Research with customers whose payment required manual allocation

Published 20 July 2023

© Crown copyright 2023

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/research-with-customers-whose-payment-required-manual-allocation/research-with-customers-whose-payment-required-manual-allocation

Qualitative research with customers who have made a payment to HMRC which has failed automatic allocation and therefore had to be manually allocated.

HM Revenue and Customs (HMRC) Research Report 702.

Qualitative research conducted by Kantar Public between January and February 2023.

Prepared by Kantar Public (Rosaline Sullivan and Lucy Joyce) for HMRC.

Disclaimer: The views in this report are the authors’ own and do not necessarily reflect those of HMRC.

1. Executive summary

Each year a significant number of payments to HM Revenue and Customs (HMRC) fail automatic allocation and must be manually allocated. This is usually because the customer payment was made with a missing, incomplete, or incorrect reference number. When this happens, payment can be delayed whilst staff at HMRC attempt to match the payment to the correct customer details. In some cases, when this is not possible, a customer can appear as not having made payment. To gain in-depth insights of the causes of manual allocation and potential drivers of behaviour change, Kantar Public held 50 telephone interviews with HMRC customers whose payments had been manually allocated within the last 12 months.

1.1 Profiles of HMRC customers

Within the sample, two customer groups (frequent and infrequent payers) were identified according to their level of interactions with HMRC. The customer’s payment journey and attitudes towards manual allocation differed according to whether they were infrequent or frequent payers. These two typologies also differed by other characteristics. Infrequent payers tended to pay Self Assessment only or one-off tax payments and were less experienced and less confident dealing with finances and with HMRC. In contrast, frequent payers paid several tax types, such as Corporation Tax, PAYE, and VAT, and were more experienced and confident with both finances and dealing with HMRC.

1.2 The customer journey

Frequent payers find out that payment is due to HMRC through a variety of sources, namely their accountant, their accounting software, their HMRC account, direct communication from HMRC, or their knowledge that payment is due on a specific date. On the other hand, infrequent payers typically receive direct communication from HMRC, usually in the form of a letter. Those who did receive a letter regarding a payment due to HMRC remembered it including a reference number (either present in the payment slip or the main text of the letter), information on when the payment is due, and how to make the payment.

Participants, across both customer groups, usually make payments to HMRC through their online banking; a payment method that cannot validate the reference number. This mode of payment was found to be driven by the reassurance in the payment method (with customers having a record of the transaction); the familiarity of the method; the ability to set up regular payments through online banking; and the accessibility of being able to login from their phone. Other payment methods that customers had previously used included paying HMRC over the phone or through their Business or Personal Tax Account.

A small number of participants had previously made payments to HMRC through the authenticated digital payment methods (such as via their HMRC account) that validate the payment against the correct customer and their account. Infrequent payers (and some frequent payers) did not know they could make a payment this way. The other barriers to making a payment this way were: the belief that they could not pay Corporation Tax this way; having been previously scammed when using a website to make a payment so were now reluctant to do so; unable to see whether the payment had gone through, as there was often a delay in the account being updated; unable to spread payments or set up a direct debit; and the website being considered slow.

Prior to learning about the manual allocation, participants had been confident in the payments they had made to HMRC. Confidence emerged because they had either provided a reference number with their payment; they could see that the money had gone out of their bank account (which they believed meant that HMRC would know who had paid it); the payment information had been provided by their accountant; they had made multiple payments to HMRC this way before; or that the payment details were saved on their banking app.

Participants understood the importance of providing correct information with their payment and knew that the reference number enabled HMRC to identify who was making the payment. When asked what they thought would happen if incorrect information was provided, there was a split between the belief that HMRC would inform them there was an error to the belief that the payment would get lost or not go through.

1.3 Manual allocations

Although the majority of the sample were not aware prior to the interview that their payment had been manually allocated, those who were aware it had happened were typically frequent payers because they tend to check their accounting software or Business Tax Account regularly and had noticed a payment had not been received by HMRC.

Among customers who were not already aware, their reaction when told by the interviewer that their payment had been manually allocated varied by customer group. While infrequent payers were concerned and actively wanted to get it right, frequent payers were typically not concerned about what had happened, and, although they wanted to check they had provided the correct reference number in future, saw it primarily as a problem for HMRC to resolve.

When asked why they thought their payment had been manually allocated, customers attributed it to a range of behavioural barriers including heuristics/mental short cuts, a lack of knowledge or experience, and a lack of capability. Heuristics included assumptions that they had made a careless mistake when manually entering the reference number on their online banking web page to make the payment, for example using a previous reference number.

Other causes suggested by customers included that they had been unaware of the reference number that they had to provide and that it was difficult to manually copy a long and complex reference number with accuracy.

1.4 Future behaviour

Having been made aware during the interview (if they were not already aware) that their payment had been manually allocated, customers’ plans to change their payment behaviour in the future centred around being more careful to check that they had provided the correct reference number when making a payment.

1.5 Use of authenticated digital payment methods

When participants were informed of the authenticated digital payment methods to make payments to HMRC, the key incentive of these methods for both frequent and infrequent payers was the reassurance that HMRC auto-checks the reference number. However, a barrier across both customer groups was the perception that it was too much hassle for not enough reward. Customers liked that online banking provided a record that a payment had been made.

1.6 Customer suggestions

Customer suggestions for how HMRC could encourage customers to use authenticated digital payment methods were split into two key themes: more HMRC communications and improving the capability of digital payment channels. More HMRC communications were suggested to raise customer awareness of authenticated digital payment methods and their benefits compared with other methods of payment and that HMRC notified individuals when their payment has been manually allocated. The other area of recommendation was in the functionality of HMRC’s digital payment channels. Customers wanted to be able to use their Personal or Business Tax Account to make all types of payment, including Corporation Tax and standing orders, but incorrectly believed they could not. This demonstrates low customer awareness of the services that HMRC currently offers as it is possible to pay Corporation Tax and set up variable direct debits and budget payment plans via the Personal or Business Tax Account.

2. Introduction

2.1 Background

A variety of prompts and reasons can lead customers to make payments to HM Revenues and Customs (HMRC). Sometimes this is the customer simply wanting to pay a regular, planned, tax bill. On other occasions it may be prompted by a communication from HMRC letting customers know that money is owed. HMRC provides various methods for customers to pay. Some of these methods have built in checks so that HMRC can check that the reference numbers are valid before payment is made, these methods include making a payment online via the HMRC app, gov.uk or HMRCs Personal and Business Tax Accounts. Other payment methods rely on the customer entering the correct reference number, which is not authenticated by HMRC. This includes customers paying HMRC directly via their banking app or bank website, making a payment via cheque, or over the phone/ in-person with their bank.

Each year a significant number of payments to HMRC fail the processes which automatically allocate payments to the correct customer account and must be manually allocated. This is usually because the customer payment was made with a missing, incomplete, or incorrect reference number. When this happens, receipt of payment can be delayed whilst staff at HMRC attempt to match the payment to the correct customer details. In some cases, when this is not possible, a customer can appear as not having made payment.

HMRC would like to reduce the number of payments requiring manual allocation and commissioned Kantar Public to undertake research to inform this. Reducing the need for manual allocation should result in significant efficiency savings, reduced costs for HMRC and significant experiential benefits for customers.

2.2 Purpose of research

The interviews aimed to:

- understand the customer journey of those making payments that fail automatic allocation and explore why people choose to use payment methods that are not authenticated

- explore the barriers to using authenticated digital payment methods

- explore what HMRC could do to encourage customers to use authenticated payment methods and/or provide correct information with their payment

2.3 Method

A qualitative approach was used to gain in-depth customer insight. Findings are based on 50 interviews completed via telephone or Zoom with customers who have made a payment to HMRC within the last 12 months that required manual allocation.

Interviews were completed between 25th January and 28th February 2023.

Kantar Public recruited the participants through the sample provided by HMRC. Table 1 and 2 show a breakdown of the sample based on demographic characteristics of the participants.

Table 1: demographics of participants - primary quotas

| Tax Paid | |

|---|---|

| Self Assessment | 14 |

| PAYE and/or National Insurance | 12 |

| VAT | 6 |

| Corporation Tax | 18 |

| Customer group | |

|---|---|

| Individual | 9 |

| Self-employed/sole trader | 11 |

| Small business | 30 |

Table 2: demographics of participants - secondary quotas

| Gender | |

|---|---|

| Male | 25 |

| Female | 25 |

| Age | |

|---|---|

| Under 35 | 6 |

| 35-64 | 35 |

| 65+ | 9 |

To understand the customer journey of those making payments that fail automatic allocation, researchers undertook journey mapping. This identifies the steps that customers go through when making a payment to HMRC, what influences those decisions, and what information customers use to inform what they do. Behavioural insight principles were also applied to explore the influences on current decision-making and identify levers to influence desired behaviours.

All interviews were audio recorded and charted into an analysis framework, which was thematically analysed.

Please note, the findings are qualitative in nature, seeking to explore the views and experiences of participants. The data does not aim or allow for statistical analyses. The data presented in this report is neither representative nor generalisable and is not meant to be used to provide statistically significant results. Where relevant, differences by customer groups and tax paid are highlighted.

3. Research findings – the customer journey

3.1 Customer groups

Within the sample, two customer groups (frequent and infrequent payers) were identified according to their level of interactions with HMRC. The customer’s payment journey and attitudes towards manual allocation differed according to whether they were infrequent or frequent payers. The two customer groups are discussed below, including characteristics of each group.

Infrequent payers have a low level of interaction with HMRC. They may make a one-off payment to HMRC (for example, for a penalty) or pay Self Assessment once a year. They include individuals and those self-employed (with a low turnover), as well as new businesses who have recently started making payments to HMRC. Infrequent payers do not tend to have a Business Tax Account or Personal Tax Account. They are not confident dealing with finances and, due to lack of exposure, are not confident dealing with HMRC (considering contact a hassle or very serious).

Frequent payers have a high level of interaction with HMRC. They make multiple payments to HMRC each year, whether that is monthly or quarterly. Tax groups include VAT, Corporation Tax, and PAYE. Frequent payers include small businesses, limited companies, and those who are self-employed (with a high turnover). They have a Business Tax Account and/or Personal Tax Account and are more likely to use accounting software and an accountant. Frequent payers are confident financially and in dealing with HMRC.

3.2 Payment journeys

This section explores the customer journey, from being informed a payment is due, to preparing and making the payment, and finally to confidence that the payment has been made successfully.

3.3 How customers are informed payments are made

Frequent payers find out that payment is due to HMRC through a variety of sources, namely their accountant, their accounting software, their HMRC account, direct communication from HMRC, or their knowledge that payment is due on a specific date. Infrequent payers receive direct communication from HMRC, usually in the form of a letter.

3.4 Communication from HMRC

As expected, the level of communication received from HMRC varies across the customer groups. Infrequent payers receive few communications from HMRC. They receive a one-off letter for a penalty or receive an annual letter to say their Self Assessment is due. New businesses identified as Infrequent Payers have just started to receive communications from HMRC.

On the other hand, most frequent payers receive multiple communications from HMRC throughout the year. This is expected communication that is either sent directly to the customer or their accountant. Some frequent payers do not receive direct communications from HMRC, as they are informed payments are due through other means, such as their HMRC accounts, accounting software, or they have opted for their accountant to receive communications from HMRC.

Not all participants recalled receiving letters from HMRC. Importantly, the frequent and infrequent payers who did receive a letter regarding a payment due to HMRC remembered it including a reference number (either present in the payment slip or the main text of the letter), information on when the payment is due, and how to make the payment.

3.5 Preparations to make payment

A variety of tasks are undertaken in preparation to make a payment to HMRC, although the steps taken vary across infrequent and frequent payers.

Frequent payers undertake calculations on software to pay a VAT return, work with an accountant to calculate what and how they should pay, and log on to their HMRC Business Tax Account to find out more information on what is owed and which HMRC account to pay. However, in some instances, frequent payers automatically make a payment to HMRC, without undertaking these steps, as they are confident due to the numerous payments they have made previously.

Infrequent payers prepare their tax return by completing a Self Assessment form or contact HMRC to clarify what is owed or to request spreading payments.

3.6 Mode of making payments

Participants, across both customer groups, make payments to HMRC through their online banking; a payment method that cannot validate the reference number. This mode of payment was found to be driven by several factors, as discussed below.

Reassurance in payment method

Customers like to have a record of the transaction and to see the money go out straight away if they pay on their online bank account. This also gave them the reassurance that HMRC had received the payment. Customers are also reassured that their online banking was secure, as they were required to enter a password to login.

Familiar

Customers were familiar with using this method, often paying HMRC and other companies this way. Some log in to their online banking daily, so find it easier to make payments to HMRC at the same time.

“I make several bank transfers a day [to suppliers or other companies] so it’s quicker and easier to do it this way” (Frequent payer, female, small business)

Ability to set up standing orders

Participants who had either received a penalty from HMRC or had financial worries that prevented them from making a lump sum payment to HMRC, chose to pay through their online bank account as they were able to set up standing orders. This meant that they did not have to remember to log in on future occasions to make a payment.

“I chose [Bankers’ Automated Clearing System (BACS)] because I thought that setting up a standing order to make regular payments would be the best way [to pay off the debt]” (Frequent payer, male)

Accessible

Online banking was considered ‘accessible’ (as they are able to access it easily on their phone), quick, and easy. Adding to the perceived ease of this mode, customers’ online banking had stored HMRC’s details from previous payments.

“If I’m working away from home, I can pay using my banking app” (Frequent payer, male, small business)

“It’s so much easier for me to pay this way because I use my bank account all the time” (Frequent payer, male, small business)

Other payment methods that customers had previously used included paying HMRC over the phone or through their Business/Personal Tax Account.

3.7 Barriers to using authenticated payment methods

Only a small number of participants had previously made (or attempted to make) payments to HMRC through the authenticated payment methods (such as at gov.uk or via their HMRC account). Most infrequent payers (and some frequent payers) were unaware they could make a payment in this way.

The other barriers to making a payment this way included the belief that they could not pay Corporation Tax this way (when, in fact, they can); they had previously been scammed when using a website to make a payment so were now reluctant to do so; they were unable to see whether the payment had gone through, as there was often a delay in the account being updated; they were unable to spread payments or set up a direct debit; and that the website was considered slow, and therefore slower than making a BACS payment.

3.8 Information provided with payment

Participants remembered providing a reference with payments they make to HMRC and understood that references identify where the payment has come from.

Infrequent payers identified the reference number in the communication they received from HMRC, the pre-filled reference on their online bank account, or were provided with a reference when they contacted HMRC to ask for a payment plan.

“[The HMRC advisor] gave me a reference number which I assume was to identify that it was me that made the payment” (Infrequent payer, female, received penalty)

Frequent payers identified reference numbers through their accountant (either contacting them to ask for their VAT registration code or the accountant forwarding communication they had received from HMRC), through their HMRC Business/Personal Tax Account, in the letter they received from HMRC, or it was already saved in their online banking.

“I get the reference numbers from my VAT registration information or from the Government Gateway” (Frequent payer, female, small business)

3.9 Confidence in payment and expected outcome

When participants made payments to HMRC, they felt confident that it was correct. Confidence was based on the fact they had provided a reference; they could see that the money had gone out of their bank account (which they believe meant that HMRC would know who had paid it); they were reassured as the payment information had been provided by their accountant; they had made multiple payments to HMRC this way before; and that the payment details were saved on their banking app.

“I felt very, very confident in the payment as I can see it on the bank statement” (Frequent payer, female, small business)

“I make the payment this way every year” (Infrequent payer, male, Self Assessment)

A few challenges making payments were identified, which led to confusion when making the payment but did not affect overall confidence in it. These include challenges associated with knowledge and manual barriers. These are discussed below.

Manual barriers

Customers identified manual barriers to making payments to HMRC. Frequent payers said that when they were making a bank transfer to HMRC while checking their Business or Personal Tax account, it could be challenging to switch between both screens.

The reference number was also considered long and complicated, with a mixture of numbers and letters. Participants often had to manually copy the reference number from a letter (as they had not received digital communication from HMRC) which could further undermine their confidence in its accuracy.

“[The reference number] comes in as a letter so you can’t copy and paste it, you either get it right or you get it wrong.” (Frequent payer, male, Limited Company, BACS)

Knowledge

Participants spoke about confusion over which HMRC account to pay as they have paid more than one HMRC account previously and their online banking did not differentiate between them. This was exacerbated by the belief that the communications from HMRC do not specify which bank account to pay.

“All the accounts [listed as payees on my online bank account] are called HMRC on my account, there is nothing to show whether it is corporation tax etc. I can’t rename it” (Frequent Payer, male, small business, BACS)

3.10 What they believe happens if the payment details are incorrect

Participants understood the importance of providing correct information with their payment and knew that the reference number enabled HMRC to identify who was making the payment. When asked what they thought would happen if incorrect information was provided there was a split between the belief that HMRC would inform them and those that thought the payment would get lost or not go through.

Participants who thought the payment would get lost or not go through thought that HMRC would end up chasing them for a payment; those who thought that HMRC would inform them there was a problem with the payment believed that HMRC would either contact their accountant to let them know or let the customer know that the wrong account was paid.

“My understanding is that there would be a chase up to my accountant to let them know it had not been paid” (Frequent Payer, male, small business)

4. Research findings – awareness and causes of manual allocations

4.1 Awareness of manual allocations

Although the majority of the sample were not aware prior to the interview that their payment had been manually allocated, those who were aware it had happened were typically Frequent Payers rather than Infrequent Payers. This was generally because Frequent Payers tended to check their accounting software or Business Tax Account regularly and had noticed a payment had not been received by HMRC, or they had been notified by HMRC that a payment had not been made. When they found out, the customer had generally contacted HMRC to resolve the issue, and HMRC had explained to them that the payment had been manually allocated.

Overall, awareness and understanding of the importance of providing a correct reference number when making a payment to HMRC was high across all customer groups. Customers generally understood that the reference number allows HMRC to match a payment to their account and so was important to provide.

“I was aware that this can happen as it happened to me years ago. About 12 years ago I received a letter from HMRC saying that they had had to manually allocate a payment I’d made because I hadn’t provided the right reference number, so I know that it can happen” (Frequent Payer, male, limited company, BACS)

4.2 Reaction to manual allocations

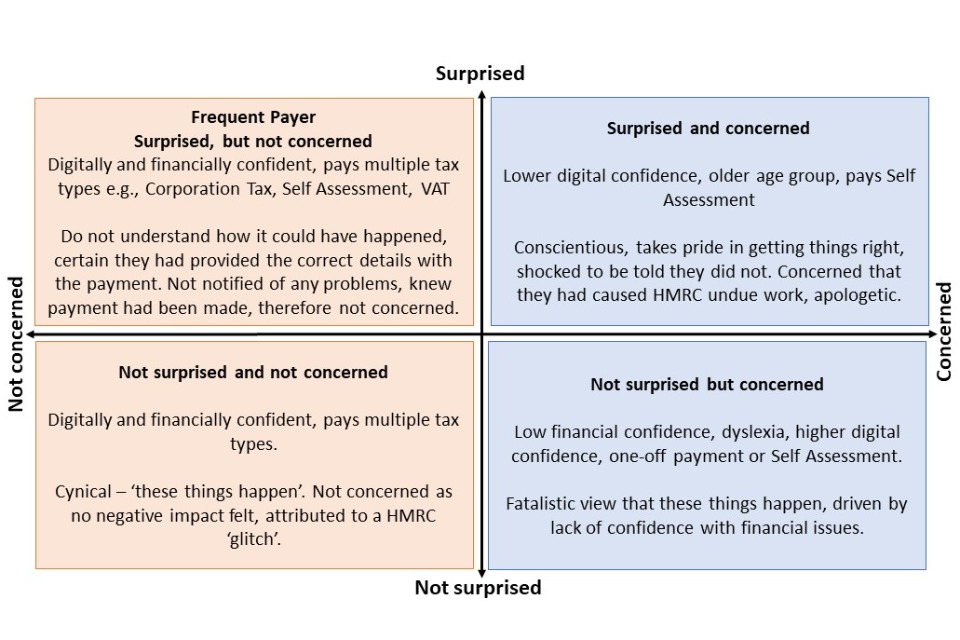

Among customers who were not already aware, their reaction when told by the interviewer that their payment to HMRC had been manually allocated varied by customer group, as shown in Figure 3.1.

Figure 3.1: Level of concern and surprise by customer group

While infrequent payers were concerned and actively wanted to get it right, frequent payers were generally not concerned about what had happened, and, although they wanted to check they had provided the correct reference number in future, saw it primarily as a problem for HMRC to resolve.

Depicted in the top right-hand box of Figure 3.1, Infrequent payers who had lower digital confidence (who were more commonly in the older age groups and tended to pay one-off or annual HMRC payments such as for their Self Assessment), tended to be conscientious, and took pride in getting their tax affairs correct. They were therefore shocked to be told that they had not included the correct details when making a payment to HMRC. This group were generally apologetic about the extra work they had caused for HMRC in making manual allocations. They were also concerned for themselves, as they worried that HMRC might not have recognised the payment was made by them.

“If I had known I would have been apologetic, and worried about the payment getting lost. These are large amounts of money” (Infrequent payer, male, Self Assessment)

Another group of infrequent payers (shown in the bottom right quadrant of Figure 3.1) with high digital confidence, but low financial confidence were generally less surprised to learn that they had made an error when making a payment. This was typically due to having experience of making errors in their tax or other financial affairs, as they found it challenging dealing with forms and numbers. They were nevertheless still concerned to hear that their payment to HMRC had been manually allocated. Their concern was primarily around the impact on themselves rather than HMRC, that is, the risk that their payment could have been lost and they could have faced penalty charges as a result.

“I wouldn’t be surprised to be honest (because things like this have happened before) but there’ll be a chance somebody will follow up… I don’t want to get in trouble.” (Infrequent payer, female)

In contrast, frequent payers (shown on the left-hand quadrants of Figure 3.1) were, overall, not concerned to learn that their payment had been manually allocated. This lack of concern stemmed from the fact that they had not felt any negative consequence; their payment had been allocated (albeit manually), and they had not been notified of any problem by HMRC. There was variation in the level of surprise within this group of frequent payers according to whether the customer had any previous negative experience with HMRC, such as debt. Frequent payers who had no negative experience of tax issues or HMRC were surprised to learn about the manual allocation of their payment. They could not understand how it could have happened, as they were certain that they had provided the correct details with their payment. In contrast, the frequent payers who had a previous negative experience of HMRC or of HMRC debt (depicted in the bottom left-hand quadrant of Figure 3.1) were more cynical and took the fatalistic attitude that these things can happen with a large organisation such as HMRC which deals with a high volume of payments. They did not express any sense of personal culpability for the manual allocation having occurred, and instead attributed it to a glitch in HMRC’s system, which was for HMRC to resolve.

“Dealing with every tax payment for the country? I’m sure a couple of payments are going to get messed up” (Frequent payer, male, sole trader, BACS)

“It is a concern for them, but they should try and make it easier for people to make payments” (Frequent payer, female, limited company, BACS)

4.3 Cause of manual allocation

When asked why they thought their payment had been manually allocated, customers attributed it to a range of behavioural barriers including heuristics/mental shortcuts, a lack of knowledge or experience, and a lack of capability. Heuristics included assumptions that they had made a careless mistake when manually entering the reference number on their online banking web page to make the payment. Customers explained that it was easy to forget to update the reference number when the reference of a previous payment was saved and auto filled by their online banking website in the payment details.

“I probably haven’t updated from the last time I made the payment. I’ve just done it and I’ve not renewed the reference” (Infrequent payer, female, Self Assessment, BACS)

Other causes suggested by customers included that they had been unaware of the reference number that they had to provide. They speculated that this was because, as far as they were aware, they had not been provided with one by HMRC. These consisted of customers who believed they had not received communication from HMRC. Customers paying a tax for the first time thought they had perhaps not realised that they needed to provide a reference number at the time of their first payment, although they had since learnt of the need to do so for subsequent payments. Another proposed cause was difficulty manually copying what was perceived to be a long and complex reference number with accuracy. Customers who had dyslexia or found form-filling difficult, and those with physical barriers such as unsteady hands caused by health issues, attributed the error to that type of cause.

” I put the wrong month in the reference number. I’m dyslexic so going on to the website is stressful” (Frequent payer, male, limited company)

5. Research findings – future behaviour

5.1 Future behaviour

At this point during the interview, customers were made aware (if they were not already) that their payment had been manually allocated. Based on this knowledge, all participants planned to change their future behaviour, including those who had not been concerned to learn that a payment had been manually allocated. Despite their lack of concern, frequent payers did want to ensure that this did not happen with any future payments they made, to ensure that payments were made promptly.

Customers’ plans to change their future payment behaviour centred around being more careful to check that they had provided the correct reference number. This was also the behavioural change that had already been made by those who were aware that their payment had been manually allocated before the interview. Across both customer groups, there was no spontaneous suggestion of any other changes (such as switching to authenticated digital payment methods) that they could make to reduce the risk of manual allocation.

When asked how HMRC could encourage customers to provide the correct payment information, customers’ ideas centred around communications about the reference number to be included with payment details. The main ways they felt they could be encouraged to change their behaviour was by understanding the importance of providing a correct reference number, the reference number being simpler and in a more intuitive format and provided in a digital format (rather than via a letter).

“Tell us what you need to do…step by step, if you’re paying by bank transfer, then ensure that you put any reference number at the top of the letter [HMRC send]” (Infrequent payer, female, Self Assessment)

A simpler reference number in a more intuitive format was preferred. Suggestions included that the reference number could incorporate a customer’s Unique Tax Reference (UTR), company registration number, rather than a long string of randomised numbers and letters, the reference number was expected to be easier to correctly copy and enter manually.

A reference number provided in a digital format, via email, text message, on the Personal or Business Tax Account, and via tax agents and software was considered easier to copy into online banking details than from a letter and present less risk of error.

5.2 Notification of manual allocation

During the interviews, participants were informed of the authenticated digital payment methods available to make payments to HMRC, such as paying via their Personal Tax Account or Business Tax Account or the HMRC app, and their benefits, that is, that HMRC can check that the reference number provided is valid before payment is made. Customers identified both incentives and barriers to switching to these payment methods.

Key incentives to switching to authenticated digital payment methods included reassurance of the HMRC auto-checks, and easier, more convenient payment methods of the Personal Tax Account or Business Tax Account or HMRC app, compared with online banking.

Both frequent and infrequent payers expected HMRC auto-checks to provide reassurance and confidence that their payment had been received correctly by HMRC. This was particularly motivating for the group of Infrequent Payers who had low financial confidence but higher digital confidence.

Frequent payers expected it to be easier to pay by providing card details on their Personal Tax Account or Business Tax Account or via the HMRC app, rather than having to ensure they selected the correct HMRC account and provided the correct reference details on their online banking site. For frequent payers who were not previously aware of the HMRC app, it was expected to be more convenient and straightforward to use than logging into their Personal Tax Account or Business Tax Account. Other benefits of paying via an app were expected to include easy access to their HMRC accounts when customers were travelling abroad and needed to make a payment.

Barriers to switching to authenticated digital payment methods centred around a perception that switching would be too much hassle for not enough reward. They included a high level of trust and comfort in existing payment methods, a reluctance to use the app, and a perceived lack of capability of the Personal Tax Account or Business Tax Account to enable certain types of payment to be made, namely standing orders and Corporation Tax.

The group of infrequent payers who had lower digital confidence wanted to continue paying through their online banking because they used this payment method regularly for non-HMRC payments and found that it worked well for them. Their level of trust in and comfort with their online banking payment method was high, and they did not want to change their habits for payments to HMRC that were typically a one-off or annual payment only.

“If it ain’t broke, don’t fix it. I don’t like change for change’s sake” (Infrequent payer, male, Self Assessment)

Moreover, there was a view among frequent payers that online banking was quicker and more streamlined to access and use to make payments, compared to their HMRC accounts. The latter were perceived to require more steps to log in, such as the verification process, and then once logged in, were considered more challenging to navigate to the correct webpage than the online banking website.

“If you were to go on the desktop and go to gov.uk, you would have to go through all the payment types first. You know, I’ve had experience where it’s gone, ‘right okay, click on this’ and then it will ask you questions maybe about the tax that you’re paying, and you will click on something, and it will take you somewhere else, so you think ‘hang on a minute’. You trust your bank; you trust the system. That’s what you know, that’s what you trust” (Frequent payer, female, limited company)

Online banking provided a record that a payment had been made, which provided reassurance to the customer that they could evidence the payment being made if it was ever called in to question. Customers therefore felt that even if there was no evidence of it being allocated by HMRC, they could always prove by referring to their online banking records that they had carried out their responsibility of making the payment.

Both infrequent and frequent payers perceived there to be barriers to using the HMRC app. Infrequent payers with low digital confidence thought it would be too much hassle to download and familiarise themselves with ‘another’ app that they would only use infrequently. Some frequent payers expressed a preference for dealing with important and serious matters such as tax on a computer screen rather than on their phone. In addition, there was a perception among some frequent payers that their online banking app was easier to use to make payments than the HMRC app would be. For example, those with multiple businesses found it straightforward and easy to navigate to the relevant business on their banking app, and did not expect it to be as easy to do the same on the HMRC app.

As much as some customers wanted to pay using their HMRC accounts, there was a perception that the Personal and Business Tax Account currently do not have the functionality to enable customers to pay certain types of tax. This included the misbelief that they could not pay Corporation Tax on the Business Tax Account or set up a standing order on the HMRC accounts to make regular payments. This demonstrates low customer awareness of the services that HMRC currently offers as it is possible to pay Corporation Tax and set up variable direct debits and budget payment plans via the Personal or Business Tax Account. These customers were therefore eager to continue paying via their online banking because they thought it was the most ‘digital’ payment method available for these types of payment.

5.3 Customer suggestions

To encourage customers to use the authenticated digital payment methods, customers suggested that HMRC should issue communications on them.

HMRC communications were suggested to raise customer awareness of these authenticated digital payment methods and their benefits compared with other methods of payment. It was suggested that communications should include reassurance that these authenticated digital methods are easy and simple to switch to and use, with details of online support that is available. In addition, customers recommended that HMRC notified individuals when their payment has to be manually allocated, to highlight the relevance and value of using authenticated digital payment methods.

“Tell me to use [these authenticated digital payment methods]. There’s absolutely nothing at all stopping me using it…Probably just as simple as sending out an email to say that this is a lot better and a lot safer and a lot easier for me because I’ve never really thought about whether it might be better than what I’m doing.” (Frequent payer, female, limited company)

The other recommendation emerged from the misbelief that HMRC’s digital payment channels have limited functionality. Customers wanted to be able to use their Personal Tax Account or Business Tax Account to make all types of payment but believed that they were unable to make Corporation Tax payments on their Business Tax Account or set up regular payments. Further communications on the functionality of HMRC accounts would address these misconceptions.