The Government Efficiency Framework

Published 19 July 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/the-government-efficiency-framework/the-government-efficiency-framework

Foreword - Cat Little, Second Permanent Secretary of HM Treasury

Driving efficiency is a mindset. In making sure we are maximising output for the minimum input, and in spending money on the things that most effectively achieve our intended outcomes, we make the most of taxpayers’ money. Delivering our public services efficiently is a core leadership responsibility for everyone.

This guidance is to support departments in delivering efficiencies – it is for every public servant involved in delivering our public services. It establishes a framework for how we should categorise and track the efficiencies we are delivering; in standardising our reporting, we create more consistency in our approach across UK public services. In doing so, we foster trust through greater transparency.

We should deliver efficiently, and embed productivity into everything we do, but we shouldn’t lose sight of outcomes and what we are trying to achieve for the public good. This guidance establishes that when we think about delivering efficiency in government, we are thinking about whole-system impacts and using high quality data. As public servants, we need to make sure that decisions are considered properly, that we assess and quantify benefits realisation in all that we do.

I hope you find this guidance useful. We should strive to continuously improve how we deliver benefits in government spending. It is a fundamental part of our role as public servants in the stewardship of public funds.

Using this guide - Tom Wipperman, Strategic Finance Director in the Ministry of Defence

Every day we make decisions on how to improve delivery of public services and drive more efficiency. The effectiveness of our decision making and quality of our outcomes is driven by the quality of our data. When we do this well, we are enabling public servants – from teams delivering on projects or providing services, to senior leaders and ministers making decisions – to administer public funds with the best possible information to best possible effect.

How we report and track efficiency savings is a key component of delivering value for taxpayers’ money: to support departments and other public sector bodies with this, we have produced the Government Efficiency Framework. It sets out what efficiency is, how we should categorise it, and best practice in gathering high quality information to best inform our decision making.

Departments are trying to deliver different kinds of efficiency savings. This guidance therefore takes a principles-based approach to the drivers of efficiency savings. There is a reporting framework and suggestions for best practice in gathering high quality data, reporting, capturing benefits realisation, and assurance. You will find examples, suggestions, and templates to help.

This is for everyone involved in the identification, monitoring, and tracking of efficiencies. It should equip you with an underpinning understanding of why, as well as provide clear information on how you can do this effectively and consistently.

1. Driving efficiency in government

The government is committed to continue identifying ways to work more efficiently, and so reduce the running costs of government and our public services. Day to day, departments are making decisions to live within their departmental expenditure limits (DEL) totals – and should seek to drive continuous improvement and improve the productivity with which government services are delivered, while maximising opportunities to drive efficiency.

This document sets out a standard approach and framework for the tracking, monitoring, and oversight of efficiency savings. It provides the definitions and reporting standards for efficiency savings, best practice guidance for reporting processes, and guidance on how department should be reporting efficiency savings to HM Treasury. Effective, standardised reporting ensures that we understand what is being done well and where improvements can be made.

Departmental priorities differ but underpinning the delivery of efficiencies are the same fundamental principles for reporting and governance, supported by effective use of data and tools. This guidance therefore also consolidates current best practice across departments to give senior leaders a blueprint for how to implement, improve, or enhance their efficiency reporting processes.

Efficiency and productivity

Efficiency means being able to spend less to achieve the same – or greater – outputs, or to achieve higher outputs while spending the same amount. It does not include decisions to reduce costs with the intention to achieve less – these are non-efficiency savings. Productivity, at a high level, measures how many units of output are produced from one unit of inputs – and so improved productivity is a means to achieve greater efficiency.

This guidance sets out the framework for how departments should report their efficiency savings. Definitions are set out below with examples to help bring this to life.

1.1 How to use this document

This guidance sets out efficiency definitions and reporting standards – which departments are expected to adopt across their efficiency reporting. It also sets out recommendations for best practice data gathering.

Departments are expected to adopt the framework – to categorise their own efficiency savings – within the 23/24 financial year, and agencies, non-departmental public bodies, and arm’s length bodies from the 24/25 financial year – further guidance will be shared in due course.

Alongside the framework, we will issue reporting guidance on how departments should report their progress to HM Treasury (and so their spending team) in delivering any efficiencies assumed in their spending plans. This guidance will also include expectations for reporting non-efficiency savings, to provide a complete picture.

Updates on progress will be reported to HMT, and begin within this financial year for central departments. Reporting guidance will be focussed on the process for doing this, featuring any necessary templates and details on deadlines, contacts, and frequently asked questions.

The intention is that this framework establishes a centralised, consistent, and enduring process for departments to track and report on their efficiency savings. This will simplify requests for information for departments, ensuring a systematic approach.

This guidance will be refreshed on an annual basis.

1.2 Who this is for

The definitions and framework apply to all bodies classified by the ONS to central government; this means all central government departments and their agencies, most non-departmental public bodies and arm’s length bodies (ALBs). The sector classification of bodies assessed by the ONS is published in their Sector Classification Guide publication; the Treasury also publishes a guidance note on sector classification.

Organisations in scope of reporting requirements will be set out in the accompanying reporting guidance.

We all have a responsibility for delivering services as efficiently as possible for the taxpayer – this guidance is for all public servants. It is expected to be adopted by departmental accounting officers, finance directors, chief operating officers, budget holders, senior responsible owners, and finance/project teams – those involved with the monitoring, delivery, appraisal, and evaluation of efficiency savings in government.

Accounting officers and finance directors are expected to implement the reporting framework set out here as the core method to monitor the efficiency savings being delivered within their organisations. As part of their wider duties for supervising reporting obligations and managing risk, departmental boards and committees should provide oversight and seek assurance that the appropriate processes are in place. The public expects transparency and accountability with the management of public finances; placing savings into a consistent, transparent framework is a vital component of ensuring public trust.

Senior responsible owners (SROs) and budget holders are expected to embed the framework within their business areas and ensure that reporting structures enable the monitoring of efficiencies against the four categories set out in the guidance.

2. Defining efficiency

In simple terms, efficiency means being able to spend less to achieve the same or greater outputs, or to achieve higher outputs, while spending the same amount. Efficiency does not include decisions to reduce costs with the intention to achieve less.

There are two different categories of efficiency – these are set out below.

Technical

Government can achieve efficiency gains by carrying out activities with fewer resources (such as people and buildings); or to a higher standard without additional resources - this is a ‘technical’ efficiency. Technical efficiency refers to achieving a given output for the lowest level of input.

For example, if a department operates a call centre, and has a target of processing 5000 customer queries per day but can do this with half the number of staff (because it has automated the logging of customer queries, triaging them to the correct team) then it requires less resource input, but for the same outputs.

Allocative

Efficiency gains can also be realised by allocating – or reallocating – resources on those activities with the best ratio of costs to the benefits achieved where this can be calculated (this is an ‘allocative’ efficiency). Allocative efficiency refers to maximising outputs or outcomes for a given input (by changing processes or inputs).

For example, if a departmental priority outcome is to eradicate a disease, it may move from treatment (dealing with the disease at the point that patients have it) to preventative support (for example, early intervention with vaccines at reduced cost). The outcomes are the same, but the allocation of resources shifts to a more efficient approach.

2.1 The drivers of efficiency

There are five broad drivers of efficiency[footnote 1]. It is likely that budget holders (and so departments) will base many of their efficiency plans around these types of activity. The five drivers are set out below for information, with examples on how these could materialise within different areas of government.

2.1.1 Markets and competition

In some situations, departments can leverage markets and competition to control their input costs. For example, where there is high quality data about common categories of cost and associated quality measures in genuinely comparable peer groups, unit cost benchmarking can provide valuable insights to help manage costs.

Other areas to consider are:

- New entry competition/market creation

- Intelligent outsourcing

- Strengthened incentives

- Cost benchmarking

2.1.2 Organisation and workforce

Departments can create efficiencies through carefully considering their organisational design. Examples may include options such as co-locating responsibility for both policy and operational teams together to avoid complex policy implementation challenges. Departments might also concentrate on workforce capability, such as cross-training staff who deal with formal correspondence to handle written, verbal and online enquiries, improved managerial quality, or building an agile workforce.

Other areas to consider are:

- Sharing services

- Pay systems

- Sharing best practice

- Capability and leadership

- Organisational structure

2.1.3 Service re-design and alternative delivery mechanisms

Departments can take advantage of improvements in cloud technology and shared services to encourage greater self-service for HR and finance processes. Many departments are currently planning significant back-office transformation as part of the Shared Services Strategy for Government. Departments can lean into this programme to identify processes that can be shared between multiple departments in their cluster, leading to greater efficiency. This could include reducing effort in case management through automation, reducing the reliance on highly customised, high-cost IT systems (and so lower associated supporting contracts/costs), or making journey improvements to reduce failure demand.

Other areas to consider are:

- Prevention/early detection

- Front-line service integration

- Reconfiguring services

- Invoicing users in service design

2.1.4 Technology efficiencies

The use of digital, data, and technology can reduce costs on a departmental and cross government level. Initiatives include: improving efficiency by reusing technology solutions (taking a ‘buy one, use many’ approach), sourcing commodity solutions to reduce operating costs, reducing reliance on legacy (higher cost) IT systems.

Other areas to consider are:

- Effective use of IT

- Effective use of digital services

- Technological advances

- Effective use of data

2.1.5 Digital transformation

Initiatives to drive digital transformation efficiencies could include: substituting manual processing with digital solutions and automation, reducing paper processing through automation and online communications, increasing the adoption of digital channels instead of higher cost offline channels, leveraging data to increase the effectiveness of public service delivery, or making journey improvements to reduce failure demand.

3. Tracking efficiency

When considering efficiency opportunities within programmes or business areas, both technical and allocative efficiencies can be measured in line with the approach to carrying out cost-effectiveness analysis and cost-benefit analysis set out in the Green Book.

3.1 Categories

If efficiency opportunities are monetisable, realised efficiency gains can be categorised as either as cash releasing or non-cash releasing. Cash releasing means it could lead to a direct reduction of departmental spending on an activity, project, programme, or policy; non-cash releasing means there is a benefit (which could be either monetisable or non-monetisable saving) but it does not lead to a direct reduction in spending.

Cash releasing

- i. Cash releasing savings

Non-cash releasing

- ii. Monetisable non-cash releasing savings

- iii. Quantifiable but non monetisable benefits

- iv. Qualitative unquantifiable benefits

3.2 Monetisable benefits

While all quantifiable benefits could be monetisable in some way, this guidance is focused on budgetary impacts and financial reporting. In this case, the distinction between cash releasing savings and monetisable non-cash releasing benefits is one of choice – there will have been a choice on whether budgets should be reduced to maintain a level of output or accept higher outputs on the same level of spending (and in this scenario, it would directly release cash if the budget was reduced).

As this framework is to aid financial reporting, it focuses on the cash releasing savings and monetisable non-cash releasing savings. Departments should also be reporting and evaluating the benefits delivered through (iii) and (iv); these are not in scope of this framework and are briefly reviewed in this framework but set out with extensive guidance in the Green Book and Magenta Book and will have different monitoring processes. This is discussed in section 3.5.

3.3 Examples

Cash releasing savings: for example, reduced estate footprint that will create capital receipts and reduced maintenance costs – if an organisation has several underused or unused buildings, rationalising and consolidating its estate would reduce energy/occupancy costs – which will directly (and sustainably) reduce spending on its estate and so department’s budget

Monetisable non-cash releasing benefits: for example, a new IT system that will save users time so they have more resource for other activities – if an organisation processes 100 customer queries per hour with 10 members of staff, but through improving the telephony process is able to increase this to 150 queries per hour with the same level of staff, there is a monetisable benefit (the improved resource cost of queries) as the budget has not been reduced to maintain 100 queries per hour - so departmental spending is not directly impacted

Quantifiable but non monetisable benefits: for example, if an agency is making improvements to the roads in a town, and can do this quicker than initially planned, the wider economic benefits are monetisable – e.g., improved access for commercial uses and less traffic – but the benefits do not directly impact a department’s spending and so are not monetisable to the department

Qualitative unquantifiable benefits: for example, if a department improves the efficiency of a service offered to the public and so reduces the time it takes for a member the public to resolve a query, there are also qualitative benefits – such as public satisfaction with the service – which are not quantifiable but contribute to the wider public value of the efficiency measure

3.4 Cash releasing savings

Cash releasing savings lead to a direct reduction in a department’s spending on an activity, project, programme, or policy, leaving surplus budgets that can be reprioritised, reinvested, or returned to the Exchequer.

To report cash releasing savings, the following principles must apply:

- They should be calculated with quality data. The calculation is likely to be based on baseline cost information, a counterfactual spending profile (which may involve estimates and assumptions) and outturn spending data. This should happen within a financial year, so that the saving can be reported against the annual budget.

- They should release cash from a department’s budget, net of costs, without causing unplanned or unintended consequential costs elsewhere in the department, other government departments, or local government. This is usually considered through business cases and impact assessments.

- There should not be an adverse impact on performance or outcomes. Savings must not adversely impact on the achievement of a department’s strategic priorities, as defined in a department’s Outcome Delivery Plans (ODPs). Departments should be able to demonstrate that because of reforms, the department and sector is delivering better value for money overall.

- They should be sustainable and should not be reallocating or deferring costs to future years. Sustainable efficiencies must exist in the year they are realised and remain in all subsequent years at equal or greater value. Cost reallocation or deferral takes place where there is a simple movement in cash across a year end which does not in fact relate to a total net reduction in waste or inefficiency when the two years are taken together. For example, where a project is delayed by six months and therefore there is a cash positive impact on the current year at the cost of future years, this is not a saving.

- Cash releasing savings should be scored once against the year in which they are realised, net of any double counting between different organisations (e.g., different departments). Departments (or ALBs working with departments) should decide how to report these efficiencies, and where accountability sits. Functional efficiencies will likely also be reported; these are not additive and double counting must be avoided through clear reporting of data.

- The nature and calculation of cash releasing savings should be readily understood, calculated with quality data, and likely to be seen as reliable, reasonable, and verifiable by an impartial third party. Savings must have been realised by the point at which they are reported as an achieved saving. Any saving should be readily defendable to the National Audit Office (NAO), GIAA, or independent auditors, well evidenced with documentation.

- The nature of the saving should be clear, for example identifying savings that relate to procurement, or pay (which would also identify the Functional area).

- Increasing income from fees or charges does not count as a saving or technical efficiency as it does not lead to reduced spending.

If a saving materialises because a programme is stopped or cancelled this is not a cash releasing efficiency saving as the original baseline outcome has not been achieved; this would be considered a (non-efficiency) saving.

If an intentional decision has been made to reallocate or reprioritise funding to an area which will deliver against another aspect of a department’s outcome delivery plan with improved outputs and outcomes (which involves stopping or cancellation another area of spending) this would be an allocative efficiency (for example, shifting spending priorities from treatment to prevention – still achieving the outcome of reducing the prevalence of a specific health issue).

If a decision has been made to reallocate or reprioritise funding to achieve a wholly different outcome or ministerial priority, or with the intention to reduce or achieve less than the original outcome, this is a reallocation and would not be considered and allocative efficiency. Through this process, a department may also realise non-efficiency savings.

3.4.1 Efficiency savings categories

For cash releasing savings to be realised some output metrics may decrease, but the benefits (in terms of outcomes delivered) must not be adversely affected.

There are several ways in which cash releasing savings could be realised or delivered – this list is indicative only, as there will be many ways of finding and driving efficiency:

Volume or scope reduction

Savings secured by a supplier resulting from a reduction of planned volume or scope delivered. The reduction must not impact the benefits (outcomes) derived.

HR and workforce

Efficiency savings can be delivered through the reduction of staffing required to deliver the same level of public services through better use of technology, or by reducing costly contingent labour and consultancy contracts through the development and building of skills in-house.

Estate rationalisation

The creation of a more efficiently operated estate (supported by the acceleration of centralisation of general purpose property under the Government Property Agency) can deliver operating cost savings through estate rationalisation and consolidation – leading to reduced running costs.

Technology efficiencies and digital transformation

Investing in online and digital services can lead to cost savings by delivering service outcomes at a lower cost compared to manual or offline processes. By embracing digital transformation and automating manual processes, public services can achieve greater efficiency. For example, implementing an online solution can reduce the need for in-person visits, paperwork processing, and manual case management. This investment in digital solutions prevents future spending on physical infrastructure, staffing, and administrative tasks, while still delivering efficient and effective public services.

Fraud prevention and recovery

Reducing irregularity drives efficiency and better value for money in government. Where fraudulent money is either recovered or prevented, this will either impact Annually Managed Expenditure (AME) or DEL budgets depending on the budgetary treatment. Departments should reflect recovery and/or prevention as an efficiency if it meets the criteria outlined above; whilst the Government Efficiency Framework is primarily intended to be used as part of DEL budgetary management, users should use the framework to categorise any AME efficiencies that they oversee.

Some efficiency plans may be realised through upfront investment (known as an ‘invest to save’ measure). If the measure achieves an overall reduction against the original delivery plans for the output or outcome, including the investment costs, this would be considered an efficiency saving.

3.4.2 Considerations

This section clarifies distinctions where cash is saved but is not measured as an efficiency saving:

Cancellation of a policy measure or legislation and tax changes

If a decision is made to deprioritise or cancel a policy measure, initiative, or programme, this is not an efficiency saving; please see above (section 3.3) on the distinction between cancellation and reprioritisation as an allocative efficiency. Similarly, if there are legislation/tax changes (e.g. to the minimum wage) resulting in savings to a department’s budget, this is not an efficiency saving.

Underspending

If there is an underspend, there may be several reasons for this being because of efficiency impacts – however where it is because of less than forecast demand or optimism bias in the forecast, this is not an efficiency saving. This includes unexpected windfalls.

Lower than expected inflation rates may also lead to direct savings within a department’s budget. This should not be calculated as an efficiency saving as an output or outcome is not being delivered more efficiently (but it would be considered a non-efficiency saving).

Liability not crystalising

A contingent liability is not usually forecast within a budget (instead it is a risk); where a liability has not crystalised this is not an efficiency saving.

3.4.3 Example - efficient use of data

Departments (internally and across government) can be more efficient by reusing technology effectively – ‘buy once, use many times’. Working collaboratively across departments can help to identify opportunities to do this; effective governance through internal controls can help to identify opportunities within a department.

One cross-government example is the contract with Amazon Web Services (AWS) and the Crown Commercial Services (CCS), through which AWS, which enables adoption of cloud computing, agreed to treat participating UK government and public sector organisations as a single client – offering savings opportunities.

Several departments have also moved to centralise access to technology and data systems through controls. This means that when procuring data sets or access to data and technology through contractual agreements with external providers, there is a mechanism for ensuring that duplications or similar procurements are identified early and so consolidated, or data/technology extended so that the department is using its existing services more efficiently.

This could create either (or both) cash releasing and non-cash releasing efficiency savings. The Chief Digital and Data Office in the Government Digital Service and the Crown Commercial Service can provide support with this.

3.5 Monetisable non-cash releasing savings

Monetisable, non-cash releasing savings (referred to from this point as a non-cash releasing savings) are a form of monetisable, non-cash releasing benefits as set out in the Green Book. These are savings that will result in monetisable efficiencies for a department or organisation – but do not deliver direct spending reductions and so cannot not be directly reported against a department’s budget. For example, non-cash releasing savings could be because of increased productivity within a service with no reduction to service costs.

The distinction is also one of reporting, as within a department there will ultimately be a choice on whether budgets should be reduced to maintain a level of output or accept higher outputs on the same level of spending (noting that reducing spending on staffing has other associated costs).

The principles underpinning accurate reporting of non-cash releasing savings are similar to those underpinning cash releasing savings, with caveats for reporting.

- There should not be an adverse impact on performance or outcomes

- They should be sustainable and should not be reallocating or deferring costs to future years

- They should be scored once, net of any double counting between different organisations

- The nature and calculation of non-cash releasing savings should be readily understood, calculated with quality data, and likely to be seen as reasonable and comprehensive by an impartial third party

- The nature of the non-cash releasing saving should be clear, for example identifying if it relates to procurement, or pay

- Every non-cash releasing saving should be evidenced through a comprehensive methodology, which has appropriate assurance; this is discussed in chapter 5

3.5.1 Categories

Non-cashable releasing benefits will often be categorised (as above, this list is not exhaustive) as:

Improved demand management

A process whereby teams ensure that the demand for goods and services is appropriate to business need, for example by reducing demand or replacing demand with an existing substitute. For example, if a forecast demand of 100 software licences is made by a government department, but reduced to 80 through negotiations, the core outcome is met but a saving of 20 licences is claimable.

Improved resource management

A benefit where an improvement leads to more for the same. For example, an improved process enables fractions of overall headcount being able to maintain output and complete additional activities resulting in improved output and outcomes (where it can be quantified in monetisable terms).

3.6 Non-monetisable benefits

Through undertaking a benefits appraisal[footnote 2] you will be able to identify benefits that are quantifiable and can be expressed in monetary equivalent terms – every reasonable attempt should be made to quantify benefits, even if they cannot be expressed in monetary equivalent terms.

Non-monetisable benefits are those which cannot be valued in a monetisable way, or are not easily monetisable. Measuring the impact of these kinds of efficiencies should be considered at the business case stage, within a department’s Outcome Delivery Plans, or through evaluation and appraisal methods as set out in the Green Book and Magenta Book. Measuring these kinds of efficiency benefits is not within this framework’s scope, but overviews are provided below to ensure that consideration of an efficiency is considered in a systematic way.

3.6.1 Quantifiable but non monetisable benefits

Not all efficiency benefits will be measured in monetary times but are still quantifiable (for instance, the unit output may not be monetisable). Quantifiable but not monetisable benefits should still be measurable and quantified to show the wider impacts of an efficiency measure.

3.6.2 Qualitative unquantifiable benefits

Qualitative unquantifiable benefits require qualitative measurements to evidence the efficiency being delivered.

Where quantification is particularly challenging, because the evidence base is insufficient or unreliable or the research costs would be disproportionate to the expenditure, it may be acceptable to express a benefit in qualitative terms; but even then it should be possible to provide evidence on the likely order of magnitude of the benefit.

When a qualitative or non-monetised benefit is considered too important to be ignored in the decision, a separate calculation and judgement needs to be made about whether its cost is ‘a price worth paying’ in terms of its additional value. This calculation provides the basis uponwhich alternative options without these benefits can be generated and appraised.

Qualitative assessments should be thorough and evidenced through techniques set out in the Green Book such as the Multi Criteria Decision-making Analysis (MCDA).

3.6.3 Monitoring

In all cases, the appraisal of benefits that cannot be expressed in monetary equivalent terms should be grounded in a review of the best available evidence. The evaluation of similar interventions previously undertaken usually provides a particularly important source of evidence.

The quantifiable (non-monetised) and qualitative benefits should be recorded in a Benefits

Register (as per Green Book guidance) with their sources and assumptions

4 Data and reporting

This section sets out the effective use of data to monitor efficiencies, and the appropriate tools to maximise monitoring effectiveness. It explains the minimum expectations, best practice, and steps to make sure better data standards are embedded across organisations.

Departments will need to, at minimum, have central data monitoring processes in place to oversee the delivery and realisation of cash releasing efficiency savings as agreed with HM Treasury; this will simplify reporting processes so that departments are reporting once, in a systematic, regular way.

HM Treasury uses this information to understand the overall efficiencies being delivered across government and so inform longer term planning. The data should therefore be accurate and timely to ensure that decisions are made with accurate information.

Data is an asset. In this context, it enables effective decision making, to ensure that senior leaders and ministers understand the impacts and delivery of efficiency initiatives. This ultimately leads to improved service quality, greater efficiency, reduced costs of public services, and an improved ability to measure the impacts of policies and programmes.

4.1 Reporting efficiencies

Accounting officers should ensure that there is an efficiencies reporting process embedded across all business areas. This should be based on what is outlined in this framework and the reporting guidance that will accompany it.

Efficiency opportunities may be identified through different channels – including central planning targets and so via senior decision makers, or within specific areas of a business at the budget holder (or SRO) level. It is possible that an identified efficiency opportunity has spread accountability across different business areas. This should not impact accountability, as roles and responsibilities should be agreed together and clear across the different business areas of a department.

As each budget holder is accountable (through their delegated accountability) for the management of their own business area’s budget, they are also responsible for the financial data being reported to finance teams. Where a budget holder is responsible for a delivery of cash releasing savings, they should work with their finance business partner or finance team to report savings data. Finance teams will also be able to support budget holders with appropriate guidance, sharing best practice, and ensuring reporting systems are fit for purpose.

The efficiency target for each business area (where relevant) should be clear and agreed between the budget holder and finance teams. There should be a clear understanding of the baseline and expectations on delivering outputs against this. Finance teams in turn discuss efficiency plans and delivery with HM Treasury.

This information should be used to inform a central dataset which aggregates the total departmental savings being delivered. This should be mapped against HM Treasury’s reporting requirements (as set out in the reporting guidance, which is shared with departmental finance teams).

4.2 HM Treasury reporting expectations

HM Treasury will monitor the delivery of efficiencies and require reporting from departments. This process seeks to understand whether the level of cash releasing efficiency savings agreed in financial plans has been delivered on time and to the value expected.

To enable reporting to HMT, reporting expectations will be internally issued through separate guidance. To enable this, finance teams, with budget holders, should internally track:

| Departments should track | Further information |

|---|---|

| What the efficiency measure is, and what is driving it | High level information about the efficiency (the business area), what it is, what business areas it impacts, how the efficiency will be delivered |

| Where and when the efficiency measure will be realised, with forecast cash releasing savings | Forecast cost reduction; this can be presented across either months or years (as appropriate) |

| Whether there are any impacts to other parts of the business, or another department | The impacts to outputs, profile, and any interactions should be listed at a high level |

| The total, actual cash releasing savings which have been realised to date within the Spending Review period | An aggregate summary of the actual savings achieved to date should be logged and presented against the total expected |

Best practice reporting will also include:

- Plans for any realised savings/where they have been reprioritised

- Non-releasing savings which have been realised

- Forecast non-cash releasing savings

4.3 Reporting tools

When departments collect data from across business areas, there may either be a commissioned reporting process in place (such as the use of templates to commission out for information) or a centralised reporting system where budget holders directly input into a template hosted in a department’s central database. The use of central systems which individuals can update in real time removes opportunities for error through re-entering information, and more timely reporting as teams can share live information (consideration to storing auditable data should be considered, so different stages of information are stored).

HM Treasury will provide templates on their data requirements, which departments should consider mapping against their data collection to simplify processes.

4.4 Example – organisational design and strategic workforce planning

Strategic workforce planning can enable better use of resources and so deliver allocative efficiencies within a department through organisational design (OD) - OD is the process of looking at what a programme (or department’s) outcomes and strategic objectives are and planning the most effective and efficient use of the workforce to best achieve those outcomes. It is an ongoing process, making best use of the skills and capabilities available.

One example is where a programme area has decided to review the design of its workforce. Leaders may decide to undertake a review on short- and long-term priorities with seniors in the department and reprioritise teams to focus on short term priority goals and outcomes. This may involve looking closely at grades and appropriate work to suit skills and responsibilities, as well as minimising and risk of duplication of effort and ensuring seamless information and data flows.

In the longer term, the business area senior leaders may want to undertake a gap analysis to make sure that the workforce has the right skills – identifying where to build new skills and capabilities in teams. They may also seek to minimise unnecessary cost in the use of contingent labour & management consultancy (which is usually a more expensive mechanism of outcome delivery).

This could create non-cash releasing efficiency savings, as the budget has stayed the same but through an allocative efficiency initiative, has made more efficient use of staff. The Government People Group has further materials and guidance.

5. Benefits realisation, risk, and governance

Efficiencies deliver better outcomes and more effective government, using public money in the smartest way possible. To ensure information is accurate and effective, processes to validate and realise benefits should be thorough and accounted for with appropriate oversight.

5.1 Benefits realisation

Benefits realisation planning and monitoring ensures that intended outcomes are achieved[footnote 3]. Green Book business case guidance sets out expectations for a benefits realisation strategy, framework, and outline. The Infrastructure & Projects Authority (IPA) provides users with case studies, tools and guides on how to meet those expectations. The below assumes that teams have considered this, and so focuses specifically on the realisation of efficiency savings (as benefits), ensuring governance arrangements are in place to support accurate and timely reporting and to identify risks to delivery.

Efficiency savings, when considered as a benefit, would typically be mapped through the wider benefits management of a programme or portfolio and be integrated into wider project management activities. Benefits management should also be built into, and follow, the full extent life cycle of the delivery of a change that will unlock an efficiency saving – before, during, and after. It is especially important to make sure there are plans in place to transition any benefits management work into ‘business as usual’, as most often efficiencies are realised after a project or programme has been delivered.

For an example of best practice benefits realisation reporting please see Annex A.

5.2 Methodology

A benefits management methodology outlines how the efficiency savings/benefits will be calculated and validated – it should be produced as early as possible. If an efficiency saving is identified within a business case, it would in accordance with Green Book guidance be initially considered at the Outline Business Case stage (where benefits identified will need to be valued), with a plan to realise the benefit at the Full Business Case stage. The methodology is a core aspect of this. The IPA’s benefits guidance (see footnote) provides further guidance and tools to consider before, during, and after the programme or project’s delivery.

Methodologies should be produced for each identified efficiency. Budget holders/SROs should work closely with finance teams, analysts and economists to develop these.

Every benefits realisation methodology should:

- Be supported by evidence and reasonable assumptions – this should include information on the baseline cost, clear calculations given against the baseline, and documented supporting evidence should be available

- Ensure all figures are accurately claimed, with evidence

- Ensure reporting is aligned with the right period

- Have sufficient review, verification, and governance arrangements in place

The IPA has also produced Cost Estimating Guidance which sets out best practice approach to the development of cost estimates for projects and programmes; the principles may also apply to the projection of an efficiency saving.

5.3 Governance and oversight

Appropriate governance arrangements should be in place to ensure that efficiency data and reporting is regularly reviewed and assured, and so accountable and responsible seniors are sighted and ultimately approve efficiencies reported by the organisation.

This in turn ensures that both the programme team and department can use high quality data to inform decision making, such as making interventions to enable or progress the efficiency measure.

5.3.1 Programme level oversight

Efficiency measures often are the benefit of programme, project, or portfolio. In this situation, an efficiency measure would form part of wider project delivery (and so benefits management) plan. Oversight for the efficiency savings being delivered and realised therefore are initially considered within the programme’s governance. Once the efficiency measure is being delivered, best practice involves:

- Ensure the efficiency measure is logged within the Benefits Register (as set out in the Green Book)[footnote 4]

- A tracking tool is in place to log benefits (in this case, the efficiency savings) realised to date

- The efficiency measure, as a benefit, has a clearly assigned owner

- Ensure any risks to delivering the efficiency measure are logged within the risk register

Delivery of the efficiency saving should be regularly monitored through programme governance. It is expected that review and assurance points have been agreed at the outset, using a panel, independent assurance, or ‘critical friend’ approach comprising diverse views with expertise tailored to that required in the project; the reviewers should have continuity across the life cycle of the project to improve the knowledge base and implement lessons learnt[footnote 5].

Review points should be held regularly. The panel should consider:

- Underpinning information, which should be regularly reviewed

- Uncertainties, which will vary depending on the efficiency measure’s maturity

- Risks, opportunities, and risk mitigation plans (which should also be quantified)

The budget holder/SRO should sign off the efficiency saving data at each point, and ensure this is reported to the appropriate governance and linked to wider departmental processes for measuring efficiencies.

Programme efficiency measures should also be reported to, and overseen, by the portfolio board where relevant, to make sure impacts and reprioritisation can be considered at the appropriate level.

5.3.2 Departmental oversight

Senior decision makers require good quality data to inform decision making; the process to input into the department’s aggregate position should be clear across the organisation. It is expected that the below sequence of oversight would apply:

- Departmental central finance teams commission budget holders for efficiency savings as part of wider financial reporting plans and business planning cycles

- The budget holder reports an efficiency saving (both realised and forecast) to finance teams

- The finance business partner or finance team offer support and challenge against the reported efficiency

- The efficiency saving is then formally submitted to finance teams

- At each quarter, efficiency delivery plans and realised savings are reviewed with senior finance leaders and budget holders (supported by finance teams) to ensure delivery is on track

- At each quarter, the department’s executive committee/board should receive efficiency delivery information for review and consider these against a department’s Outcome Delivery Plans

5.3.3 Risk and Assurance

Risk and opportunity monitoring and reporting is a requirement for effective financial management, as set out in the Orange Book, Managing Public Money, and Consolidated Budgeting Guidance.

As part of the delivery and realisation of an efficiency measure, both should be considered – for the purpose of this guidance, the definitions of risk and opportunities is concerned with financial management.

Risk considerations begin at the beginning: when policies and projects are being formulated, consideration of risks to achieve these efficiencies should be considered and captured at that stage. Then, at every stage of review of efficiency delivery, decision makers should consider the risks to delivery and realisation through financial risk reporting. This is because efficiency savings may be:

- Necessary for the successful implementation of a wider portfolio of work – and so programme budgets may be impacted if there is a high risk to realisation of benefits as planned

- Already be factored into a departmental budget – and so risks to delivery could risk a department breaching control totals

If efficiencies are not being delivered as planned, programme teams must intervene as early as possible, notifying senior leaders to ensure that all possible mitigations have been considered.

Where plans are not on track, and have not been successfully mitigated, departments must notify their Treasury spending team.

5.3.4 Departmental boards

Accounting officers and a department’s board should have oversight of efficiency delivery and realisation plans, supported by its Audit and Risk Assurance Committee (ARAC) – who should in turn proactive support in advising on and scrutinising risks, and audit assurance requirements.

The board should, when considering delivery of efficiencies:

- Consider any financial risks and opportunities (including any shifting exposure), and take proactive and early intervention to mitigate where necessary

- Ensure that the appropriate assurance processes are in place so that the underpinning data to efficiency delivery and realisation is accurate, and so inform decision making

- Review and sign off reported efficiencies, in line with wider budget accountability processes

The principles and requirements around financial reporting and risk management set out in the corporate governance code apply fully [footnote 6].

5.3.5 Maturity level reporting

Cash releasing savings can take several years to materialise within a department’s budget. Best practice reporting will identify the maturity of an efficiency measure’s delivery – from inception to realisation. This enables finance teams to identify and reflect efficiencies within a wider pipeline of delivery, and so take appropriate action to make sure the delivery of efficiency savings is on track and right risk mitigations have been identified where appropriate.

Maturity level cash releasing savings reporting can be used as additional data to help inform understanding of efficiency delivery (is not a requirement); this is reflected against the below pipeline of delivery:

Pipeline – the forecasted savings

- Maturity Level 0: Efficiency opportunity identified with basic idea and savings/benefit profile generated

- Maturity Level 1: Initiative scoped, levers identified, stakeholders engaged, and an estimate of the value of resources required are established against the benefits/savings profile

- Maturity Level 2: Initiative refined with actions for delivery; stakeholders engaged and plan agreed

- Maturity Level 3: Initiative plan finalised and developed for implementation; stakeholders involved agree to transition to delivery phase

In delivery/realised – the actual savings

- Maturity Level 4: Outputs required by the initiative are complete

- Maturity Level 5: Activity to realise efficiency is complete, actual spend reflects efficiency saving realised

5.3.6 Example – property and estates

A large area for delivering property efficiencies is in maximising utilisation of a department’s estate, freeing up space for alternative uses (like sub-letting to other public sector bodies), disposals or lease exits from unused or underused properties through co-location and consolidation.

However, designing in efficiency can also help realise operating cost efficiencies or reducing future liabilities throughout the life cycle of government properties, reducing waste and minimising the negative impact on the environment. Many of these features can also be successfully retrofitted to existing properties. Examples include:

- adopting sustainable construction methods such as Modern Methods of Construction (MMC) to reduce construction cost, time and waste;

- using Passivhaus principles in design, where appropriate, so that buildings naturally maintain a comfortable temperature;

- selection of materials to reduce future energy consumption like high quality insulation, solar glazing film and LED lighting;

- installation of renewable energy generation such as solar photovoltaic cells, solar thermal panels and air source heat pumps to reduce or eliminate dependency on carbon-based heat sources;

- using intelligent building management systems to reduce the energy consumption, operating costs and carbon footprint of a building

- recycling existing property-based consumables such as office furniture in new projects, or rainwater to irrigate government land, watering plants and for flushing toilets

These initiatives could provide cash releasing efficiency savings. The Office of Government Property can provide further guidance and support.

6. Insight

This section sets out what data should be provided at the departmental level.

It is important that decision-makers undertake their duties in an informed way. To support finance leaders to do this in a board reporting context, the Government Finance Function has developed standards to guide the content that department teams produce for senior boards. The below is an addition to this, and forms part of the Board Pack Reporting Minimum Standards: Key & Subsidiary Metrics[footnote 7].

A template of how departments should be reporting to their boards is annexed (Annex B). This is intended as a guide. The information assumes that departments adopt the below guide, so senior leaders are aware of the department’s efficiency plans and enabled to make better informed decisions.

Efficiency savings

Measure

- Realised cash releasing savings

- Forecast cash releasing savings with adjustments for risk

- Historical accuracy of forecast cash releasing savings (against prior quarter actuals)

Best practice will also include:

- Forecast cash releasing savings with adjustments for risk – pipeline and in-delivery

- Non-cash releasing savings which have been realised

- Forecasted non-cash releasing savings with adjustments for risk – pipeline and in-delivery

7. Annex

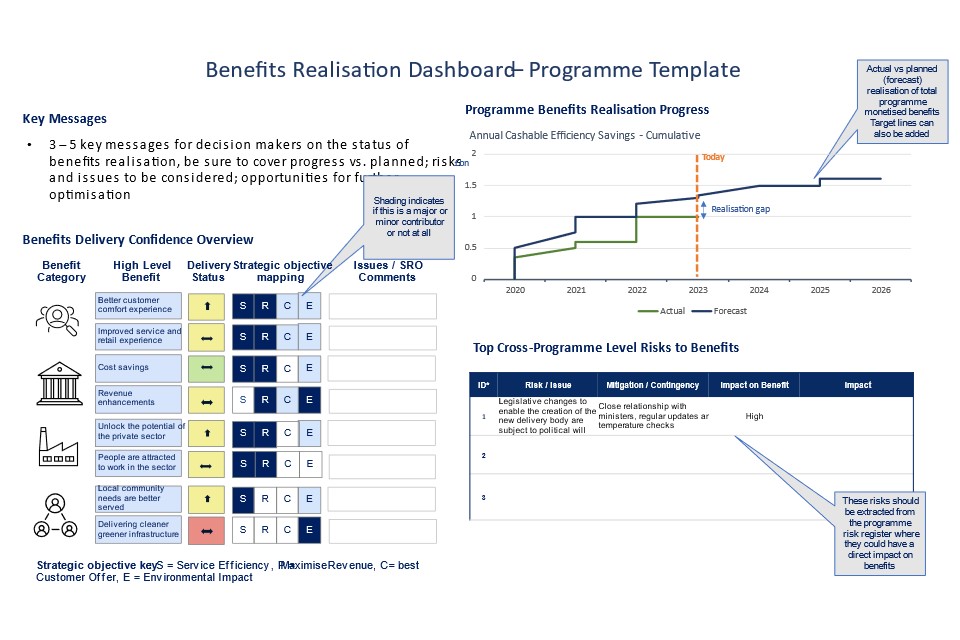

7.1. Annex A: Benefits best practice reporting to a departmental board

An example dashboard would include:

- 3-5 key messages

- A programme benefits realisation progress chart, featuring separate lines for actual vs. planned forecast

- A benefits delivery confidence overview, with coloured shading to indicate whether each benefit is a major or minor contributor

- A top cross-programme level risks to benefits chart

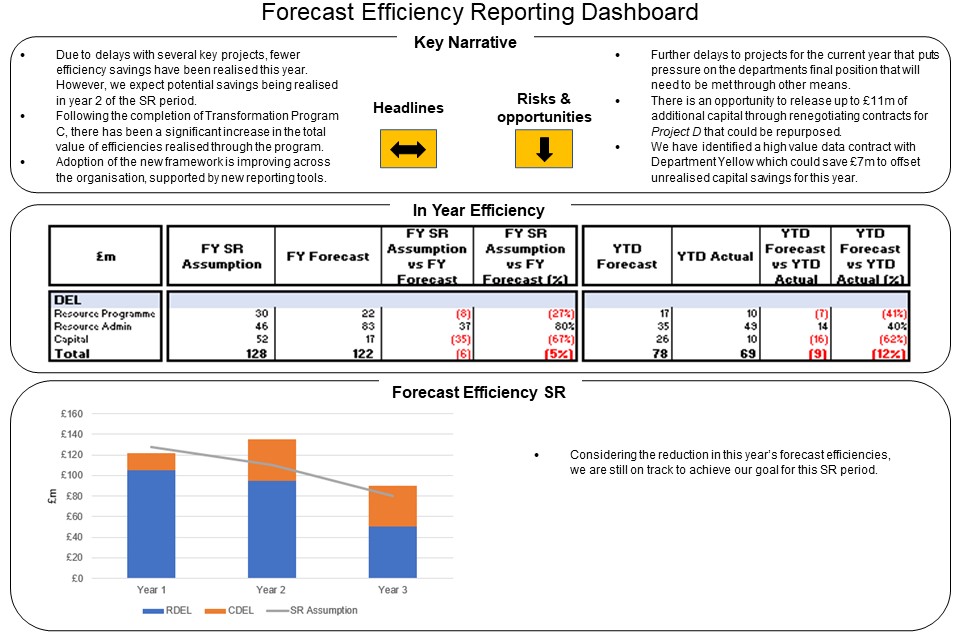

7.2. Annex B: Central dashboard for a department board

An example dashboard would include:

- A key narrative, including headlines as well as risks and opportunities

- A section showing in year efficiency

- A section showing efficiency in relation to SR

Where appropriate, departments may want to include reporting on AME efficiencies at board level.

8. Further guidance and information

-

Consolidated Budgeting Guidance Consolidated budgeting guidance 2023 to 2024 - GOV.UK (www.gov.uk)

-

Managing Public Money Managing public money - GOV.UK (www.gov.uk)

-

Functional Standards: Functional Standards - GOV.UK (www.gov.uk)

-

As identified by the Public Sector Efficiency Group in 2018 ↩

-

See The Green Book: appraisal and evaluation in central government - GOV.UK (www.gov.uk) for guidance ↩

-

See the IPA’s Project Delivery Hub : (link https://projectdelivery.civilservice.gov.uk/ ↩

-

The Green Book: appraisal and evaluation in central government - GOV.UK (www.gov.uk) ↩

-

IPA Cost estimating guidance ↩

-

https://www.gov.uk/government/publications/corporate-governance-code-for-central-government-departments ↩

-

Minimum Standards: Key & Subsidiary Metrics (civilservice.gov.uk) - please note, you will need an account on OneFinance to access this link. ↩