CFM96890 - Interest restriction: joint ventures: group ratio (blended) election: interaction with the non-consolidated investment election

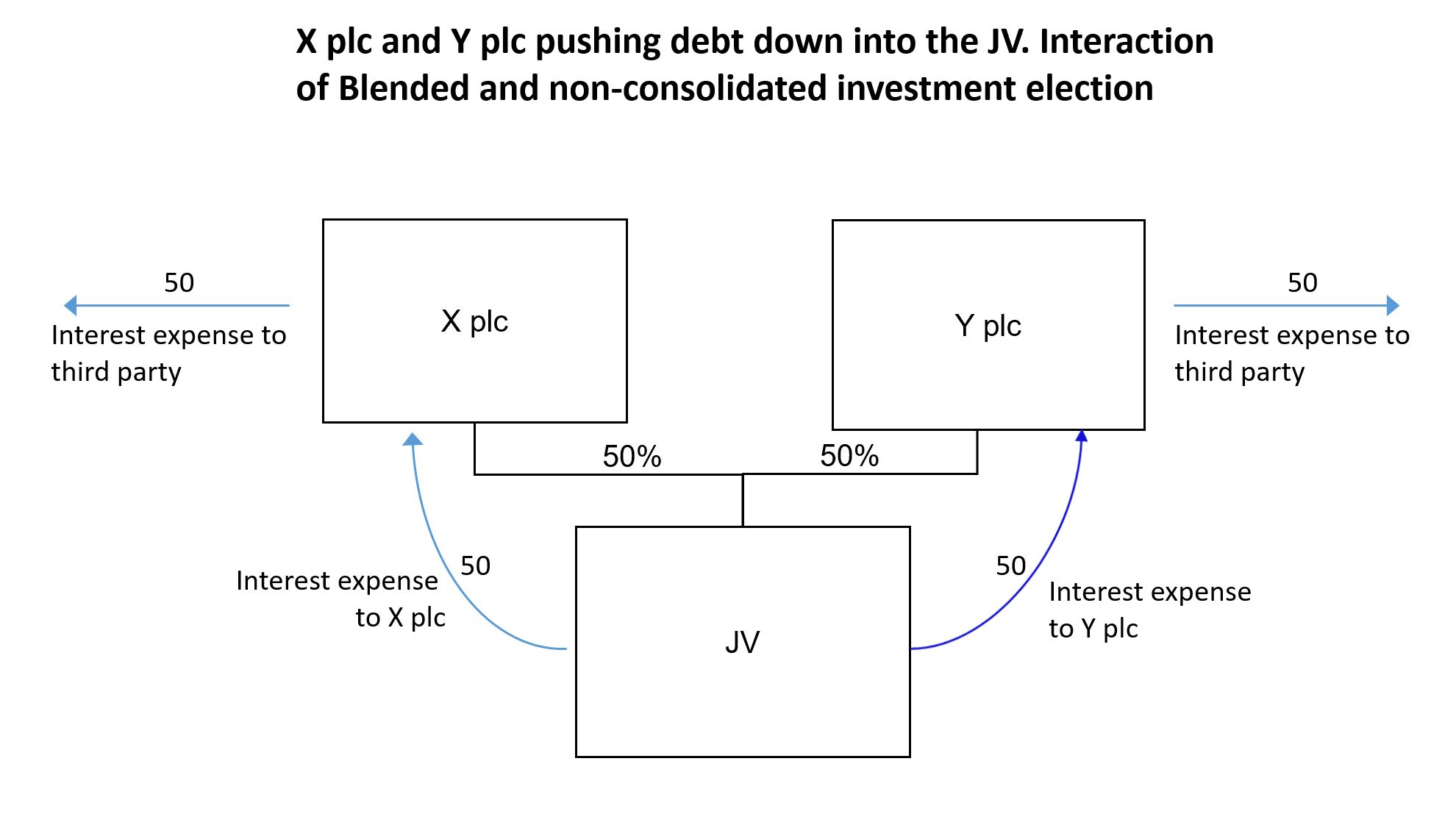

A joint venture (JV group) can be funded by the investors obtaining debt from third parties and pushing this debt down into the joint venture. In this circumstance all of the net tax-interest expense in the joint venture is related party debt and as a result the qualifying net group-interest expense for the JV group is nil. Therefore it is advantageous to use the group ratio (blended) election to calculate a group ratio for the JV group.

However if the only borrowing from the investors is from the third parties which is then pushed down then the investors will not have any qualifying net group-interest expense themselves. The interest expense to the third party will be covered by the interest receipt from the JV group. Therefore the investors will not have a group ratio so the group ratio (blended) election would be ineffective.

In these circumstances it would be advantageous for the investors to elect into the interest allowance (non-consolidated investment) election. Such an election would not make any difference to the amount ultimately disallowed in the investor groups as their aggregate net tax-interest would be nil. However this benefits the JV group as it provides the investors with a group ratio that can be used by the JV group in calculating its group ratio.

CFM96900 below outlines the flexibility that the JV group has to specify whether it treats if investors of having made elections or not irrespective of whether an election has been made by the investor.

The interaction of the two elections can be illustrated by means of an example.

Link to the structure diagram for this example

{kind=link}

X plc takes out a third party loan which has an interest expense of 50. This loan is pushed down into JV with the same terms so the JV pays an interest expense of 50 to X plc. Y plc mirrors the lending of X plc. X plc and Y plc have no other income apart from their share in the JV and the interest income on the loans to JV.

| Accounts | X plc and Y plc | JV | X plc and Y plc Group |

|---|---|---|---|

| Operating profit | - | 200 | - |

| Third party interest expense | - 50 | - | - 50 |

| Interest income | 50 | 50 | |

| Related party interest expense | - | - 100 | - |

| Share of profits of JV | - | - | 50 |

| Profit before tax | - | 100 | 50 |

- X plc Group share of profits from JV - 50%

| Calculation of QNGIE | X plc Group |

|---|---|

| QNGIE in X plc | 50 |

| Share of JV QNGIE | - |

| Total QNGIE (A) | 50 |

| Calculation of Group- EBITDA | |

|---|---|

| Group-EBITDA of X plc Group | 50 |

| Reduction in Group-EBITDA from JV profits | -50 |

| Increase in share of Group-EBITDA from JV Group-EBITDA | 100 |

| Group-EBITDA (B) | 100 |

| Calculation of blended Group ratio | % |

|---|---|

| Group ratio of X plc | 50% |

| Similarly group ratio of Y plc | 50% |

| Blended group ratio (50% of 50% + 50% of 50%) | 50% |

| Calculation of interest restriction | JV |

|---|---|

| Tax-EBITDA | 200 |

| Group ratio from blended election | 50% |

| Interest allowance | 100 |

| Net tax interest expense | 100 |

| Interest restriction | - |

| Group ratio debt cap (blended net group-interest expense) | 100 |

| Interest restriction | - |

X plc and Y plc

The investment allowance (non-consolidated election) ignores the loans to the JV so X plc and Y plc have qualifying net group interest expense of 50 from the third party expense. X plc and Y plc take their share of group-EBITDA from the JV. This is 50% * 200 = 100. Therefore the group ratio in both X plc and Y plc is 50%

JV

When the group ratio (blended) election is applied the blended group ratio of JV is 50%*50 + 50%*50 = 50%. If this is applied to the tax-EBITDA of JV this gives an interest capacity of 100 which corresponds with the net tax interest of JV. This means that there will be no restriction.

The blended debt cap is restricted to the qualifying net group-interest expense of X plc and Y plc that is used to fund JV. As in this case the funding is solely used to fund JV then both X plc and Y plc have an applicable net group-interest expense of 50 which gives the blended net group-interest expense of JV as 100. Therefore this does not create an additional restriction beyond the application of the blended group ratio.