Government response to local audit framework: technical consultation

Updated 31 May 2022

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3 or write to the Information Policy Team, The National Archives, Kew, London TW9 4DU, or email: psi@nationalarchives.gov.uk.

Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned.

This publication is available at https://www.gov.uk/government/consultations/local-audit-framework-technical-consultation/outcome/government-response-to-local-audit-framework-technical-consultation

Ministerial foreword

I would challenge anyone to find another time in our nation’s history when local government has mattered as much as it does today.

Over the last 2 years, councils have acted as a lifeline to our communities, at the forefront of shielding the most vulnerable while supporting residents and businesses through the pandemic.

In times of such challenge, public confidence in our systems of local democracy becomes ever more vital. A robust system of local audit is a key part of that. Through assuring probity, transparency and accountability, local audit keeps the wheels of local government turning.

Today’s publication marks the culmination of the government’s response to Sir Tony Redmond’s Independent review into the effectiveness of external audit and transparency of financial reporting in local authorities and celebrates the first steps already taken towards a more coordinated local audit system, in which key players work together to address challenges as they arise.

The 2014 Local Audit and Accountability Act created a locally-led audit framework, giving councils the power to appoint their own auditors while also delivering a significant saving to the public purse.

Despite these lasting advantages, in recent years the local audit system has faced growing issues of timeliness and wider market instability. These really matter, as late completion of local audits impedes citizens’ rights to transparency, and as local councils face financial pressure, it is essential that good financial reporting and the audit process are used to make any risks clear in good time.

For these reasons, in 2019 the government commissioned Sir Tony Redmond to conduct an independent review of the local audit framework. I remain wholly committed to the principles of the 2014 Act, so am delighted that we can now fulfil Sir Tony’s key recommendation that a ‘system leader’ should be appointed to ensure a coherent response to challenges that arise – with the support of a vast majority of those who responded to our public consultation.

Today’s government response confirms that the new regulator, the Audit Reporting and Governance Authority (ARGA) will act as system leader for local audit. Ahead of ARGA’s establishment, shadow arrangements will start at the Financial Reporting Council. In the coming months Neil Harris, currently a Key Audit Partner at EY with over 20 years’ experience of local audit, will join FRC as the first director of local audit, leading a local audit dedicated unit.

We have not stood still in the meantime. In spring 2021, we announced measures to ease immediate timeliness issues and reduce the financial burden which increased audit requirements had placed on hard pressed councils.

Since then, collaboration has accelerated across the current system as key players have worked closely through the Liaison Committee chaired by my department to deliver a package of measures to improve timeliness published in December 2021.

Furthermore, we have committed to provide councils with £45 million additional funding over the course of the next Spending Review period to support with the costs of strengthening their financial reporting and increased auditing requirements.

Finally, the Levelling Up Bill has fired the starting gun on the biggest shift in power from Whitehall in modern times, with local leaders newly empowered to direct funding towards their own, locally identified priorities. We must ensure that all elements of local accountability keep pace with this great change, both for citizens and local bodies themselves. So, this government response also confirms that once parliamentary time allows, we plan to make Audit Committees mandatory for all councils, with at least one independent member nominated to each audit committee.

Our mission to spread opportunity and prosperity to all parts of the country starts at the local level. Taken together, the reforms to local audit we are announcing today will further enhance and build on public trust in our dedicated public servants through improved transparency and accountability for the communities they serve.

Kemi Badenoch MP

Minister for Local Government, Faith and Communities

1. Introduction and purpose of the consultation

The independent audit of a local authority’s statutory accounts and arrangements for achieving value for money is a key transparency and accountability mechanism which is fundamental to sustaining public confidence in our systems of local democracy. Local audit enables taxpayers, and local bodies themselves, to have confidence that financial accounts are true and fair and that the authority has been acting with propriety and has arrangements in place to secure value for money through the economic, efficient and effective use of its resources.

Sir Tony Redmond’s Independent review into the oversight of local audit and the transparency of local authority financial reporting reported in September 2020 that there was a lack of coherence and join up across the current local audit framework, as none of the organisations in the system “had a statutory responsibility, either to act as a systems leader or to make sure that the framework operates in a joined-up and coherent manner”, which was contributing to wider issues including audit delays and market instability.

Local Audit Framework: technical consultation (July 2021) set out the government’s intention to establish the Audit Reporting and Governance Authority (ARGA), which will be established to replace the Financial Reporting Council (FRC), as the new system leader for local audit. It also set out proposals to implement other recommendations from the Redmond Review: to strengthen audit committees, improve capacity and capability and a number of measures relating to smaller bodies.

The consultation sought views on how these arrangements would work and received 57 responses from a range of local bodies, audit firms, partner organisations, and other stakeholders. The government is grateful for the time and effort that has gone into these responses, and the suggestions made.

This consultation response sets out how the government plans to act in the light of comments received, confirming its intention to establish ARGA as the system leader for local audit and for shadow arrangements to be established at the FRC ahead of that. It should be read in conjunction with the government’s response to its White Paper Restoring trust in audit and corporate governance, which confirms its broader plans for reforming audit and corporate governance and establishing ARGA.

The consultation response also confirms that when parliamentary time allows, we plan to make audit committees compulsory for all councils, with at least one independent member appointed to each audit committee. It sets out wider developments since the consultation was published, including activities undertaken by the Department for Levelling Up, Housing and Communities (DLUHC) and local audit partners as part of the Liaison Committee and the interim system leader arrangements.

This document does not set out a response to those consultation proposals related to smaller bodies. The government has reviewed the comments it has received and has concluded that more time is required to consider these proposals in the context of broader work underway to progress the commitments in the Levelling Up White Paper. The government will therefore provide a response to the proposals relating to smaller bodies in due course.

2. Interim system leadership

Local Audit Framework: technical consultation set out the government’s intention to act as interim system leader for local audit before new system leader arrangements were established.

This has included the establishment of the new Liaison Committee, which has met 4 times – on 29 July, 21 September, 13 December, and 19 May. The minutes of Liaison Committee meetings are made available online at: Local Audit Liaison Committee.

This forum has enabled strong and positive engagement from across the local audit system on how to balance different priorities and objectives. A primary focus for the Liaison Committee across this period has been the development of measures to address ongoing audit delays and to support the fragile audit market.

Through this work a cross-sector package of additional measures was agreed by government and other key stakeholders to support improved timeliness and the wider local audit market. This was published in December 2021: Measures to improve local audit delays. An update on progress (PDF, 123KB) against these measures and other work underway on local audit was recently provided to the Liaison Committee by the department.

In addition, Public Sector Audit Appointments Ltd (PSAA) has continued to progress its procurement strategy for the next round of local audit contracts. In March, PSAA confirmed that 470 out of 475 (99%) eligible local bodies had opted-in to its scheme for the procurement of the 23/24-27/28 audit contracts. In addition, following good feedback from audit firms at the Selection Questionnaire stage, PSAA issued the Invitation to Tender in April. Audit firms have until 11 July to submit bids for the local audit contracts.

The government is also continuing wider work to prepare for the establishment of ARGA, including the publication of the government response to the White Paper Restoring trust in audit and corporate governance.

The FRC has recently confirmed the appointment of its first director of local audit. Neil Harris, a Key Audit Partner at EY with 20 years of local audit experience will join FRC in the coming months to lead a new dedicated local audit unit which will be integral to shaping the FRC’s new system leadership role and working with wider partners.

As the new shadow unit is established and builds capacity, the FRC will start to take on a greater system leadership role. This will include a period of transition during which the new FRC director of local audit will jointly chair the Liaison Committee with DLUHC as interim system leader. As part of its commitment to establish strong networks, FRC plans to start early engagement with key stakeholders across the summer.

Once the outcome of the upcoming procurement of local audit contracts is confirmed, it will also work with the market on the development of a new workforce strategy.

These arrangements will be formalised through a high-level Memorandum of Understanding covering the proposed remit of the new shadow arrangements to be published later in 2022, ahead of future statutory governance arrangements. The specifics of these future arrangements are outlined in more detail in this consultation response.

3. System leadership

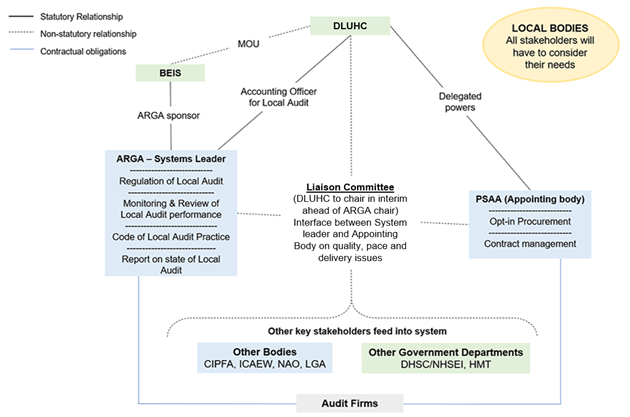

Section 5 of the consultation set out our proposals to simplify the existing local audit framework and create a new ‘system leader’ for local audit.

DLUHC remains committed to the principles of the 2014 Local Audit and Accountability Act, which abolished the Audit Commission and created a locally-led audit regime in which local bodies have the right to appoint their own auditors. This reduced the costs of local audit to local authorities and government considerably.

We accepted Sir Tony’s finding that a system leader was needed for the local audit framework; accordingly our Spring Report announced our intention that the Audit Reporting and Governance Authority (ARGA) being established to replace the Financial Reporting Council (FRC) should assume that role.

Figure 1: New Local Audit Framework

System leadership is a term used to describe how individuals and organisations can work across traditional organisational boundaries to ensure a more joined-up approach. Paragraphs 25-29 of the consultation set out that the functions within the existing local audit framework are currently delivered by 5 separate bodies.

These organisations have sought to engage proactively to resolve emerging issues, yet each is bound by its own organisational objectives which can fail to ‘join up’ or may even conflict.

We set out our view that a system leader was needed to:

- Assume responsibility for ensuring coordination across different parties and for responding to strategic priorities.

- Identify risks and issues as they emerge, with the power to act on these, or oversee action by others, as well as considering potential trade-offs in the round.

We proposed that the system leader should have statutory responsibilities and powers to ensure they can function appropriately.

Question 1: Do you agree with the proposed functions which the system leader for local audit needs to enable a joined-up response to challenges and emerging priorities across local audit? Please let us know any comments you have on the proposal.

Summary of responses

Three quarters of respondents either agreed or partially agreed with the proposed functions. Respondents commented that a system leader should both identify issues of concern within the local audit framework and lead work to tackle those. There was support for the system leader to have statutory responsibilities and powers; some respondents proposed that the system leader should have scope to address issues within audited bodies, as these also form part of the system. Respondents also commented that national guidance from a system leader would be welcome in cases of recurring differences (between auditors and audited bodies, for example) which are currently being left for resolution at a local level. There was also a view that the system leader should act as an advocate for the local audit system.

Government response

The government welcomes respondents’ support for the creation of a system leader for local audit, the functions we have proposed for the system leader and for these to be underpinned by statutory responsibilities and powers as appropriate. The Government agrees that a systemic approach to challenges facing the local audit system needs to reflect audited bodies’ role in the system, so the system leader will need to continue local networks, for example and have a strong understanding of the needs of local bodies.

We agree that the system leader should work with organisations and sector representatives to resolve or issue direction on issues facing the local audit system, as well as working as a broader advocate. We will consider further the case for the specific statutory powers the system leader needs as we develop legislation, and outline them in the future draft bill, but currently we do not propose for the system leader to have powers over individual audited bodies.

ARGA’s responsibilities and functions as system leader

Paragraphs 30-41 set out that as system leader ARGA will have overarching responsibility for the local audit quality framework. The FRC already has specific delegated responsibility for the oversight and monitoring for audits of significant local public bodies and the regulation of auditors of local public bodies by Registered Supervisory Bodies; these will continue.

In addition, ARGA will take over statutory responsibility for preparing and issuing the Code of Audit Practice and associated guidance notes from the National Audit Office (NAO). In support of its statutory code setting function, NAO conducts a wide range of activities. We invited views on whether these activities should continue.

As primary legislation is needed to transfer the Code to a different organisation, this would remain with the NAO until legislation was brought forward to establish ARGA. The consultation also set out the intention for the new system leader to conduct a full post-implementation review of the new value for money narrative requirement introduced in the 2020 Code. This would assess whether it has led to more effective external audit consideration of financial resilience and value for money matters to help inform development of the next Code. The FRC will work closely with NAO in the interim period before formal transfer of responsibility by legislation.

We also confirmed that procurement and contract management functions would continue to be delivered by a separate Appointing Body.

Question 2: Do you have any comments on the proposed functions that the Audit, Reporting and Governance Authority (ARGA) should have alongside its new system leader responsibilities?

Question 3: Do you agree that the system leader should conduct a full post implementation review to assess whether changes to the Code of Audit Practice have led to more effective external audit consideration of financial resilience and value for money matters 2 years after its introduction, with an immediate technical review to be conducted by the National Audit Office (NAO)? Please let us know any comments you have on the proposal.

Question 6: Do you agree that the responsibilities set out above will enable the Audit, Reporting and Governance Authority (ARGA) to act as an effective system leader for local audit? Are there any other functions you think the system leader for local audit should have?

Summary of responses

Three quarters of respondents agreed or partially agreed that the responsibilities set out for ARGA would enable it to act as an effective system leader.

Respondents expressed a range of views on the specific functions ARGA should have alongside its system leader responsibilities. Some said that FRC’s existing quality oversight role could make this the ‘dominant function’ of the new system leader, while a concern was raised that any uncertainty over the Code could deter market entry. There were also a number of views that the system leader should issue guidance and direction to auditors and work with CIPFA to reconcile existing sets of guidance.

There was very strong support for the activities which the National Audit Office currently conducts in support of the Code of Audit Practice to continue.

Over three quarters of those who answered agreed or partially agreed there should be a post-implementation review of the Code. Some respondents said it should be conducted by the NAO given its current role. There were suggestions it should focus on whether the VfM judgement is properly understood, and consider how financial resilience is assessed, as well as how it impacts on behaviour. It was suggested the review should consider wider learning, and consult other organisations, with consideration given to how data could be shared.

A number of respondents felt the review should be delayed, particularly as ongoing timeliness issues have limited the sample of completed VfM reports, while additional COVID-19 funding made the period unrepresentative. Respondents further cautioned that the timing of the review should not create uncertainty around the Code ahead of the next procurement.

Government response

We welcome the wide range of views expressed on proposed functions and respondents’ strong support of responsibilities which ARGA will have as system leader. We do not agree there is a risk of a single function ‘dominating’ the system leader; indeed, one of our reasons for choosing ARGA as system leader for local audit has been that it is the only organisation in the current system which already conducts all the functions we think a system needs to have – these include code-setting.

We note the value which stakeholders across the system place on the activities currently conducted by the NAO in support of its code setting function (including responses to public enquiries raised under the 2014 Act). The NAO has confirmed its intention to continue these activities while it remains responsible for code-setting.

The government can confirm that these activities will also be continued once the Code has transferred to ARGA. Some of these activities – such as the Local Auditors Advisory Group and technical networks – would be undertaken directly as part of ARGA’s code setting role, or potentially included in practice note 10.

Some other activities – for example, those which involve providing advice and assurance on specific audits which are then reviewed by ARGA – would not be undertaken by ARGA directly. The exact method of delivery for these activities will be considered as part of establishing the new shadow arrangements.

The government welcomes support for a full post-implementation review of the new VfM arrangements. The Code is a key part of the local audit system, and it is important to ensure that it helps to facilitate effective local audit.

To provide certainty ahead of the next procurement, the government has confirmed the agreement with the NAO and FRC to re-lay the current code so that it will apply until the end of the 2027/28 audit year.

On balance, taking account of the views of respondents, the government agrees that a slightly longer timeframe for the review may be appropriate, both to allow the new arrangements time to bed in and to ensure a sufficient sample size. Consequently, the overnment has provisionally agreed with the FRC and NAO that this should be completed within 3 years, building on the ongoing work being undertaken by the NAO. To reflect the expectation of a period of transition, our expectation is that the wider review will be undertaken with input from both the FRC and NAO, to confirm details in due course.

Expertise and focus

Paragraphs 42 and 43 of the consultation set out our proposal that a dedicated local audit unit should be set up within ARGA to ensure that the new regulator will have sufficient focus and expertise when it becomes system leader for local audit. The intention that the new unit would establish effective engagement networks with local bodies and audit firms was also set out.

Question 4: Do you agree with the proposals to ensure that the Audit, Reporting and Governance Authority (ARGA) has sufficient expertise and focus on local audit? Please let us know any comments you have on the proposals.

Summary of responses

There was strong support for this proposal. Respondents stressed that the dedicated unit would need sufficient prominence and profile within the new regulator to be effective. There was support for including staff from both audited bodies and auditors, although some concern that this could aggravate existing audit supply issues. There was widespread agreement that active engagement with auditors and local bodies are vital to the healthy functioning of the local audit system, so networks should be maintained and strengthened.

Government response

The government welcomes the support for the development of a dedicated local audit unit within ARGA. The FRC has recently announced the appointment of its new director of local audit, and work is underway to establish the new unit in shadow form.

While recognising concerns about audit capacity, it is critical that the new regulator is furnished with the right expertise from the outset. The government agrees that effective networks will be important to the effective functioning of this system. The government will be working with the FRC to establish these in shadow form from May 2022, to ensure that local bodies and audit firms are involved in the development of the system leader function. Over time this will include taking on responsibility for the current Local Audit Advisory Group; the system leader will want to establish their own strong networks with the various stakeholder groups.

Liaison Committee

Paragraphs 45 and 46 of the consultation set out our proposals for a new Liaison Committee of senior stakeholders, to be the key forum for ensuring coordination across different parties and acting on risks and issues as they emerge. The consultation set out the intention that the Liaison Committee would meet quarterly and be chaired by the DLUHC as part of interim arrangements ahead of the ARGA’s establishment as system leader for local audit.

Question 5: Do you agree with the proposed role and scope of the Liaison Committee? Please let us know any comments you have on the proposal.

Summary of responses

Two thirds of respondents agreed or partially agreed with this proposal. Several respondents commented on the Liaison Committee’s proposed membership, proposing direct local government and audit firm representation. There were also comments on the need to set out clear structures, including the relationship with the Local Audit Monitoring Board (LAMB) and the importance of sub-groups and objectives to ensure actions can be progressed, and wider networks could feed in. There were also comments that it was important that the Liaison Committee had sufficient authority to drive forward work on resolving differences, given potentially conflicting objectives.

Government response

The government welcomes the positive response to our proposals for the Liaison Committee.

As set out in the interim system leadership section above, in July 2021 DLUHC established the Liaison Committee as part of its interim system leader role. The positive actions undertaken by the Committee members to date have helped to agree a more collaborative and coordinated response to ongoing timeliness issues, as well as actions to support the procurement for the next appointing period.

As the new local audit shadow unit is established and builds capacity, the FRC will start to assume a greater system leader role. This will include a period of transition during which the FRC will jointly chair the Liaison Committee with the DLUHC. We will work closely with the FRC to fully develop the Liaison Committee during this period, including formalising its structures and membership.

Statutory local audit objective and regulatory principle

The White Paper Restoring Trust in Corporate Reporting and Governance set out the Government’s intention to establish ARGA on a statutory basis. Paragraphs 47-54 of the consultation set out how the new regulator’s role as system leader for local audit will be reflected in its proposed overarching statutory objectives and in the regulatory principles to which it will be required to have regard.

The White Paper set out 3 overarching statutory objectives for ARGA, while our consultation set out a further statutory objective for local audit:

General objective: To protect and promote the interests of investors, other users of corporate reporting and the wider public interest.

Quality objective: To promote high quality audit, corporate reporting, corporate governance, accounting and actuarial work.

Competition objective: To promote effective competition in the market for statutory audit work.

System leader for local audit objective: to ensure the local audit system operates effectively.

The White Paper further proposed that ARGA will be required to have regard to a series of regulatory principles. In order to reflect the specific requirements of the local audit, the consultation proposed that ARGA should also have a responsibility for the value for money arrangements in local audit: For local audit, also having regard to the requirement of the Local Audit and Accountability Act 2014 that an audit of a relevant authority (referred to in the Act as ‘local audit’) includes a value for money arrangements commentary.

Question 7: What is your view on the proposed statutory objective for the Audit, Reporting and Governance Authority (ARGA) to act as system leader for local audit? Please include any comments on the proposed wording.

Question 8: Do you agree with the proposal that the Audit, Reporting and Governance Authority (ARGA) will have a responsibility to give regard to the value for money considerations set out in the Local Audit and Accountability Act 2014? Please include any comments on the proposed wording.

Summary of responses

Overall, respondents welcomed the proposal that ARGA’s system leader role should be reflected in its overarching objectives. A number of respondents commented that the proposed system leader objective should define what is meant by ‘effectively’, including references to timeliness, quality, or ensuring resilience. There were suggestions that it should specifically reference the 2014 Audit and Accountability Act; value for money; democracy and accountability; or ‘the public interest’.

There were numerous comments on ARGA’s other objectives, including support for the proposed competition objective, given concerns about the fragility of the local audit market. Some commented that local audit should have a separate quality objective, or that the other objectives should reference local audit or the interests of citizens or stakeholders, as well as investors.

There was strong support for the proposed regulatory principle that ARGA should give regard to the value for money considerations set out in the 2014 Audit and Accountability Act. Respondents’ comments mainly affirmed the importance of the value for money arrangements judgment element of local audit, although a few responses demonstrated some confusion over the purpose of judgement. The judgement considers whether an audited body has sufficient arrangements in place to judge whether the audited body delivered value for money; rather than whether the audited body has delivered value for money.

Government response

The government welcomes the support for the proposed system leader objective and regulatory principle and confirms the intention to take these forward, along with the other proposed objectives and principles which have been confirmed in the recently published government response to Restoring Public Trust in Audit and Corporate Governance where similar concerns are addressed in detail.

Some respondents expressed a wish for further detail in the objective, but we would note that this will be one of the new regulator’s overarching statutory objectives, which are deliberately high-level. Further detail on ‘how’ these objectives should be delivered will be set out through other mechanisms, such as the Remit Letter and Memorandum of Understanding; in developing these we will consider respondents’ views on what ‘effectiveness’ means.

We have also noted calls to add an additional system leader quality objective or amend ARGA’s other overarching objectives to reference local audit. As the system leadership objective will be one of only 4 overarching objectives the new regulator will have, we are satisfied this strikes a reasonable balance and confirms the high priority local audit will have within ARGA’s overall remit.

Governance of ARGA as system leader for local audit

Paragraphs 52-57 of the consultation set out our proposed governance and accountability arrangements for ARGA’s role, including that DLUHC would retain Accounting Officer responsibility for policy relating to local audit, and Memoranda of Understanding between respective Secretaries of State would set out departmental lines of accountability for ARGA’s role as system leader for local audit.

The consultation also proposed that DLUHC’s Secretary of State would send a discrete Remit Letter to ARGA related to its local audit role. This would mirror the Remit Letter from the Secretary of State for Business, Energy and Industrial Strategy (BEIS) related to ARGA’s wider statutory audit role, to which it would be required to formally respond and the response to be published. This would complement the regulator’s statutory objectives and seek to ensure that the regulator has regard to the Government’s overarching policy aims when carrying out its policy-making functions, without compromising its operational or regulatory independence.

Question 9: Do you agree that the proposals outlined above will provide an appropriate governance mechanism to ensure that the new system leader has appropriate regard to the government’s overarching policy aims without compromising its operational and regulatory independence? Please let us know any comments you have on the proposal.

Summary of responses

There was broad support for the proposed governance arrangements. Several responses commented that Memoranda of Understanding (MoUs) and Remit Letters should clearly reflect all associated government departments and local body priorities; there was also a question over how any departmental differences would be resolved.

There were suggestions the Remit Letter could undermine the system leader’s independence, and it should not seek to intervene in interactions with other organisations in the system. There were also comments on timing, with suggestions it should be annual. One response suggested that ARGA’s response to the Remit Letter could be used to challenge government strategy when the system leader considers it in the interest of local audit to do so.

Government response

The government welcomes the consultation response and confirms the intention for a discrete Remit Letter from DLUHC’s Secretary of State to ARGA at least once during the lifetime of each Parliament. This will cover the government’s priorities for local audit for all relevant bodies, meaning it will require close working among all interested departments, to ensure alignment across government.

While some respondents raised concerns about independence, in practice it is an important mechanism for ensuring clarity of strategic objectives and to reflect lines of Ministerial accountability, both on corporate reporting and local audit. The frequency of letters would be at least once a Parliament but could be more often if necessary.

As outlined earlier in the consultation response, the intention is that during the shadow arrangements before ARGA is established, strategic priorities will be included in a high-level Memorandum of Understanding which will be in place while the FRC is establishing its new unit ahead of taking on full responsibilities.

Other government departments also retain a responsibility where local audit relates to their bodies – for example, the Department of Health and Social Care (DHSC) with health audit – and it will be important to ensure that appropriate lines of accountability are agreed with DLUHC in recognition of this.

The Annual Report

Sir Tony Redmond recommended a responsibility for producing annual reports summarising the state of local audit. We strongly agreed with this recommendation as no entity currently has the responsibility to collate and report on the results of the work of the external auditors of local authorities and individual NHS bodies.

Paragraphs 58-62 set out the annual report which ARGA will be required to produce for Parliament on delivery against its objectives and proposed that ARGA’s statutory function as local audit system leader should form a distinct, standing element of ARGA’s annual reporting, potentially as a separate annex to the main annual report which ARGA produces.

Question 10: Do you agree that the Audit, Reporting and Governance Authority (ARGA) annual reporting should include detail both on the state of the local audit market, and the Audit, Reporting and Governance Authority’s (ARGA) related activities, but also summarising the results of audits? Please include any views on other things you think this should include.

Summary of responses

There was very strong support for this proposal. Suggestions for annual reporting included timeliness, a summary of audit findings and related trends observed across audits, issues surfaced through Public Interest Reports and statutory recommendations, an overview of value for money findings across the sector and details of authorities unable to appoint an auditor.

Respondents also sought a clear distinction between ARGA’s need to report on its own activities as system leader and the separate need for both a clear overview of the state of the local audit market and a summary of local audits.

Government response

The government welcomes the broad support for this proposal and the key elements we have proposed for the annual reporting process. The Government will work with the FRC to progress this, including taking into consideration the comments of respondents.

Board membership

The White Paper Restoring Public Trust in Corporate Reporting and Governance set out that ahead of ARGA’s establishment, the existing FRC board should be refreshed with members equipped to deliver the new regulator’s expanded remit and should be reduced in size. It was also proposed that board appointments should be made by the Secretary of State for Business, Energy and Industrial Strategy (BEIS), subject to an open and fair recruitment process.

Paragraphs 63-65 of the consultation reprised these proposals and proposed that the future ARGA board should include a nominated member with responsibility for local audit. It was further proposed that BEIS would liaise with DLUHC on the criteria for board appointments to ensure that these reflect the needs of local audit.

Question 11: Do you agree with the proposal outlined above relating to board responsibility for local audit? Please let us know any comments you have on the proposal.

Summary of responses

There was strong support for a board appointee with responsibility for local audit. Some respondents said that DLUHC should exercise some oversight of the appointment process for the board member with responsibility for local audit, with one suggestion that the HCLG Select Committee should confirm the appointment. Other suggestions made included that the board member with responsibility for local audit should chair the Liaison Committee or maintain a reporting link with the Liaison Committee.

Government response

The government welcomes the support for this proposal and is fully committed to ensuring that board members have the diverse skills, experience, and knowledge to provide appropriate scrutiny and challenge to the ARGA executive team, including in relation to its local audit responsibilities.

The Business Secretary recently confirmed four new directors to the FRC Board, to work alongside Sir Jan du Plessis, who has been confirmed as the organisation’s new Chairman. These directors have experience across a range of sectors, including Sir Ashley Fox, who served for 8 years as a councillor for Bristol City Council, including as Chairman of the council’s Oversight and Scrutiny Committee. These new appointees will complement the existing board members, including the current Chief Executive, Sir Jon Thompson, who was previously Finance Director of North Somerset Council.

BEIS and DLUHC will continue to work together on the criteria for future board appointments ahead of the establishment of ARGA, including the board member who will have specific responsibility for local audit. This process will be enshrined in an MoU between the 2 departments, but we are not minded to create further administrative steps beyond this.

To complement this arrangement, the FRC also plans to appoint a senior advisor drawn from a local audit background. The FRC’s senior advisors provide advice, feedback and mentoring and act as sounding boards for ongoing issues and topics.

Funding of ARGA’s system leader role

Paragraphs 66-69 discussed the proposed funding model for the ARGA’s specific local audit responsibilities. The government’s response to the consultation Restoring Public Trust in Audit and Corporate Governance confirms its intention to give ARGA statutory powers to raise a levy, whereby the new regulator’s costs of carrying out its regulatory functions will be met by market participants.

The consultation set out that we had considered extending this arrangement for the local audit responsibilities. However, given ongoing market fragility, the consultation instead proposed that ARGA’s specific local audit responsibilities should be funded directly by the Government.

Question 12: Do you agree that the Audit, Reporting and Governance Authority’s (ARGA) local audit functions and responsibilities should be funded directly by the Department for Levelling Up, Housing and Communities (DLUHC) rather than a statutory levy?

Summary of responses

There was strong support for this proposal, with 93% either agreeing or partially agreeing with the proposal. Several respondents commented on the funding model, suggesting that it should be ring-fenced against any future changes.

Government response

The government welcomes the high level of support for this proposal and confirms its intention for ARGA’s local audit functions and responsibilities to be funded directly by the government. Given the nature of the planned arrangement, we do not judge that ring-fencing is necessary.

ARGA to act as system leader for health audit

Local government and health audit are currently aligned, sharing the same Code of Audit Practice. Accordingly, paragraphs 70-72 of the consultation invited views on whether ARGA should also assume system leadership for health audit, as many of the constraints and objectives we have set out for local government audit apply to health.

This would include NHS trusts and Clinical Commissioning Groups, plus NHS foundation trusts (which currently sit outside the scope of the 2014 Local Audit and Accountability Act).

In this case, the reporting and governance mechanisms we have set out for local audit would also apply to health audit. The Department for Health and Social Care (DHSC) supports continued alignment between the 2 audit systems.

Question 13: Do you agree that the Audit, Reporting and Governance Authority (ARGA) should also take on system leader responsibilities for health audit? Please let us know any comments you have on the proposal.

Question 14: If you agree that the Audit, Reporting and Governance Authority (ARGA) should assume system leader responsibilities for health audit, do you think any further measures are required to ensure that there is alignment across the broader system?

Summary of responses

There was strong support for this proposal, with respondents commenting that the current alignment whereby local government and health audit are governed by the same legislation and share the same Code should continue, which would require common system leadership.

It was further noted that Integrated Care Boards could lead to joint financial arrangements between health and local bodies, making strong alignment between the 2 audit systems even more important. Respondents noted that the same auditors work across both systems and the need to increase the supply of auditors was stressed.

It was also suggested that common system leadership could enable better coordination of the timing of end of year audit arrangements across local government and health audit. This could improve overall timeliness, as clashes and delays in local government audit are seen to have a knock-on effect on health audit, and vice versa.

Two respondents opposed ARGA acting as system leader for health, citing a potential conflict with DHSC’s responsibility to Parliament for DHSC and NHSE’s consolidated financial statements, plus a risk that the new regulator could be overly burdened by assuming system leadership for health, when the challenges facing health audit are less severe.

Government response

The government welcomes the support for ARGA to act as system leader for health audit, which we plan to progress; we agree that this should enable better coordination. Given the interdependencies between timings for health audit and wider local audit, we do not agree that ARGA’s establishment of system leadership for health audit should be delayed. And, for similar reasons, we do not agree that this would place an undue burden on the new regulator.

We do not agree that DHSC’s responsibility as Accounting Officer to report to Parliament is material to system leadership arrangements. Appropriate departmental oversight for health will be assured through the governance and accountability mechanisms we have proposed.

Appointing person arrangements

Paragraphs 77-87 of the consultation set out our proposals to maintain the existing audit appointment arrangements, which specify that principal authorities have responsibility for the appointment of their own auditors. However, regulations permit DLUHC to specify an organisation to act as an ‘Appointing Person’ for the bulk procurement of audit services to those local bodies that choose to opt-in. The current Appointing Person is PSAA.

The consultation also proposed strengthened governance across the system, including with the new system leader, to ensure that objectives are aligned across the system.

Question 15: Do you agree with the government’s proposals for maintaining the existing Appointing Person and opt-in arrangements for principal bodies but with strengthened governance across the system, including with the new system leader? Please let us know any comments you have on the proposal.

Question 15 responses

There was broad agreement on the proposals, with 90% either agreeing or partially agreeing. Some respondents commented on the future relationship between the Appointing Person and ARGA, with some suggestions that ARGA’s remit be expanded to monitor the performance of the Appointing Person, while others said that ARGA should not be closely involved in the procurement arrangements due to possible conflicts of interest. The importance of the Appointing Person and other parties working collaboratively was noted.

There were also comments on the way that the Appointing Person arrangements are operating currently, including the need for more effective contract management.

Government response

It remains the government’s view that the current Appointing Person arrangements should remain in place, including separate arrangements for health audit. These arrangements will continue to be kept under review.

The government agrees that it will be vital for the new system leader to collaborate effectively with key partners, including the Appointing Person (PSAA). Over the past 9 months, the Liaison Committee has agreed actions for all parties to support the development of PSAA’s strategy for the next procurement. This has included promoting the benefits of the scheme to firms and local bodies, and PSAA and the FRC working together on the methodology for evaluating bids from firms. It will be important for the new system leader to ensure that the Liaison Committee continues to support the Appointing Person throughout the next appointing period and at future procurements.

PSAA has sought to address feedback on its approach to procurement and contract management from audit firms and local bodies in its new procurement strategy, within the scope of its remit. This has included introducing an increased number of lots, a Dynamic Purchasing System and other measures to encourage new firms to enter the market. PSAA has continued to progress its procurement strategy and, following a high number of opt-ins (99% of eligible local bodies) and good feedback from audit firms at the Selection Questionnaire stage, proceeded to issue the Invitation to Tender in April. Firms are eligible to submit bids for local audit contracts until 11 July.

In addition, new regulations designed to update and improve the process for the Appointing Person to set fee scales and fee variations came in force on 16 February 2022. We are hopeful that the new regulations will have a positive effect on the fee-setting process through the contract periods.

Over the longer-term, we will continue to review whether the current arrangements are working as effectively as they can and consider whether any further changes to regulations might be necessary.

Enhancing the functions of local audit and the governance for responding to its findings

Guidance on audit committees reinforce that they are a vital part of an organisation, supporting good governance, strong public financial management and effective internal audit and external audit. The Redmond Review recommended that local authorities should review their governance arrangements, including ‘the composition of their audit committees to include at least one independent member, suitably qualified’.

Paragraphs 96 and 97 of the consultation set out our proposals to ensure that strengthened guidance is developed to support local authorities to manage their audit committee arrangements, and the longer-term improvement of audit committee arrangements and delivery of good practice. It was proposed that this would be delivered through the production of an updated version of CIPFA’s existing guidance, Audit Committees: Practical guidance for local authorities and police.

CIPFA guidance makes clear that an Audit Committee is required as part of robust arrangements for governance and financial management. However, as Sir Tony highlighted in his report, it is not a statutory requirement for most types of local authority to have an audit committee. Paragraphs 98-100 of the consultation discuss audit committee arrangements and ask respondents to reflect on whether audit committees and several aspects of them should be made statutory.

In the interests of transparency and accessibility, a local body’s public accountability is best served by raising important matters at Full Council (or Police equivalent) as this is more visible to the public. The Redmond Review found that some serious matters had not been passed to Full Council when first presented to the Audit Committee and there was concern that if this was widespread practice, serious governance or financial resilience issues may be unsighted and addressed by elected members.

Question 16: Do you agree with the proposal for strengthened audit committee guidance? Please let us know any comments you have on the proposal.

Question 17: Do you have any views on whether reliance on auditors to comment and recommend improvement in audit committee arrangements is sufficient, or do you think the department should take further steps towards making the committee a statutory requirement?

Question 18: Do you agree with the proposals that auditors should be required to present an annual report to Full Council, and that the Audit Committee should also report its responses to the Auditor’s report? Please let us know any comments you have on the proposal.

Summary of responses

Two thirds of those who responded to this question either agreed or partially agreed. There were specific comments that Guidance should state that members should be on Audit Committees for longer and that they should be de-politicised. Respondents found that audit committee membership and decisions in the council often reflect its political inclination, which they believed could undermine the independence of the committee. It was also suggested that Audit Committees should review draft accounts before they are submitted to audit firms for review.

It was also felt that training and experience need to be included. Committee members should have the right skills and appropriate expertise, including sector-specific knowledge and experience, along with continued professional development.

There was a more mixed response to whether audit committees should be made statutory. Some respondents were supportive of making them statutory, noting that this would ensure consistency in arrangements with other sectors, and that this would allow for improved transparency and accountability.

Local authority respondents were more likely to be opposed to mandating Audit Committees, suggesting that it could undermine accountability of Full Council or prevent bodies tailoring committee arrangements to local need. Some respondents also said the fact that auditors could give a view on whether arrangements were adequate was sufficient.

Most respondents either agreed or partially agreed that auditors should be required to present an annual report to Full Council, and that the Audit Committee should also report its responses to the Auditor’s report. However, there were some concerns about the specialist nature of the audit reports and suggestions this should only be by exception, i.e. when there was a qualified opinion or a Value for Money weakness, or that this would undermine the Audit Committee, which is supposed to have sufficient expertise.

Government response

The government welcomes the strong support for strengthened guidance. The government has fed back the key comment themes to CIPFA, as they developed the guidance further, in consultation with other stakeholders. Government has worked with partners to ensure consultation views are reflected on the composition of the audit committees and its reporting mechanisms which it considers to be a relatively simple and cost-effective step in ensuring transparency across the sector. CIPFA published its Position Statement and supporting guidance in April 2022 which recommends the need for audit committees to be apolitical, for improved preparedness for external audit arrangements, ensuring membership has the right expertise, and reporting and publishing annually on committee effectiveness. This guidance was published in April 2022.

The government accepts there are different perspectives on whether Audit Committees should be a statutory requirement, and notes that fundamentally it is very important that local authorities are able to tailor their structures to local need.

There are, however, benefits to mandating audit committees, including increased transparency and consistency. Redmond found that arrangements for the Police were working effectively, while Major Combined Authorities were also required to have them, making local authorities an anomaly. Strengthened audit committees have also been a key issue in recent Public Interest Reports.

Fundamentally, it is important that councils, as with other public bodies, have appropriate measures in place: the government considers it proportionate to establish a simple principle that local authorities should have an audit committee, with at least one independent member. Mandating for audit committees would ensure widespread take-up, along with improved public accountability.

Consequently, based on the consultation feedback, we will be making Audit Committees, with at least one independent member, a mandatory requirement, once Parliamentary time allows.

We will continue to consult with partners on how this should be implemented. In the intervening period, the government would encourage local bodies to establish their arrangements in line with CIPFA’s guidance, including appointing independent members. We are providing £15m per annum to local bodies over the next 3 years to support with increased new burdens from the Redmond Review and increasing audit demands.

The government has also noted the importance of training. To support capability further, government is providing funding via the Local Government Association sector grant, for targeted training events for audit committee chairs and members. The government continues to work with the LGA on expanding their offer during 2022/23.

Auditor training and qualifications

Paragraphs 108-119 of the consultation address auditor training and qualifications. In his independent Review, Sir Tony highlighted significant evidence of market stress in the supply of appropriately experienced and qualified local authority auditors and suggested several reasons for this.

The consultation highlighted work underway by the FRC and other stakeholders to review the current guidance on entry requirements for Key Audit Partners (KAP) in local audit and to consider what else is possible to ensure that firms with the capacity, skills and experience are not excluded from bidding on local audit work. The consultation also sought views on whether changes might be needed to regulations to facilitate increased capacity and capability.

Question 19: Do you have any comments on the proposals for amending Key Audit Partner guidance or addressing concerns raised about skills and training?

Question 20: Are there other changes that might be needed to the Local Audit (Auditor Qualifications and Major Local Audit) Regulations 2014 alongside changes to the Financial Reporting Council’s (FRC) guidance on Key Audit Partners?

Question 21: Are there other changes that we should consider that could help with improving the future pipeline of local auditor supply?

Summary of responses

There was general agreement from respondents on the importance of widening the pool of KAP, including the need to support alternative routes to becoming a KAP and make allowances to ensure that there was sufficient time and ability for new KAP entrants to complete the registration process to support new firms to enter the market.

Respondents also noted that it was important that it remained a requirement to ensure ongoing experience and accreditation, and that it was important to increase capacity but without lowering standards. And that to deliver this would require improved training to ensure new entrants could develop sector specific knowledge.

A number of respondents noted that NHS foundation trusts have an option to appoint an auditor based on Companies Act eligibility alongside an option based on the KAP requirement, commenting that this should be maintained to avoid further pressure on market supply.

There was a broad consensus from respondents that the Regulations were adequate, and that the priority needed to be to ensure capacity through adequate sector knowledge and training.

Respondents said that there was a need to review and invest in specialised training for the sector, including a ‘top up’ qualification, as well as for firms to review their practices for recruitment and use current skills for succession planning and plugging gaps. It was noted that it was important to explore interchangeability between public and private audit experience to support local audit capacity.

Government response

The government welcomes the significant interest in widening the pool of KAPs. To address this, the FRC has consulted on proposals to enable alternative routes to obtain KAP status and allow local audit Recognised Supervisory Bodies’ greater discretion in determining suitability of the experience gained by KAP applicants without reducing quality. The FRC consulted on the current guidance in Spring 2022 and plans to publish updated guidance shortly.

Alongside this, the government has considered the case for a new technical advisory service proposal from the working group formed to respond to the Redmond Review. The government will be undertaking a process of pre-market engagement to test appetite ahead of a possible procurement to fund the establishment of this new service. In the longer term, the expectation is that this would need to be funded by firms, provided there is sufficient interest.

It is anticipated that this would support on topics unique to the local government sector. This could be by providing the local audit system with advice and guidance to local auditors on issues responding to electors’ objections, how and when to produce a public interest report, performance audit issues (for VfM reporting) and whether an issue identified meets the threshold for issuing a public interest report.

Looking ahead, the government is proposing that, following the outcome of the next local audit procurement, DLUHC will work with the new system leader and one or two of the successful audit firms to develop an industry-led workforce strategy, to consider the future pipeline of local auditors, and associated questions related to training and qualifications. This will form part of the new system leader’s broader role in setting out the future priorities for the local audit system.

Annex A: Responses per question

1. Do you agree with the proposed functions which the system leader for local audit needs to enable a joined-up response to challenges and emerging priorities across local audit? Please select one answer and let us know any comments you have on the proposal.

| 50/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 29 | 58% |

| I partially agree with the proposed | 14 | 28% |

| No, I disagree with the proposed | 6 | 12% |

| Unsure | 1 | 2% |

2. Do you have any comments on the proposed functions that ARGA should have alongside its new system leader responsibilities? Please let us know any comments you have on the proposal.

| 29/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 6 | 21% |

| I partially agree with the proposed | 14 | 48% |

| No, I disagree with the proposed | 5 | 17% |

| Unsure | 4 | 14% |

3. Do you agree that the system leader should conduct a full post implementation review to assess whether changes to the Code of Audit Practice have led to more effective external audit consideration of financial resilience and value for money matters 2 years after its introduction, with an immediate technical review to be conducted by the NAO? Please select one answer and let us know any comments you have on the proposal.

| 46/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 28 | 61% |

| I partially agree with the proposed | 16 | 35% |

| No, I disagree with the proposed | 2 | 4% |

4. Do you agree with the proposals to ensure that ARGA has sufficient expertise and focus on local audit? Please select one answer and let us know any comments you have on the proposals.

| 49/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 24 | 49% |

| I partially agree with the proposed | 16 | 33% |

| No, I disagree with the proposed | 7 | 14% |

| Unsure | 2 | 4% |

5. Do you agree with the proposed role and scope of the Liaison Committee? Please select one answer and let us know any comments you have on the proposal.

| 49/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 24 | 49% |

| I partially agree with the proposed | 11 | 23% |

| No, I disagree with the proposed | 12 | 24% |

| Unsure | 2 | 4% |

6. Do you agree that the responsibilities set out above will enable ARGA to act as an effective system leader for local audit? Are there any other functions you think the system leader for local audit should have?

| 47/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 18 | 38% |

| I partially agree with the proposed | 17 | 36% |

| No, I disagree with the proposed | 9 | 19% |

| Unsure | 3 | 7% |

7. What is your view on the proposed statutory objective for ARGA to act as system leader for local audit? Please include any comments on the proposed wording.

There were 47 responses to this part of the question.

8. Do you agree with the proposal that ARGA will have a responsibility to give regard to the value for money considerations set out in the Local Audit and Accountability Act 2014? Please choose one answer and include any comments on the proposed wording.

| 43/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 34 | 79% |

| I partially agree with the proposed | 6 | 14% |

| No, I disagree with the proposed | 2 | 5% |

| Unsure | 1 | 2% |

9. Do you agree that the proposals outlined above will provide an appropriate governance mechanism to ensure that the new system leader has appropriate regard to the government’s overarching policy aims without compromising its operational and regulatory independence? Please choose one answer and let us know any comments you have on the proposal.

| 43/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 22 | 51% |

| I partially agree with the proposed | 12 | 28% |

| No, I disagree with the proposed | 6 | 14% |

| Unsure | 3 | 7% |

10. Do you agree that ARGA’s annual reporting should include detail both on the state of the local audit market, and ARGA’s related activities, but also summarising the results of audits? Please choose one answer and include any views on other things you think this should include.

| 46/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 31 | 68% |

| I partially agree with the proposed | 12 | 26% |

| No, I disagree with the proposed | 2 | 4% |

| Unsure | 1 | 2% |

11. Do you agree with the proposal outlined above relating to board responsibility for local audit? Please choose one answer and let us know any comments you have on the proposal.

| 45/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 22 | 49% |

| I partially agree with the proposed | 14 | 31% |

| No, I disagree with the proposed | 5 | 11% |

| Unsure | 4 | 9% |

12. Do you agree that ARGA’s local audit functions and responsibilities should be funded directly by MHCLG rather than a statutory levy?

| 47/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 42 | 89% |

| I partially agree with the proposed | 2 | 5% |

| No, I disagree with the proposed | 1 | 2% |

| Unsure | 2 | 4% |

13. Do you agree that ARGA should also take on system leader responsibilities for health audit? Please let us know any comments you have on the proposal.

| 39/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 29 | 74% |

| I partially agree with the proposed | 4 | 10% |

| No, I disagree with the proposed | 6 | 16% |

14. If you agree that ARGA should assume system leader responsibilities for health audit, do you think any further measures are required to ensure that there is alignment across the broader system?

| 42/57 responses | ||

|---|---|---|

| Yes | 22 | 52% |

| No | 4 | 10% |

| Unsure | 16 | 38% |

15. Do you agree with the government’s proposals for maintaining the existing Appointing Person and opt-in arrangements for principal bodies but with strengthened governance across the system, including with the new system leader? Please let us know any comments you have on the proposal.

| 41/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 23 | 56% |

| I partially agree with the proposed | 14 | 34% |

| No, I disagree with the proposed | 2 | 5% |

| Unsure | 2 | 5% |

16. Do you agree with the proposal for strengthened audit committee guidance? Please let us know any comments you have on the proposal.

| 44/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 23 | 52% |

| I partially agree with the proposed | 15 | 34% |

| No, I disagree with the proposed | 6 | 14% |

17. Do you have any views on whether reliance on auditors to comment and recommend improvement in audit committee arrangements is sufficient, or do you think the Department should take further steps towards making the committee a statutory requirement?

There were 47 responses to this part of the question.

18. Do you agree with the proposals that auditors should be required to present an annual report to Full Council, and that the Audit Committee should also report its responses to the Auditor’s report? Please let us know any comments you have on the proposal.

| 47/57 responses | ||

|---|---|---|

| Yes, I agree to the proposed | 20 | 43% |

| I partially agree with the proposed | 12 | 25% |

| No, I disagree with the proposed | 13 | 28% |

| Unsure | 2 | 4% |

19. Do you have any comments on the proposals for amending Key Audit Partner guidance or addressing concerns raised about skills and training?

There were 45 responses to this part of the question.

20. Are there other changes that might be needed to the Local Audit (Auditor Qualifications and Major Local Audit) Regulations 2014 alongside changes to the FRC’s guidance on Key Audit Partners?

There were 36 responses to this part of the question.

21. Are there other changes that we should consider that could help with improving the future pipeline of local auditor supply?

There were 49 responses to this part of the question.

Annex B: Update to original Redmond Review recommendations

Action to support immediate market stability (recommendations 5, 6, 8, 10, 11)

| Redmond Review - key recommendations | December 2020/ May 2021 Response | February 2022 update |

|---|---|---|

| 5. All auditors engaged in local audit be provided with the requisite skills and training to audit a local authority irrespective of seniority. | Accept; we will work with the ICAEW, CIPFA and FRC to deliver this recommendation. | In progress. The Government is currently undertaking a process of pre-market engagement to test appetite ahead of a possible procurement to fund a new technical advisory service to provide specialist training to auditors. |

| 6. The current fee structure for local audit be revised to ensure that adequate resources are deployed to meet the full extent of local audit requirements. | Accept. | Delivered. On 16 February 2022, new regulations designed to streamline the process for the Appointing Person to set fee scales and fee variations came in force. We are providing £15m additional funding to local bodies in 21/22 and have committed to £45m further funding over the course of the next Spending Review period. |

| 8. Statute be revised so that audit firms with the requisite capacity, skills and experience are not excluded from bidding for local audit work. | Partially accept; we will work with the FRC and ICAEW to deliver this recommendation, including whether changes to statute are required. | In progress. The FRC is consulting on changes to its Key Audit Partner guidance, and of potentially publishing updated guidance in Spring 2022. Following consultation, it has been confirmed that changes to statute are not necessary. |

| 10. The deadline for publishing audited local authority accounts be revisited with a view to extending it to 30 September from 31 July each year. | Partially accept; we will look to extend the deadline to 30 September for publishing audited local authority accounts for 2 years, and then review. | Delivered. In addition, we intend to extend the deadline for the 21/22 accounts, before reverting to 30 September for 6 years, until the 27/28 accounting year. |

| 11. The revised deadline for publication of audited local authority accounts be considered in consultation with NHSE/I and DHSC, given that audit firms use the same auditors on both Local Government and Health final accounts work. | Accept. | Delivered. Regulations extending the audit publication deadline to 30 September for 2 years came into force on 31 March 2021. |

Consideration of system leadership options (recommendations 1, 2, 3, 7, 13, 17)

| Redmond Review - key recommendations | December 2020/ May 2021 Response | February 2022 update |

|---|---|---|

| 1. A new body, the Office of Local Audit and Regulation (OLAR), be created to manage, oversee and regulate local audit. 2. The current roles and responsibilities relating to local audit discharged by PSAA, ICAEW, FRC/ARGA and C&AG be transferred to the OLAR. |

Partially accept; We accept the need for a single organisation to have responsibility for leadership of the local audit system, including oversight of the quality framework and encouraging competition in the local audit market. We do not accept that a new body needs to be created to undertake these functions, and think that these functions, as well as an overarching responsibility for system leadership and encouraging competition in the local audit market, should be undertaken by the Audit, Reporting and Governance Authority (ARGA), set to be established to replace the Financial Reporting Council. We do not accept that this body should also have responsibility for procurement and management of local audit contracts, and think that these should functions should continue to be undertaken by PSAA. | In progress. This consultation response confirms the next steps for establishing the ARGA to manage, oversee and regulate local audit, with work ongoing to ensure that the Financial Reporting Council is ready to start functioning in shadow form from the first quarter of financial year 2022-23. Statutory responsibilities will transfer to ARGA once primary legislation allows. |

| 3. A Liaison Committee be established comprising key stakeholders and chaired by MHCLG, to receive reports from the new regulator on the development of local audit. | Partially accept; we will establish this new Liaison Committee, but think that this should be chaired by ARGA as the ‘system leader’ once the new arrangements our established. DLUHC will chair this in the intervening period. | Delivered. The Liaison Committee has now been established with committees meeting regularly to discuss key issues affecting the Local Audit sector. DLUHC will continue to chair this important committee whilst ARGA is operating in shadow with the intention of migrating the role fully to ARGA in due course. |

| 7. That quality be consistent with the highest standards of audit within the revised fee structure. In cases where there are serious or persistent breaches of expected quality standards, OLAR has the scope to apply proportionate sanctions. | Partially accept; we will work with stakeholders to consider whether additional sanction powers, beyond the audit enforcement procedures that ARGA will already have, are necessary. | We are currently not minded of the case for additional sanctions powers beyond the audit enforcement procedures already available. |

| 13. The changes implemented in the 2020 Audit Code of Practice are endorsed; OLAR to undertake a post implementation review to assess whether these changes have led to more effective external audit consideration of financial resilience and value for money matters. | Accept; we have endorsed the changes to the 2020 Audit Code of Practice, and will look to ARGA to undertake a post implementation review to assess whether these changes have led to more effective external audit consideration of financial resilience and value for money matters in due course. | In progress. This consultation response confirms the expectation of a post-implementation review, to be completed within 3 years on the new Code being implemented. |

| 17. MHCLG reviews its current framework for seeking assurance that financial sustainability in each local authority in England is maintained. | Accept; DLUHC carries out a range of assurance activity, drawing on local authority data and financial metrics and soft intelligence from engagement with the sector. We have undertaken additional data collection in 2020-21 to provide government with robust data on local financial pressures in the context of the Covid-19 pandemic and has also implemented a consistent process to engage with local authorities facing financial challenges and, where appropriate, provide exceptional financial support. | Delivered. |

Enhancing the functioning of local audit, and the governance for responding to its findings (recommendations 4, 9, 12, 18)

| Redmond Review - key recommendations | December 2020/ May 2021 Response | February 2022 update |

|---|---|---|

| 4. The governance arrangements within local authorities be reviewed by local councils with the purpose of: an annual report being submitted to Full Council by the external auditor; consideration being given to the appointment of at least one independent member, suitably qualified, to the Audit Committee; and formalising the facility for the CEO, Monitoring Officer and Chief Financial Officer (CFO) to meet with the Key Audit Partner at least annually. |

Accept; we will work with the LGA, NAO and CIPFA to deliver this recommendation. | In progress. We consulted on proposals to deliver this recommendation as part of our technical consultation. CIPFA is due to publish new, strengthened guidance relating to the operation of audit committees, with the endorsement of other key stakeholders in April 2022. DLUHC plans to legislate to make it a statutory requirement to submit an annual report to Full Council and have an Audit Committee, with at least one independent member. |

| 9. External Audit recognises that Internal Audit work can be a key support in appropriate circumstances where consistent with the Code of Audit Practice. | Accept; we will work with the NAO and CIPFA to deliver this recommendation. | In progress. We emphasised the importance and value of internal audit within local government bodies and the importance of operating in accordance with the requirements of the Accounts and Audit Regulations 2015, as part of our summer consultation, and the NAO is considering how this might also be reinforced through auditor guidance notes. |

| 12. The external auditor be required to present an Annual Audit Report to the first Full Council meeting after 30 September each year, irrespective of whether the accounts have been certified; OLAR to decide the framework for this report. | Accept; we will work with the LGA, NAO and CIPFA to deliver this recommendation, including whether changes to statute are required | In progress. We consulted on this matter in our technical consultation. This will be reflected in updated guidance, and also amendments to regulations. |

| 18. Key concerns relating to service and financial viability be shared between Local Auditors and Inspectorates including Ofsted, Care Quality Commission and HMICFRS prior to completion of the external auditor’s Annual Report. | Accept; we will work with other departments and the NAO to deliver this recommendation. | In progress. We have had discussions with the NAO and others to start to take this forward. |

Improving transparency of local authorities’ accounts to the public (recommendations 19, 20, 21, 22)

| Redmond Review - key recommendations | December 2020/ May 2021 Response | February 2022 update |

|---|---|---|