National space strategy: technical annex

Updated 1 February 2022

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/publications/national-space-strategy/national-space-strategy-technical-annex

Purpose of this document

This document presents an overview of a Space Sector Market Model. This model was developed by Bain & Company on behalf of BEIS in April 2021. The model informed the development of the National Space Strategy.

Explanation of the Market Model

The Market Model was intended to bring together the best data from third party forecasts of growth in the global space sector, in order to identify high growth markets, and to set the foundation for assessing opportunities for the UK space sector.

Definition of the space sector

There is not a standardised global definition of the space sector. However, the OECD, the European Space Agency, and many national space agencies consider the space sector to cover the entire spacecraft value chain, from initial R&D to manufacture, launch, operation, and finally the processing and application of satellite data and signals in consumer products and services.

The Market Model only includes forecasts that fall within scope of this definition of the space sector.

Model methodology

Step 1: Define the value chain and corresponding market segments

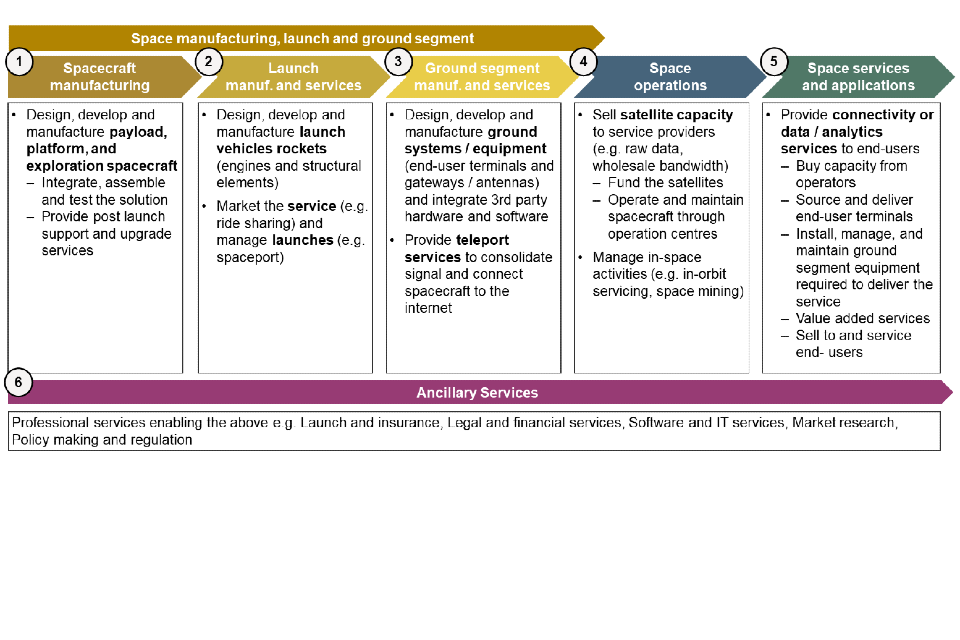

In order to be able to compile and compare third party estimates, the model defines six segments in the space sector value chain. The diagram below shows the value chain definition, with descriptors for each segment.

Figure 1: Definition of the space sector value chain

-

Spacecraft manufacturing

Design, develop and manufacture payload, platform, and exploration craft:

- integrate, assemble and test the solution

- provide post launch support and upgrade services -

Launch manufacturing and services

Design, develop and manufacture launch vehicles rockets (engines and structural elements).

Market the service (for example ride sharing) and manage launches (for example spaceport). -

Ground segment manufacturing and services

Design, develop and manufacture ground systems / equipment (end-user terminals and gateways / antennas) and integrate 3rd party hardware and software.

Provide teleport services to consolidate signal and connect spacecraft to the internet. -

Space operations

Sell satellite capacity to service providers (for example, raw data, wholesale bandwidth):

- fund the satellites

- operate and maintain spacecraft through operation centres

Manage in-space activities (for example, in-orbit servicing, space mining). -

Space services and applications

Provide connectivity or data / analytics services to end-users:

- buy capacity from operators

- source and deliver end-user terminals

- install, manage and maintain ground segment equipment required to deliver the service

- value added services

- sell to and service end-users -

Ancillary services

Professional services enabling the above, for example:

- launch and insurance

- legal and financial services

- software and IT services

- market research

- policy making and regulation

Step 2: Compiling market segment estimates to derive the size of the global space sector in 2019

The Market Model makes use of third party estimates of the US dollar value of the income of different market segments, selected on the basis of which estimate provides the most accurate, granular, and complete picture of that market segment. These estimates are mapped back to the value chain segment definition to avoid any double counting.

Step 3: Compiling market segment forecasts to estimate the size of the global space sector in 2030

Using a similar methodology to Step 2, the Market Model makes use of third party forecasts of the US dollar value of the income of different market segments, selected on the basis of which forecast provides the most accurate, granular, and complete picture of that market segment.

The chart below shows the different sources used to estimate the market segments for 2019 and 2019 to 2030.

Figure 2: The Composition of market segment estimates and forecasts

| Segment | Description | Source (19) | Source (19-30) |

|---|---|---|---|

| Other government spending | Scientific research funded by government grants | Euroconsult/Bryce | - |

| Applications & services - Earth Observation | Provide connectivity or data / analytics services to end-users | NSR | NSR / Eurconsult |

| Applications & services - Navigation | GSA | GSA | |

| Applications & services - Other comms (radio, broadband, managed services) | Bryce | Morgan Stanley | |

| Applications & services - Television | Sell satellite television packages to consumers | Bryce | S&P |

| Operations | Sell satellite capacity to service providers | NSR | NSR/Euroconsult |

| Ground manufacturing & services - comms, User terminal & network equipment | Design, develop and manufacture ground systems / equipment | NSR | NSR |

| Ground manufacturing & services - GNSS user terminal | Design, develop and manufacture GNSS chipsets | GSA | GSA |

| Launch manufacturing & services | Design, develop and manufacture launch vehicles rockets (engines + structural ekements) | Euroconsult | Euroconsult |

| Spacecraft manufacturing | Design, develop and manufacture payload + platform + exploration spacecraft | Euroconsult | Euroconsult |

Step 4: Extrapolation to 2030

Where third party estimates do not extend to 2030, growth is extrapolated to 2030 at the rate of growth between 2025 and the final year of estimates available. For example, if the last year of data is 2028, then growth in 2029 and 2030 is forecasted to be the same as the annualised growth rate between 2025 and 2028.

Step 5: Conversion from US dollars into pounds sterling

Currency conversion is not formally part of the Market Model, but BEIS converted the US dollar value estimates into pound sterling using annual average spot exchange rate published by the Bank of England[footnote 1]. In 2019 (the base year of the model), $1 was equal to £0.78. The 2020 value was used to convert currency in years 2020 up to 2030.

Results of the Model

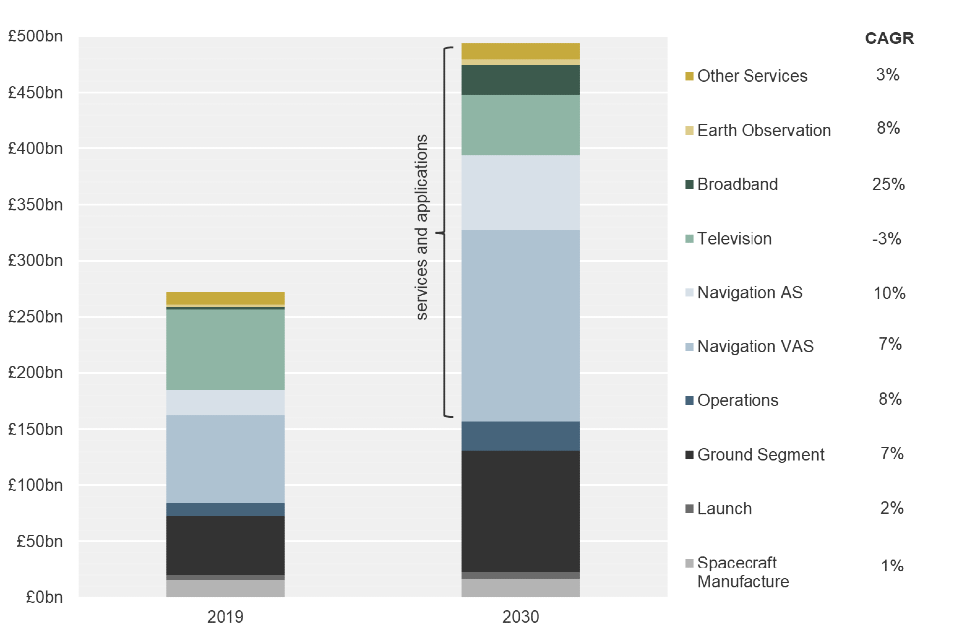

In aggregate terms, the Market Model estimates the size of global space sector to be around $350bn (£270bn) in 2019. The global space sector is forecast to grow up to around $630bn (£490bn) in 2030. This equates to growth of around 80% over 11 years, or alternatively a compound annualised growth rate of 5.6%.

Within the space sector, some segments are forecast to grow significantly faster than others, with annualised growth rates ranging from 1% for spacecraft manufacturing to 25% for broadband.

The chart below shows the estimated size of different market segments in 2019 and their forecast values in 2030, along with compound annualised growth rates (CAGR).

Figure 3: The size and growth of the global space sector

Source: BEIS Space Market Model

Notes: CAGR = compound annualised growth rate. Navigation AS = Navigation Augmented Services. Navigation VAS = Navigation Value Added Services.

Data sources

A number of data sources were used to create this model. The list below contains references to all freely available data sources used in the Market Model; some commercial sources of data, which are not cited, were also used:

- GNSS Market Report, Issue 5, copyright © European GNSS Agency, 2017

- GNSS Market Report, Issue 6, copyright © European GNSS Agency, 2019

- Morgan Stanley, ‘Space: Investing in the Final Frontier’, July 2020

- Euroconsult, ‘Satellite communications market to reach $19.4B by 2028’, Sept 2019

- Euroconsult, ‘Space Economy Report’ (Free Extract), 2020