise known as the life of the investment fund.

91. The second section of the draft SI then makes equivalent provisions in Regulation 8 which offers the second of 2 general methods for calculating the overall charge cap.

Question 1: Are the performance fee regulations:

a) clear

b) likely to be taken up by trustees

c) going to make a difference to trustees’ confidence to invest in illiquids?

How this would work for schemes

92. To provide guidance on how a multiple year smoothing approach would work in practice, a series of illustrative examples have been developed. For a scheme that invests in a venture capital (VC) or illiquid investment product with associated performance fees, the examples demonstrate the possible impact averaging these fees - over a period of up to 5 years – may have on the risk of breaching the default fund charge cap (0.75%). The examples do not account for the effect of scheme members moving in or out of a fund during its lifetime nor do they account for changes in asset allocation a scheme may choose to make to its portfolio during the investment period.

93. The modelling of the illustrative examples builds upon British Business Bank/Oliver Wyman analysis conducted to support the recommendations their September 2019 paper made around multiple-year calculation of performance fees[footnote 10].

94. Three scenarios are presented, each of which involve the fictitious DC pension scheme, Grow Pension. Grow Pension are keen to diversify the asset allocation of their largest default fund and are considering investing in a private equity fund, Forte PEI. Forte PEI operate a “2-20” fee structure in which investors are charged a fixed annual management charge of 2% of assets under management (AUM) alongside a 20% performance fee on returns delivered above an 8% hurdle rate. Grow Pension have some concerns about using Forte PEI due to the higher costs quoted and the unpredictability of the performance related element of the fee structure. Grow’s main concern is the possibility that performance fees, which are accrued annually over the life of the private equity fund, could lead to the charges imposed on members exceeding the 0.75% charge cap in a given year when returns are high.

95. Figures 1 – 3 illustrate how Grow Pension’s charges regime may be calculated over a period of 7 years whilst their members are invested in Forte PEI as well as a mix of liquid assets with fixed management charges. The charts compare how Grow’s charges may be calculated, using the existing legislation around charge cap compliance, against how the charges may be calculated if Grow were to take advantage of an optional easement permitting the averaging of performance fees over a period of up to 5-years, hereon referred to as the “smoothing option”.

96. The examples focus on a scheme that uses the retrospective method of charge regime calculation, permitted under Regulation 7 of the Charges and Governance Regulations 2015. This means that the scheme looks back over the charges year, at the end of the charges year, and calculates the fees that can be imposed on members within the cap. The regulations also allow for a similar calculation using the prospective method, permitted under Regulation 8.

97. In each scenario, the total assets under management in Grow Pension’s default fund at the start of the 7-year period are £100 million. In each year, the fund grows by 6% solely due to additional member contributions. On top of this, average investment returns for Forte PEI are assumed to be 15% and 8.5% for the other assets in the fund.[footnote 11] The scenarios assume that all members of the Grow Pension default fund remain invested in Forte PEI for the whole of the fund’s life. The full set of assumptions for the 3 scenarios are set out in Annex E.

98. Forte PEI charges performance fees in the form of ‘carried interest’. Under both the existing regulations and the smoothing option provided for in draft regulation, performance fees are included in the assessment of charge cap compliance at the point of fee accrual. All performance fees presented in the below examples are annually accrued fees - notionally deducted from members’ pots at the end of each year. Crystallisation of performance fees, the payment of fees from the notional pot of member deductions to the fund manager, is assumed to take place at the end of a fund’s life. The total performance fee crystallised will be the sum of accrued fees over the fund’s life. Charge cap compliance is not a requirement at the point of crystallisation as this will already have been demonstrated at point of accrual.

99. The first example represents a hypothetical baseline scenario where Grow Pension’s asset allocation is 5% to Forte PEI and 95% to other assets which only use fixed management charges. Over 7 years of the fund’s life, the total assets under management increase from £100 million to £219 million as a result of investment returns and additional member contributions. Assets invested in Forte PEI increase from £5 million to £12 million. This is based on the 15% and 8.5% returns assumptions set out above.

100. The annual charges imposed on Grow Pension members across the DC default fund, under the baseline scenario, including management charges and the annually accrued Forte PEI performance fee, are presented in rows 3 to 6 of Table 1. In measuring these charges for the purposes of charge cap compliance at a member level, trustees of Grow Pension may use the existing process stipulated by Regulation 7:

- at the end of the charges year, look back on the year’s data and pick at least 4 intervals at which to measure the size of a member’s pot

- calculate the average of these figures

- multiply this by the charge cap figure (0.75%) to calculate the maximum charges regime which may be imposed

- calculate the sum of management fees imposed on the member and accrued performance fees over the charging year

- the charge cap is exceeded if the sum of member charges exceeds the maximum charges regime

101. Alternatively, Grow may choose to take advantage of the smoothing option. Rows 8 to 11 of Table 1 show the member charges measured across Grow Pension’s DC default fund if Grow trustees were to use the option to average the Forte PEI performance fee over a period of up to 5 years. To do this, Grow Pension trustees may use the following process:

- at the end of the charges year, look back on the year’s data and pick at least 4 intervals at which to measure the size of a member’s pot

- calculate the average of these figures

- multiply this by the charge cap figure (0.75%) to calculate the maximum charges regime which may be imposed

- calculate the sum of management fees imposed on the member over the charges year

- calculate the sum of the Forte PEI performance fees accrued over the charges year and each of the preceding charges years, up to a maximum of 4 preceding charges years

- divide this by 5, or where the investment period is less than 5 charges years, the number of charges years in the relevant period

- add the quotient (the smoothed performance fee) to the sum of management fees to calculate the annual total member charge

- the charge cap is exceeded if the annual total member charge exceeds the maximum charges regime

Table 1 – Annual charging regime (£millions) for Grow Pension’s Default Fund and charges measured for the purposes of charge cap compliance when the option to smooth performance fees is utilised

| Charges imposed on member | Investment year - 1 | Investment year - 2 | Investment year - 3 | Investment year - 4 | Investment year - 5 | Investment year - 6 | Investment year - 7 |

|---|---|---|---|---|---|---|---|

| Forte PEI performance fee – actual accrued | £0.05 | £0.06 | £0.06 | £0.07 | £0.08 | £0.09 | £0.10 |

| Forte PEI AUM fee | £0.10 | £0.11 | £0.13 | £0.14 | £0.16 | £0.18 | £0.21 |

| Other assets AUM fee | £0.44 | £0.47 | £0.54 | £0.61 | £0.69 | £0.77 | £0.86 |

| Total | £0.59 | £0.64 | £0.73 | £0.82 | £0.93 | £1.04 | £1.17 |

| Charges measured (multi-year smoothing) | |||||||

|---|---|---|---|---|---|---|---|

| Forte PEI performance fee - smoothed | £0.05 | £0.05 | £0.06 | £0.06 | £0.06 | £0.07 | £0.08 |

| Forte PEI AUM fee | £0.10 | £0.11 | £0.13 | £0.14 | £0.16 | £0.18 | £0.21 |

| Other assets AUM fee | £0.44 | £0.47 | £0.54 | £0.61 | £0.69 | £0.77 | £0.86 |

| Total | £0.59 | £0.64 | £0.72 | £0.81 | £0.91 | £1.03 | £1.15 |

102. For this same baseline scenario, Figure 1 presents the charges Grow Pension would measure if they were to use the existing compliance process compared to if they chose to use the smoothing option. To help demonstrate the level of charges measured relative to the charge cap, the charges are expressed here as a percentage of AUM. Figure 1 indicates that Grow Pension’s overall member charges would be substantially below the charge cap both under the existing charge compliance regulations and if Grow were to take advantage of the smoothing option.

Figure 1 – Annual charges measured by Grow Pension using the existing process compared to the smoothing option– Scenario 1 (base case, fixed returns)

103. Figure 2 shows the charges measured in a scenario where Grow Pension’s investment in Forte PEI experiences variance in returns over the 7 years. Forte PEI’s average returns for the period remains 15% but annual returns vary between 0% and 30%. All other variables remain constant. In this scenario, the impact of Grow choosing to take advantage of the smoothing option is more pronounced. Whilst the cap is not breached under either calculation approach, in years 2 and 6 where Forte PEI significantly outperforms, the increase in related performance fees lead total member charges to approach or exceed 0.7% under the existing calculation. Conversely, when the smoothing option is utilised, the charges regime remains between 0.5% and 0.6%.

Figure 2 – Annual charges measured by Grow Pension using the existing process compared to the smoothing option– Scenario 2 (variable returns)

104. Finally, Figure 3 illustrates the charges Grow Pension may expect to report in a scenario where they began the 7-year period with an increased proportion of their default fund’s assets allocated to Forte PEI: 10% with 90% allocated to other asset types. Under existing compliance regulations, in this scenario, Grow’s overall member charges would breach the charge cap substantially on 2 occasions due to Forte PEI’s significant outperformance in years 4 and 7. However, if Grow were to take advantage of the smoothing option the effect of averaging the fee would prevent cap breach in all years.

Figure 3 – Annual charges measured by Grow Pension using the existing process compared to the smoothing option– Scenario 3 (variable returns, increased allocation to Forte PEI)

Chapter 3: Look-through

Background

105. In both our consultations, ‘Investment innovation and future consolidation’ and ‘Improving outcomes for members of defined contribution schemes’ of February 2019 and September 2020, the government developed a position on look-through which now sits in statutory guidance on charge cap compliance. The government is now seeking views on its position, whether it acts as a significant barrier to investment in alternative asset classes, particularly venture capital and growth equity, and if so what solutions should be considered.

106. The current position is that trustees of occupational DC pension schemes should ‘look-through’ any fund of funds or pooled investment vehicles, no matter the type of funds such vehicles invest in. This means that trustees should not just incorporate the costs of investing in the pooled vehicle but look-through this structure and consider the costs paid by the pooled vehicle manager as it invests in other funds, known as the underlying investments.

107. Whilst this issue was not specifically consulted on, some stakeholders either raised it in context of other questions on performance fees or consideration of physical assets, or have raised it with the government since.

Call for evidence

108. In the consultation ‘Improving outcomes for members of defined contribution schemes’, the government made it clear that look-through should apply when investing in all open-ended funds, all UK listed closed-ended investment funds and international equivalents. Since the consultation, other stakeholders have suggested that this policy makes it less attractive to invest in certain types of closed-ended investment funds, namely venture capital investment trusts and other vehicles that make allocations to illiquid assets. Stakeholders have also suggested that the requirement for trustees to look-through to underlying investment costs may be stifling product innovation that would otherwise expand the range of products offered by DC schemes.

109. The argument presented is that particular illiquid investments, namely venture capital and growth equity (VC/GE), can offer DC schemes access to the top end of the illiquidity premium. The potential for return in these investments is high but so is the risk. As trustees become increasingly interested in investing in illiquid assets, it is argued that VC/GE represents the next potential frontier for sustained, long-term returns.

110. There are specific costs attributed to venture capital investments which tend to be higher than traditional alternatives. These include extensive research, management fees, performance fees, set-up fees etc., but all stem from the same fact that VC/GE requires greater due diligence and post-investment involvement. Stakeholders have suggested that the best way to organise this involvement and pool resources while ensuring that schemes can benefit from diversified returns across a host of VC sectors is to invest via a fund of funds structure, i.e. a venture capital investment trust.

111. The government wishes to hear more about this issue, and any proposed solution, and invites industry stakeholders to make clear their views on this concept. That is why we are asking trustees, asset managers and others to tell us more about how they treat look-through and whether this treatment is incompatible with the nature of illiquid investments.

Question 2: What is the likely appetite that pension scheme trustees have for investment in venture capital and/or growth equity?

112. If trustees choose to explore investments in such asset classes, they will need to understand how look-through should work when undertaking such an investment. Some stakeholders have stated that look-through will pose such a barrier. One argument is that the requirement to consider the costs linked to the underlying investments – the premise of look-through – will drive up the overall cost of investing in this type of vehicle to such an extent as to make it commercially unviable.

113. Of course, no matter whether look-through is required or not, those costs will still exist. The question becomes whether those costs form part of the charge cap, and so are passed onto members directly via a charges regime, or are treated as a drag on performance, involving the pricing down of units in the underlying funds. The government believes that removal of look-through in the case of closed-ended funds would not impact the underlying costs to members of pension schemes but would improve the commercial viability of such investments to trustees. As the government works with industry and the Financial Conduct Authority to set up and launch the new Long Term Asset Fund (LTAF), it will also consider this issue as it applies to this structure. We welcome views on this and the extent of the material impact on schemes’ appetite to invest in illiquid assets.

Question 3: How do you currently treat look-through when calculating the charges regime of the scheme?

Question 4: Does look-through act as a significant barrier to investment into investment vehicles that allocate to VC/GE?

Question 5: Are there more significant barriers to the success of pooled illiquid investment vehicles than look-through? If so, what are they?

114. Some stakeholders have proposed that government could pursue a regulatory solution which would remove performance fees, management fees, and the costs of underlying investments from the overarching look-through requirement. Stakeholders have also suggested it may be possible to define an asset class VC/GE to narrow the some of the exemption. We would welcome views on this option.

115. There are risks to consider. Would the government be diluting member protections and exposing members to high fees that don’t deliver high returns by removing one type of investment, which attracts high fees, from the charge cap? The government reaffirmed its commitment to member protection, including the existing charge cap, in its review published in January 2021. Any measure that might increase the accessibility of illiquid investments should be consistent with maintaining an appropriate level of member protections given the varied risk-return profile of some of these asset classes. We invite evidence on how appropriate member protections can be maintained under these proposals and any measures that can be put in place to ensure limited impact on members should illiquid investments not perform.

116. Arbitrage is another consideration. The government is committed to finding solutions to greater investment in Productive Finance, especially by DC schemes. However, we believe consideration must be given to inadvertently favouring one type of investment or structure of investments to another. Without look-through in investment trusts and other closed-ended funds, direct investment in individual funds by schemes would become relatively more expensive, at least presentationally, as costs involved in direct investment are not classified as look-through costs and would therefore still be subject to the charge cap.

117. This has ramifications for the allocation of assets and structure of portfolios that may favour one sector, asset class, or fund manager over another. The creation of inappropriate incentives such as these is clearly something the government wishes to avoid. We want to understand the extent to which the clear differences in the structure of a pension scheme’s investments, i.e. direct investment in a fund they choose or via fund of funds, generates an economic distinct activity such that the possibility of incentivising unhelpful arbitrage is minimised. We invite views on the arbitrage risk in the questions that follow. One approach could be to limit the extent to which schemes can use open-ended or closed-ended investment funds or the percentage of an individual scheme’s assets that a fund manager can hold in a fund of funds vehicle so that investments cannot be structured in a way that would intentionally avoid the charge cap. This would need to be balanced against the government’s desire not to excessively restrict trustees in their choice and use of investment vehicles.

118. The government wishes to understand all views and perspectives on this issue before making any policy changes. We understand that there are other barriers to the success of such vehicles, linked to demand, liquidity, daily-dealing etc. We would like to understand the views of industry on how the government should rank these barriers and prioritise possible solutions including the role that industry can play in addressing any barriers.

Respondents can offer an overall, rather than an individual, response to each of the following questions:

Question 6: If perceived as a significant barrier, how can the government act to ensure it is removed whilst maintaining member protection/the objectives of the charge cap? Should this change be a regulatory one or in guidance?

Question 7: Is there a risk of arbitrage? How can this be mitigated?

Question 8: Are there recognised industry definitions of venture capital and growth equity?

Question 9: Are there any other proposals that the government should consider to allow greater investment in venture capital or growth equity?

Annex A: List of respondents to Chapter 3 of ‘Improving outcomes for members of defined contribution schemes’

ABI

Aegon

Ali (individual)

Aon

AIC (Association of Investment Companies)

Association of Pension Lawyers

Association of Real Estate Funds

Aviva

Barnett Waddingham LLP

Buck consultants

BVCA (British Private Equity & Venture Capital Association)

Caritas International Independent

CFA Society UK

Creative Pension Master Trust

Dalarida Trustees

Gowling WLG

Hymans Robertson LLP

IFoA (Institute and Faculty of Actuaries)

Investment Association

Isio

John Forbes Consulting

Lane, Clark and Peacock

Legal and General