Opening a Lifetime ISA

How to get started with your account

To be eligible for a Lifetime ISA, you must be:

- between the ages of 18 and 39

- a UK resident, or a member of the armed forces serving overseas, or their spouse/civil partner

One Lifetime ISA per person, per tax year

Lifetime ISAs are opened by individuals – you cannot open them with someone else. This is the same for all ISAs. If you plan to buy a home with someone else who is also a first-time buyer, you can each open and save money into your own Lifetime ISA account. You must both meet the individual eligibility criteria (above).

You can open more than one Lifetime ISA during your life, but you can only open one per tax year and put money into one per tax year. Each time you apply for a new Lifetime ISA you will still need to meet the eligibility criteria (above) for opening an account.

Saving into a Lifetime ISA

How much you can save and how it affects your other ISAs

As long as you have opened an account before you turn 40, you can pay into a Lifetime ISA up to the day before you turn 50.

You can save up to £4,000 into a Lifetime ISA during each tax year, as long as you’re not saving more than the annual overall ISA limit.

The annual overall ISA limit is the maximum total amount you can save into all your ISAs each tax year. The limit for the 2018 to 2019 tax year will be £20,000. Any contribution to a Lifetime ISA counts towards this.

Learn more about the ISA annual overall limit.

You can transfer your Help to Buy ISA into a Lifetime ISA, but it will count towards your £4,000 annual limit.

The government bonus

How it’s calculated and how you get it

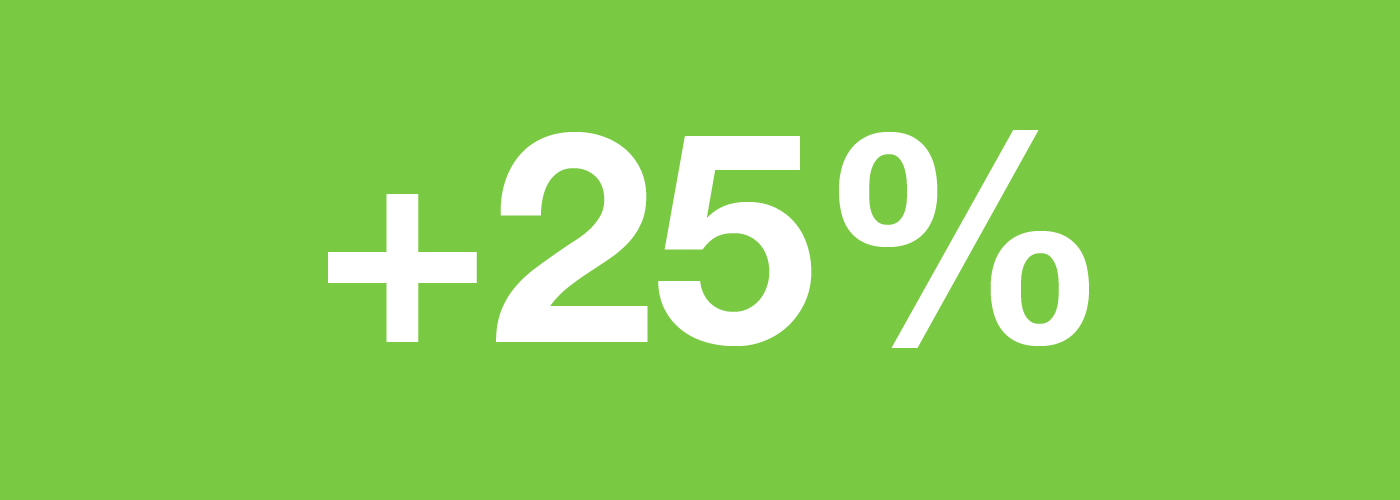

The government will give you a 25% bonus on the total amount you pay into your Lifetime ISA, not including investment interest or investment growth.

That means if you pay in the maximum amount of £4,000 in a year, you’ll receive a tax-free bonus of £1,000 that year.

Money transferred into a Lifetime ISA from another ISA is also eligible for the government bonus.

Once the government bonus has been paid into your Lifetime ISA account, you can invest it just like your other savings and will be able to earn interest or get investment growth on it.

How you claim the bonus

Your Lifetime ISA manager will claim the bonus for you and it will be added automatically to your Lifetime ISA account. Your Lifetime ISA manager is the bank, building society or asset manager where you open your Lifetime ISA.

The bonus will be added to your account every month.

From April 2018 any bonus will be added to your account every month.

If you withdraw money from your Lifetime ISA before you have received the government bonus you will still be entitled to the bonus on your contributions. Your Lifetime ISA manager will claim the bonus in the same way as if the funds had not been withdrawn and pay that bonus to you (either into your Lifetime ISA or directly to you).

Special rules apply to withdrawals in the 2017-18 tax year or if you wish to cancel an account within 30 days of opening it.

If my Lifetime ISA manager does not claim my bonus from HMRC in time what will happen?

In 2017-18 your Lifetime ISA manager will make a single claim for the whole year between 6 April 2017 and 19 April 2018.

In subsequent years the claims will be made for each month in which you make a contribution. Your Lifetime ISA manager will make the claim by the 19th day of the month following your qualifying addition to the account.

If your Lifetime ISA manager does not make the claim that month they can make it in the claim period for a subsequent month.

Is the Lifetime ISA an alternative for a pension?

The Lifetime ISA is designed to be a complement to pensions saving, not a replacement. Pension contributions can receive substantial tax relief, and your employer may make contributions to your pension as well.

The Lifetime ISA does not affect an employer’s obligation to automatically enrol their employees into a workplace pension and contribute to it.

If you are thinking about opting out of a workplace pension you should consider this decision carefully, and may wish to take advantage of free information about pensions through The Pension Advisory Service.

Withdrawing: the basics

You can withdraw your funds, including the government bonus, without a government charge in any of the following circumstances:

- to help buy a first home worth up to £450,000 at any time from 12 months after you first save into the account

- if you become terminally ill

- from the age of 60

If you close the account within a 30 day cooling off period (as set out by the Financial Conduct Authority), no government charge is payable. You will not receive any government bonus on money you paid into the account.

Fees and charges for managing a Lifetime ISA may be paid directly to the Lifetime ISA manager from your Lifetime ISA without incurring a government withdrawal charge.

Withdrawing for your first home

You must be a first-time buyer to put the Lifetime ISA towards your first home. A first-time buyer is someone who does not own, and has never owned, a home anywhere in the UK or the rest of the world.

Read guidance on first-time buyers.

To be able to be eligible for the government bonus, you must have opened a Lifetime ISA at least 12 months ago.

The home you buy must:

- be in the UK

- have a price of £450,000 or less

- be the only home you will own

- be where you intend to live

- be purchased with a mortgage

If you’re buying with someone else and they are also a first-time buyer, you can put both bonuses towards the purchase of your home. The price of the home still mustn’t be more than £450,000.

If you’re buying a home with someone who has owned a property before they don’t count as a first-time buyer. But you can still put your own bonus towards the price of the home you’re buying together.

You can use your Lifetime ISA with other government schemes as long as you meet the eligibility requirements of the other schemes you wish to participate in.

Learn more about government housing schemes.

You can use the Lifetime ISA to buy land for a self-build property as long as the purchase meets all the other criteria for property purchase through the scheme.

Speak to your solicitor or conveyancer if you’re not sure whether the property you are purchasing is within the price limit of the Lifetime ISA and if you can use your government bonus.

Planning your purchase

Lifetime ISA funds, including the bonus, can be put towards an exchange deposit, provided the property purchase is completed within 90 days of your conveyancer receiving the withdrawn funds from your Lifetime ISA manager.

If it’s taking longer than 90 days for your property purchase to go through, your conveyancer can write to HMRC for an extension.

There is no restriction on which stage of the property purchase you can put your Lifetime ISA funds towards. If it meets the conditions above, you will be able to put them towards a deposit at exchange of contracts.

Problems when buying your home

If your property purchase doesn’t go through your conveyancer must return all of the funds to your Lifetime ISA.

The amount returned must be the same that left the account. Any interest you have earned on funds while held by your conveyancer can be paid direct to you and will not count as a withdrawal.

If the house you are buying is not eligible for the Lifetime ISA then you will not be able to pay for it with a charge-free withdrawal. If you do withdraw money from your Lifetime ISA in these circumstances then a charge will be applied on the amount withdrawn.

Buying with joint property ownership

You can use your Lifetime ISA savings to buy your first home with someone else, regardless of whether they have their own Lifetime ISA. If you both have Lifetime ISAs you can both use them towards your home together. That includes tenants-in-common and joint tenants.

However, you can still only put your Lifetime ISA towards a property valued at £450,000 or less. That price cap applies to the full sale price for the whole property rather than just the share you are buying.

Buying with a shared ownership scheme

If buying with a shared ownership properties the £450,000 price cap applies to the full sale price of the property rather than just the share you initially buy. For shared ownership properties the full sale price is calculated as a multiple of the equity share you are buying.

This means if you are purchasing a 25% equity share of a property for £50,000, the full sale value is £200,000.

Your conveyancer can calculate the sale price based on the price paid for the equity share you are buying plus the net present value of rental payments due over the term of the lease.

Guidance for armed forces members and other Crown servants

If you are a Crown servant, such as a member of the armed forces serving overseas (or are their spouse or civil partner) and you intend to use the property as your main residence, then you will be eligible for the scheme even if you are unable to live in it as your main home when you first purchase it. When you first purchase your property, you will be able to rent it out until you are able to move in.

Withdrawing after you turn 60

After you turn 60, money you withdraw from your Lifetime ISA account is restriction-free and doesn’t incur a government charge.

If your Lifetime ISA manager offers it, funds can remain invested and any interest or investment growth will continue to be tax-free. You could also transfer your savings to another type of ISA

What happens to my Lifetime ISA if I become terminally ill or die?

If you become terminally ill and have less than 12 months to live, you can withdraw from your ISA without a government charge. You will still be eligible for the government bonus.

On death, your Lifetime ISA will form part of your estate for inheritance tax purposes. As the money will no longer be inside a Lifetime ISA wrapper, no government charge will apply on withdrawals.

Withdrawing for any other reason

A Lifetime ISA is intended to be a long-term savings product. It is not designed to encourage regular withdrawals. If you withdraw money for any reason other than buying your first home, at age 60 or if you are terminally ill, a charge of 25% will be applied to the amount you wish to withdraw. On death, no withdrawal charge will apply to Lifetime ISA savings.

The withdrawal charge aims to recover the government bonus received and apply an extra charge to the original savings. This means if you treat your Lifetime ISA as a short-term savings product, you could get back less than you paid in.

Example 1

Assuming no growth, initial savings of £800 will earn a 25% government bonus of £200 and give you a pot of £1,000. If you wish to withdraw the entire pot, a 25% charge will apply to the full £1,000. You will have to pay a government withdrawal charge of £250. This will leave you with £750, which is £50 less than you originally paid in.

If you only wish to access some of your money, you will have to take the withdrawal charge into account when requesting funds. You will have to withdraw more than the amount you need, to cover your needs and the 25% withdrawal charge.

Example 2

If you need enough cash to cover a £120 bill, you will have to withdraw more than you actually require. Withdrawing £160 means you pay a 25% withdrawal charge of £40, and receive £120 in cash to meet the bill.

I am having problems with my Lifetime ISA and wish to make a complaint.

If your complaint is about your Lifetime ISA manager or anything to do with the management of your account you should complain directly to them.

If you are not satisfied with your ISA manager’s response to your complaint, you can contact the Financial Ombudsman Service:

complaint.info@financial-ombudsman.org.uk

0300 123 9123

If your complaint is about your solicitor or conveyancer you should complain directly to them.

If you are not satisfied with your solicitor’s or conveyancer’s response to your complaint, in England and Wales you can contact the Legal Ombudsman:

http://www.legalombudsman.org.uk/

0300 555 0333

In Scotland you can contact the Scottish Legal Complaints Commission on 0131 201 2130.

In Northern Ireland you can contact the Law Society of Northern Ireland on 028 9023 1614.

If your conveyancer is not a registered solicitor you should make a complaint to the Council of Licensed Conveyancers. You can email them at clc@clc-uk.org or call them on 0207 250 8465.