Council Tax: practice notes

The Valuation Office Agency's (VOA) technical manual for assessing domestic property for Council Tax.

1. Introduction

The Local Government Finance Act (LGFA) 1992 requires the Commissioners of Inland Revenue (now HMRC) to carry out valuations of dwellings in England and Wales for the purposes of compiling and maintaining valuation lists (sections 20-23), and specifies bands within which dwellings are to be placed (Section 5). The Act also requires that a similar valuation exercise be carried out in Scotland by the Scottish Assessors, acting under the direction of the Commissioners.

The Council Tax (Situation and Valuation of Dwellings) Regulations 1992 as amended by The Council Tax (Situation and Valuation of Dwellings) (Amendment) Order 1994 (hereinafter referred to as “the regulations”) contain, inter alia, the basis of valuation to be adopted when banding for Council Tax purposes.

2. Definition of dwelling

It is Section 3 of the LGFA 1992 that defines what a “dwelling” is for CT and reads as follows:

-

This section has effect for determining what is a dwelling for the purposes of this Part.

-

Subject to the following provisions of this section, a dwelling is any property which -

a) by virtue of the definition of hereditament in section 115(1) of the General Rate Act 1967, would have been a hereditament for the purposes of that Act if that Act remained in force; and

b) is not for the time being shown or required to be shown in a local or a central non-domestic rating list in force at that time; and

c) is not for the time being exempt from local non-domestic rating for the purposes of Part III of the Local Government Finance 1988 Act (“the 1988 Act”);

and in applying paragraphs (b) and (c) above no account shall be taken of any rules as to Crown exemption.

- A hereditament which -

a) is a composite hereditament for the purposes of Part III of the 1988 Act; and b) would still be such a hereditament if paragraphs (b) to (d) of section 66(1) of that Act (domestic property) were omitted, is also, subject to subsection (6) below, a dwelling for the purposes of this Part.

- Subject to subsection (6) below, none of the following property, namely:

a) a yard, garden, outhouse or other appurtenance belonging to or enjoyed with property used wholly for the purposes of living accommodation; or

b) a private garage which either has a floor area of not more than 25 square metres or is used wholly or mainly for the accommodation of a private motor vehicle; or

c) private storage premises used wholly or mainly for the storage of articles of domestic use,

is a dwelling except in so far as it forms part of a larger property which is itself a dwelling by virtue of subsection (2) above.

(4A) Subject to subsection 6 below, domestic property falling within section 66(1A) of the 1988 Act is not a dwelling except in so far as it forms part of a larger property which is itself a dwelling by virtue of subsection (2) above.

- The Secretary of State may by order provide that in such cases as may be prescribed by or determined under the order -

a) anything which would (apart from the order) be one dwelling shall be treated as two or more dwellings; and

b) anything which would (apart from the order) be two or more dwellings shall be treated as one dwelling.

- The Secretary of State may by order amend any definition of “dwelling” which is for the time being effective for the purposes of this Part.”

2.1 Points to note:

In respect of the above definition, the following points are to be noted;

(i) Hereditament is defined in section 115(1) of the General Rate Act 1967 as being,

“property which is or may become liable to a rate, being a unit of such property which is, or would fall to be, shown as a separate item in the valuation list”. It is case law, however, that tells us what this means in practice.

- hereditament in relation to CT was examined in the case RGM properties v Speight LO 2011. In paragraphs 13-17 an analysis of the law was undertaken in relation to beneficial occupation. The authorities were examined and the practical definition linked to that expounded in Post Office v Nottingham City Council CA 1979 in the answer to the question “as a matter of fact and degree, is or will the building, as a building, be ready for occupation, or capable of occupation, for the purposes for which it is intended?”

- in both the RGM case and Wilson v Coll LO 2011, the need to separate the ‘hereditament test’ as to whether an existing property is capable of reasonable repair, and the valuation assumptions to be applied (see paragraph 3 below) once it was found that a hereditament existed, was emphasised

- in R v East Sussex Valuation Tribunal Ex p. Silverstone 1996 RVR 203, it was confirmed that where two separate dwellings are converted into a single unit, a new dwelling comes into existence

- the case of Baker (VO) v Citibank LT 2007 confirmed the principle that a change in the boundaries of a hereditament created a new hereditament. It follows from this that where a dwelling either acquires or disposes of land, to add or subtract from its boundaries (that is not merely de minimis in extent), a new dwelling will have been created in each case. In these circumstances a relevant transaction is not necessary to trigger a band review where material increases have taken place

- a dwelling which is removed from the list because it becomes non-domestic property will cease to be a dwelling. If subsequently it becomes domestic property again and qualifies as a dwelling, it will be treated as a new dwelling when brought back into a CT list. Any improvements which may have occurred will be taken into account as part of the new dwelling $LegislativeList

- i. Exemptions for the purposes of Part III of the LGFA 1988 are listed in its 5th Schedule.

- ii. Any property which satisfies the definition in Section 3 LGFA 1992 but is in the occupation of the Crown is nevertheless a dwelling for Council Tax purposes.

- iii. Any property which is a composite property as defined by Section 64(9) of the LGFA 1988 is a dwelling unless it forms such a hereditament by virtue of the fact that it contains only domestic property defined in paragraphs (b) to (d) of Section 66(1) of the 1988 Act.

-

iv. Any property included in those categories mentioned in S.3(4)(a) (b) and (c) LGFA 1992 will never constitute a dwelling in isolation. It will only ever be a dwelling to the extent that it forms part of a larger dwelling. Such property will only form part of a larger dwelling if, for the purposes of the General Rate Act 1967, it would have formed part of a hereditament as defined by S.115(1) e.g. a house and garage occupied together and situated within a single curtilage will together form a single dwelling. $EndLegislativeList

- a garage which is physically separated by a main road, from the dwelling house with which it is enjoyed, will not comprise a dwelling in its own right or be regarded as forming part of the dwelling. (It would have formed a separate hereditament for the purposes of the General Rate Act 1967). Similarly a garage situated within the curtilage of a block of flats will not comprise part of a dwelling if for the purposes of the 1967 Act it would have formed a separate hereditament. The value of any such garage should not be reflected directly in the value of the individual dwelling

- communal facilities such as car parking areas, gardens, communal lounges at a block of flats or sheltered housing development will not comprise a dwelling in their own right but the value of such facilities will fall to be reflected in the market values of the individual units

- in those instances where a facility is used by both owners of adjoining living accommodation, as a right of occupation of their respective hereditaments, and individuals living elsewhere (provided the latter use is not de minimis) it will have been treated as non-domestic property, e.g. leisure facilities at a luxury development. The right to use such facilities should be reflected in the market values of the individual dwellings

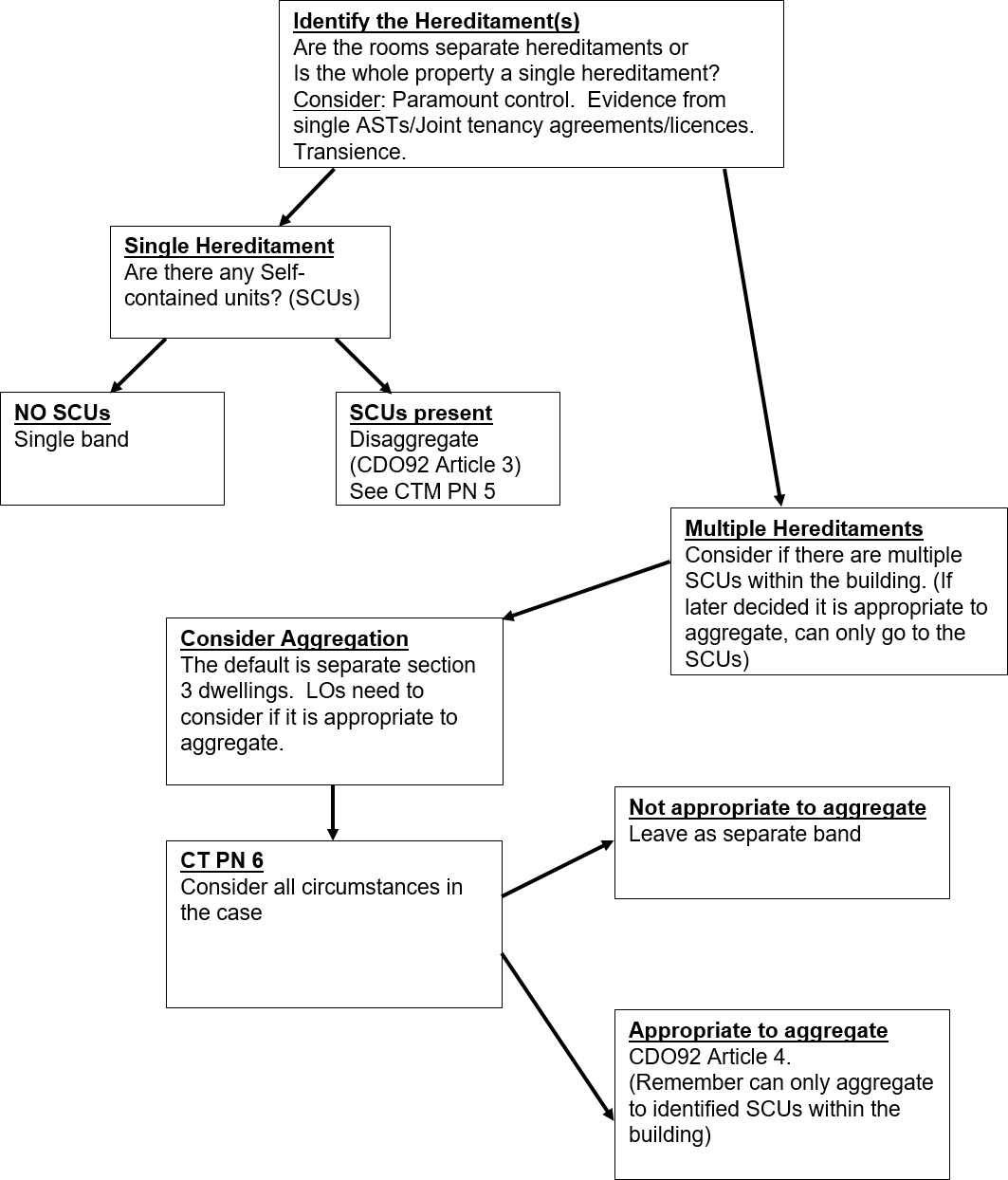

- i. The power conferred on the Secretary of State in subsection (5) has been exercised in the form of The Council Tax (Chargeable Dwellings) Order 1992 (SI No. 549) as amended by The Council Tax (Chargeable Dwellings, Exempt Dwellings and Discount Disregards) Amendment Order 1997 (SI No 656) and the Council Tax (Chargeable Dwellings, Exempt Dwellings and Discount Disregards)(Amendment) ( England) Oder 2003 SI 3121and the Health and Social Care Act 2008 (Consequential Amendments) (Council Tax) Order 2012. Articles 3 and 3A of the Order detail the circumstances where properties which would otherwise form single dwellings are to be treated as more than one. Article 4 gives the Listing Officer a discretion in prescribed circumstances to treat properties which would otherwise form multiple dwellings as single ones. For instructions on the disaggregation and aggregation of dwellings see CTM: PN5 and PN6 respectively.

- ii. From 1st April 2013 paragraph (4A) was added by the Non Domestic Rating and Council Tax (Definition of Domestic Property and Dwelling) (England) Order 2013. This is an amendment of Section 66 (1) LGFA 1988, which designates all small scale energy generation equipment, of sub 10 kilowatts capacity, as domestic property.

It should be noted that, for the purposes of the current lists, there is no evidence that such equipment (eg solar panels) which do form part of the dwelling where no 3rd party agreements exist, would have made any significant difference to property values under the valuation assumptions.

Where generation equipment is installed on part of the dwelling subject to a separate licence or lease agreement in favour of a 3rd party (the provider and owner of the equipment), that part including the generators will not form part of the dwelling. However, because it is still designated domestic property, will not be liable to non-domestic rates either. Thus, solar panels on roofs which are subject to 3rd party agreements will fall into the same category as private garages and private stores outside the dwelling boundaries and not be subject to local taxation or affect the underlying dwelling Band.

Basis of Valuation- Valuation Assumptions

The basis of valuation for any dwelling is found in Reg 6(1), (2) and (3) of The Council Tax (Situation and Valuation of Dwellings) Regulations 1992 (SI No. 550) as amended by the Council Tax (Situation and Valuation of Dwellings) (Amendment) Order 1994. Reg 7 simply sets out an apportionment approach for the valuation of a composites dwelling but does not affect the basic assumptions. Reg 6 is as follows:-

-

Subject to Reg 7, for the purposes of valuations under Section 21 (valuations for purposes of lists) of the Act, the value of any dwelling shall be taken to be the amount which, on the assumptions mentioned in paragraphs (2) and (3) below, the dwelling might reasonably have been expected to realise if it had been sold in the open market by a willing vendor on 1 April 1991.

-

The assumptions are:

(a) that the sale was with vacant possession;

(b) that the interest sold was the freehold or, in the case of a flat, a lease for 99 years at a nominal rent;

(c) that the dwelling was sold free from any rent charge or other encumbrance;

(d) except in a case to which paragraph (3) or (3A) applies, that the size, layout and character of the dwelling, and the physical state of its locality, were the same as at the relevant date;

(e) that the dwelling was in a state of reasonable repair;

(f) in the case of a dwelling, the owner or occupier of which is entitled to use common parts, that those parts were in a like state of repair and the purchaser would be liable to contribute towards the cost of keeping them in such a state;

(g) in the case of a dwelling which contains fixtures to which this sub-paragraph applies, that the fixtures were not included in the dwelling;*

(h) that the use of the dwelling would be permanently restricted to use as a private dwelling; and

(i) that the dwelling had no development value other than value attributable to permitted development.

*Reg 6(2)(g) only applies to fixtures which are designed to make a dwelling suitable for use by a disabled person and which add to the dwelling’s value - this is covered in Reg 6(4) (see paragraphs 4.14 & 4.15 below)

- In the case of a valuation carried out for the purposes of an alteration of the valuation list resulting from a material reduction in the value of the dwelling, it shall be assumed that –

-

a. the physical state of the locality of the dwelling was the same as on the date from which the alteration of the list would have effect; and

-

b. the size, layout and character of the dwelling were the same

-

i. in the case of an alteration resulting from a change to the physical condition of the dwelling, as on the date from which the alteration in the list would have effect;

-

ii. in a case where there has been a previous alteration of the valuation list in relation to the dwelling, as on the date from which that alteration had effect;

-

iii. in a case where in relation to the dwelling, there has been a relevant transaction within the meaning of Section 24, not resulting in an alteration of the valuation list, as on the date of that transaction;

-

iv. in a case to which more than one of sub-paragraphs (i) to (iii) applies, as on whichever is the latest of the dates there mentioned; and

-

v. in any other case, as on 1 April 1993.

- In the case of a valuation carried out for the purposes of an alteration to correct an inaccuracy in a list which arose –

(a) in the course of making a previous alteration which resulted from a material reduction in the value of the dwelling, or

(b) since the date of such an alteration by reason of an alteration which was the next alteration to be made and was neither the result of a material reduction in the value of the dwelling nor the occurrence of any of the events described in paragraph (5B) below.

it shall be assumed that the physical state of the locality of the dwelling, and the size, layout and character of the dwelling are the same as on the dates which were applicable in respect of the previous alteration in accordance with paragraph (3) above”. (4)..etc

The valuation approach for any dwelling which is a composite hereditament or part of a single property which is a composite hereditament is contained in regulation 7(1) of The Council Tax (Situation and Valuation of Dwellings) Regulations 1992. For instructions on the valuation of such dwellings see CTM: PN 2.

Interpretation and application of basis of valuation

4.1 Open market value as at 1 April 1991

a. “Reasonably expected” and “open market”

“Reasonably expected” and “open market” are not defined in the regulations but may be taken as having the same meaning as when used in a similar context in S.272(1) of the Taxation of Chargeable Gains Act 1992 and S.160 of the Inheritance Tax Act 1984.

It is therefore necessary to assume that,

-

i. all preliminary arrangements have been made prior to disposal

-

ii. adequate publicity has been given to the sale

-

iii. the most appropriate method of sale has been chosen so as to maximise the proceeds of the sale.

(NB Lotting - selling in parts - cannot be assumed as this would be inconsistent with the concept of the hereditament from which the dwelling is derived).

Problems can arise when a covenant is entered into a conveyance of the freehold or long leasehold interest, restricting the value on re-sale of the interest, to a percentage of the open market value of the dwelling. This restriction must be ignored for Council Tax purposes. (See paragraph 4.11 Restrictive Covenants).

Open market value will be determined by having regard to all the evidence of sales of similar dwellings in the locality at the antecedent valuation date (1 April 1991). Prices paid for new properties purchased from a builder should be treated with caution, since they often reflect a “new build premium” which will not be payable in the second-hand market from where the bulk of sales evidence is drawn.

(b) “Willing Vendor”

The term “willing vendor” is not defined in the regulations but may be taken to have the same meaning as “willing seller” as contained in S.5 of the Land Compensation Act 1961 (Rule 2) ie. not a person selling without reserve but one who does it as a free agent as opposed to one who is forced to sell.

(c) Special Purchaser and Marriage Value

The definition of open market value does not specifically exclude either a special purchaser or marriage value. However, an increase in value which is attributable to a situation where either a special purchaser or marriage value is seen to exist will often be excluded by virtue of Reg 6(2)(h) and (i) (ie the requirement to assume a restriction on use and limited development value only).

Where the existence of a special purchaser is identified and the above regulations would not be offended, regard should only be had to any overbid if it can be established that such a bid would have been made if the dwelling had been marketed at 1 April 1991.

(d) Number of properties assumed to be on the market as at 1 April 1991

No reduction should be made on account of a theoretical “flooding of the market” on 1 April 1991.

Regs 6 and 7 refer to the valuation of any one property as at the date of valuation and does not permit the assumption that all dwellings are placed on the market at the same time. In other words the valuer should consider that the equilibrium of the market place is maintained in the state which actually existed on 1 April 1991. Accordingly the valuation of any dwelling is to be approached as if it were simply one additional dwelling coming on to the existing market as at 1 April 1991.

(e) Unlawful use of property

Reg 6(2) does not require an unlawful use of a property to be disregarded.

The banding of any property where any unlawful use is apparent should therefore take into account the value which the market would have placed on that use as at 1 April 1991, for example, a dwelling which has been built without permission should be banded having regard to how the market would have viewed it as at 1 April 1991, as compared to others for which planning approval had been obtained.

4.2 Vacant possession

The assumption as to vacant possession serves to ensure that any statutory provision or other circumstance which has an effect on value either by way of affording protection to an occupier or by allowing that person to purchase at a reduced figure, for example under the Right to Buy provisions of the Housing Act 1985, is to be disregarded.

It should be noted that the assumption is only to be made in respect of the actual dwelling being banded as at 1 April 1991. For example, if the dwelling to be banded is a tenanted local authority owned flat situated within a block of similar units or a tenanted cottage on a large rural estate, regard must be had to the actual nature of the occupation of the surrounding premises as at 1 April 1991 and any consequential effect on the vacant possession value of the subject dwelling.

4.3 Tenure

All premises, excluding only those which may be defined as flats, are to be valued on the basis that it is a freehold interest which is for sale.

Flats, irrespective of the actual length of the remaining term or rent paid, are to be valued on the basis that there is the benefit of a lease for 99 years at a nominal rent. Consequently there will sometimes be instances where there is a substantial difference between the price a dwelling might have been expected to achieve if marketed as at the antecedent valuation date of 1 April 1991 and the valuation arrived at in accordance with the regulations.

Reg 6(5) defines “flat” as having the same meaning as in Part V of the Housing Act 1985. S.83 of that Act provides:

(2) A dwelling-house is a house if, and only if, it (or so much of it as does not consist of land included by virtue of S.184) is a structure reasonably so called; so that -

(a) where a building is divided horizontally, the flats or other units into which it is divided are not houses;

(b) where a building is divided vertically, the units into which it is divided may be houses;

(c) where a building is not structurally detached, it is not a house if a material part of it lies above or below the remainder of the structure.

(3) A dwelling-house which is not a house is a flat.

Thus any dwelling, irrespective of its actual description and tenure, should be regarded as a flat if it satisfies the above definition. In essence, a property which forms part of a building will be a flat unless it is divided vertically from the rest of the building and no material part of it lies above another part of the structure.

4.4 Repair

NB CTM: PN4 deals with Repair in more detail

It is required to be assumed that the dwelling was in a “state of reasonable repair”. Regulation 6(6) states,

“In determining what is “reasonable repair” in relation to a dwelling for the purposes of paragraph (2), the age and character of the dwelling and its locality shall be taken into account.”

Age

The “age” of a dwelling will naturally affect the standard of repair which could reasonably be expected by a prospective purchaser but it is necessary to consider this factor in the context of the other two mentioned in the regulation. For example, the mere fact that a property is modern does not necessarily mean that it can be assumed to be in good repair. Due to a particular design, or the fact that properties in a locality have generally been allowed to deteriorate, the state of repair which might reasonably be expected may be lower than that attaching to similar properties outside the locality.

Locality

“Locality” as used in Reg 6(6) may be taken to be any area or district which is generally recognised and described as such, not necessarily only by reference to the housing stock, but also by reference to the district’s associated infrastructure and the level of amenities it is seen to enjoy.

Character

The “character” of a dwelling may be seen to consist of all those characteristics which are peculiar to it (as opposed to its locality) including any advantages or disabilities which exist.

Often the character of any given dwelling will be the same as that exhibited by neighbouring dwellings of a similar age and design and there will be little problem in arriving at the state of repair to be assumed. For example, if one dwelling on an estate of identical houses has been allowed to deteriorate, its basic character would nevertheless be the same as that of the neighbouring property and the inferior state of repair existing would not be reflected in its valuation banding. Conversely, if one was valuing a dwelling in a row of Georgian town-houses, all of which have minor structural defects (which would never be remedied due to the expense involved), the state of repair assumed would be that which actually exists. Similarly when valuing any dwelling which has been designated defective under the Housing Defects Act 1984 regard must be had to the state of repair which actually attaches to that type of property in the locality.

There will, however, be instances where despite the fact that a property might be of a similar age and design its character will vary from that of its neighbours, for example a Victorian terrace might comprise various properties whose character is seen to vary considerably either due to general neglect or because substantial improvements have occurred. The role that the character of a given property will have in determining what is “reasonable repair” in any instance will depend upon the extent to which this character is seen to vary from that attaching to the majority of properties within the locality.

If it is considered that the character of any dwelling is so different from that of the majority of other dwellings within the locality, then it will generally be inappropriate to assume that the same state of repair exists. For example, in the case of a property which is in an inferior condition, if the works required to be carried out to achieve the same state of repair as that which attaches to the majority of other dwellings, would result in the creation of a dwelling which was wholly different in character in its repaired state from that presently existing, then a similar state of repair should not be assumed to exist. Such works would not constitute repair simply to make good the ravages of time, but rather renewal or improvement, and it cannot be assumed that they would be carried out. However, it may be assumed that repairs would be carried out to such an extent to bring the property up to the average state of repair of its peer group. Similarly, if a dwelling has been so substantially improved and extended, so as to become wholly different in character from those around it, the state of repair which it is appropriate to assume may well differ from that state which attaches to its previously similar neighbours.

Where a dwelling is identified as being of a different character to that of its neighbours, it should be valued having regard to the state of repair which is seen to attach to dwellings which exhibit the same characteristics as those which exist in the subject dwelling. In such circumstances it may be appropriate to assume a state of repair exhibited by more comparable dwellings elsewhere than in the immediate vicinity.

Hereditaments and the repair assumptions: A useful summary of case law relating to a state of reasonable repair as it applied in the domestic Rating context is contained in Benjamin (VO) v Anston Properties Ltd (1998), in particular Wexler v Playle (VO) (1960) and Saunders v Maltby (VO) (1976). More recent cases, however, in relation to repair for CT are the High Court appeals in Burke v Broomhead (LO for Camden) 2009, RGM Properties v Speight LO 2011 and Wilson v Coll LO 2011.

In the Burke case, it was confirmed that if a hereditament existed, the repair assumption must be assumed and it was not possible to reduce a valuation on account of a necessary repair, in this case, the necessity of a new roof. A calculation as to whether it was an economic repair was unnecessary.

In RGM Properties v Speight this principle was spelt out in paragraph 35, “The assumption as to a reasonable state of repair, applies…only if a building is already accepted as a hereditament …..It is not relevant to determining that a property which is plainly uninhabitable but could be made habitable by reasonable repair is in some magical way capable of occupation so as to be a hereditament. The proposition is obvious: a barn without a roof which might be converted into a dwelling is not capable of occupation for the purposes of a dwelling, merely because it could be repaired to reach that state. Once it is however put into position as being capable of being a dwelling, the fact that elements of disrepair about and around it do not affect the banding….”

In Wilson V Coll, a landlord argued that a hereditament did not exist because it made no made no economic sense for him to do so. The Judgement confirmed that whether a repair was economic or not was not a relevant consideration in council tax, as it was in Non-Domestic Rating. If a vacant property was capable of normal repair, without major reconstruction or character changing work, then it would still qualify as a hereditament and thus a dwelling. It was also emphasized that the initial hereditament question is entirely separate from the subsequent repair assumption with regard to reasonable repair of a dwelling. Only if a hereditament exists, can the repair assumption be invoked, and the two ‘repair’ issues should not be confused.

Dwellings subject to major repair work or structural alterations

With effect from 1 April 2000 article 2 of the Council Tax (Exempt Dwellings) (Amendment) (England) Order 2000 (SI 424) amends Class A of the 1992 Order SI 558 to limit the exemption from Council Tax for a vacant dwelling subject to structural alteration or requiring or subject to major repair work, to a maximum of 12 months. “Major repair work” includes structural repair work. This order revokes SI 1999/1522.

Empty houses or flats awaiting demolition should be treated in accordance with advice given in CTM PN4 para (6) where Local Government Act 1988 S66 (5) may come into play.

Summary

It is necessary to judge each case of repair on its own merits within the meaning of “state of reasonable repair.” In the vast majority of cases the state which might reasonably be expected will be readily apparent as evidenced by the standard of repair attaching to the majority of similar dwellings (in terms of age, character and location) and it is this state which is to be assumed when banding. Only in those cases where the character of a dwelling is wholly different from the majority of its neighbours should one vary from the general level being adopted, at which time it will be necessary to have regard to the state of repair attaching to similar dwellings elsewhere.

4.5 Derelict properties

No property will constitute a dwelling unless it would have been a hereditament for the purposes of S.115(1) of the General Rate Act 1967 (S.3(2) of the LGFA 1992). Accordingly, where a domestic property is derelict or undergoing structural alterations to the extent that it is not ready for, nor capable of, beneficial occupation, it will not constitute a dwelling for the purposes of S.3 of the LGFA 1992. (See CTM: PN 4).

4.6 Size, layout and character of the dwelling and the physical state of the locality

Regs 6(2)(d) and 6(3) refer to the assumptions to be made in respect of the size, layout and character of the dwelling and the physical state of its locality. For valuation purposes, the regulations require it to be assumed that these variables were the same as at the AVD of 1 April 1991 as those actually existing at later dates. The variables are taken back to AVD for the purposes of valuation. The date(s) at which each variable needs to be considered whilst having regard to the level of values existing at the AVD will depend upon the occasion giving rise to the alteration of the list. (See CTM: PN3).

This section considers those matters which may be reflected under:

(a) Size and Layout

(b) Character

(c) Physical state of the locality

a) Size and layout

A change in the size and layout of a dwelling will usually arise through structural alterations being carried out which reduce or increase the size of the property and/or alters its floor plan.

If structural alterations causing a reduction in value occur, the definition of “Material reduction” will usually be satisfied and, if appropriate, an alteration of the list may be made. If however, structural alterations increase the value of the property an alteration to the list cannot be made to reflect this “material increase” until there has been a “relevant transaction” (CTM: PN3).

b) Character

Any matter which can be considered to have a direct effect on the character of any dwelling (as opposed to its locality), and is not otherwise excluded by any of the assumptions contained in Reg 6(2), will generally fall to be reflected as it existed at a date other than the AVD.

However the word “character” does not allow a planning restriction or restrictive covenant, not otherwise made irrelevant by virtue of Reg 6(2)(h) or (i), to be reflected as it existed at a date other than the AVD. (For the treatment of planning restrictions and restrictive covenants which attach to properties see sections 4.10 and 4.11 below).

c) Physical state of the locality

“Physical state of locality” may be taken to mean that which is readily apparent to anyone viewing that locality, without knowing or being made aware of any economic, social, legal or other non-physical factors affecting the locality.

This definition does not allow it to be argued that factors such as unemployment, the prospect of development, or the designation of a conservation area were any different from those actually existing at 1 April 1991. These factors may be reflected in the banding of a property only insofar as they may have affected its value at 1 April 1991, assuming they do not otherwise affect the physical state of the locality.

4.7 Use as a “private dwelling”

Reg 6(2)(h) requires it be assumed that,

“the use of the dwelling would be permanently restricted to use as a private dwelling”.

“Private dwelling” in the above context should be taken to mean a dwelling which is used primarily for private or domestic (as opposed to commercial or public) purposes. The definition does not exclude any partial non-private use so long as it does not stop the dwelling from being considered to be private.

The extent to which non-private uses may exist before they offend the definition of a private dwelling will be a matter of fact and degree in each case. Only if a use prevents a dwelling from being regarded as private should the effect of that use on its value be disregarded for banding purposes. For the purpose of clarification, those small guesthouses and holiday homes which are used for minor commercial purposes and defined as being wholly domestic by virtue of S.66(2A) and (2B) LGFA 1988 as amended respectively, are to be treated as being private dwellings for the purposes of Council Tax.

Situations where it is appropriate to adjust the market value to accord with the statutory assumption will be seen to be extremely rare. In most cases any substantial non-private use of any dwelling will result in the dwelling becoming a composite hereditament when Reg 6(2)(h) will not be applicable (CTM: PN6).

4.8 “Permitted development”

It is to be assumed that the dwelling under consideration had no development value other than that attributable to “permitted development”. Permitted development is defined in Reg 6(5) as being development:-

“for which under the Town and Country Planning Act 1990 planning permission is not required, or for which no application for planning permission is required”

reflecting the differing situations which exist under Sections 57 (planning permission required for development) and 59 (development orders; general) respectively of the Town and Country Planning Act 1990.

Consequently, regard is to be had to both the Use Classes Order 1987 and the General Development Order 1988 along with any additional value they are seen to attach to a particular premises.

For example, any increases in value by virtue of there being a strong demand for holiday homes in a locality (a use permitted by class C3), or a plot being of sufficient size to allow development which would be granted permission by the General Development Order, should be correctly reflected in any valuation for banding purposes.

Conversely, any “hope” of obtaining planning permission in respect of a dwelling as at the AVD, which would have had the effect of increasing its value, should be disregarded as this would offend the definition of permitted development as contained in Reg 6(5). For example, a dwelling in, or on the verge of, an area where a substantial number have been converted into offices might well have had a market value in excess of similar dwellings in the immediate neighbourhood, but its banding will be the same.

It is to be noted that whilst there may be no difficulty in adequately reflecting any value which is attributable to “permitted development” (as such value is generally inherent in the open market sale price of a property), special attention should be paid to those factors which, though not always readily identifiable, are clearly outside its definition and must not be taken into account.

4.9 Rentcharges and incumbrances

It is to be assumed that no “rentcharge or other incumbrance” attaches to any dwelling. (Reg 6(2)(c)).

Reg 6(5) defines rentcharge as having the same meaning as in the Rentcharges Act 1977 which states (in section 1),

“For the purpose of this Act, “rentcharge” means any annual or other periodic sum charged on or issuing out of land, except –

(a) rent reserved by a lease or tenancy, or

(b) any sum payable by way of interest”.

The phase “or other incumbrance” should be interpreted in a restrictive sense namely something which it is in the power of the vendor to remove by his own unilateral action. Effectively that is limited to financial restrictions such as a mortgage on the dwelling. Thus there is a statutory right to redeem a rent charge in Sections 8-10 of the Rent Charges Act 1979; mortgages and other financial changes can be similarly redeemed as can a judgement against the land by paying the amount of the judgement.

Easements, rights of way , restricted covenants and planning restrictions are all ‘incumbrances’ in the widest sense of the word, but cannot be lifted by the unilateral action of the vendor. They therefore fall outside this valuation assumption that the dwelling is sold free from any such incumbrances as existed at the relevant date, with the result that such restrictions CAN be reflected in the valuation. Rentcharges, mortgages liens and the like must NOT be reflected in the valuation.

Support for this argument may also be gained by considering the order of the assumptions in regulation 6(2) of 1992 SI No 550. Assumptions (a) to (c) relate to the interest being valued, (d) to (g) to physical matters concerning the dwelling and its locality, and planning matters are referred to in (h) and (i). A planning restriction would therefore not fall within 6(2)(c) as an ‘incumbrance’.

4.10 Planning restrictions

Regard should only be had to a planning restriction which was, or may be deemed to have been, attached to a property as at 1 April 1991.

Only if a value significant restriction was either

(i) actually attached to a property as at 1 April 1991

or

(ii) attached to a property constructed after 1 April 1991 and prior to its inclusion in the valuation list, should it be taken into account for banding purposes.

Any planning restriction imposed on an existing dwelling or removed from a dwelling during the life of a list is a non physical change and should be ignored.

Relevant case law: The relevance of a planning restriction was considered by the Court of Session in Scotland in Re the Appeal of Grampian Valuation Joint Board Assessor 2003 RA167. It rejected an appeal made by the assessor against the decision of the Valuation Appeal Committee that in valuing a dwelling for the purposes of council tax, an agricultural occupancy condition in the planning permission for its construction was not to be ignored. There was nothing in the Council Tax (Valuation of Dwellings) (Scotland) Regulations 1992 which stated or implied that a planning restriction that affected the value of the dwelling should be ignored, and although under the regulations development value was to be ignored, the assessor was not required to ignore any depreciation in value that was due to a planning restriction. The contention that the planning condition fell to be ignored involved a departure from reality that was required neither by the assumption of a sale on the open market or by any of the specific valuation assumptions. Although the regulations in Scotland differ slightly from the wording of the equivalent regulations in England and Wales, the decision is equally applicable and should be followed.

Weight to be given: Where a planning restriction is correctly to be taken into account the likelihood of getting the restriction lifted at the AVD should be reflected in arriving at the valuation. Regard should be had to the local authority’s general policy on such matters and how they were seen to treat applications to have similar restrictions lifted as at AVD.

Agricultural occupancy restriction: If the restriction was attached to a property on or before 1 April 1991, or imposed on anew dwelling during the life of a list any reduction in value caused by its existence should be reflected. Imposition or removal of planning restrictions to existing dwellings should be ignored as these are non-physical factors, unless associated with changes to the curtilage.

Thus the removal of an agricultural restriction should be ignored unless it is carved out from the main farm holding, in which case it will be a split from the main hereditament and be treated as a new dwelling with different boundaries.

Key worker restrictions: Planning agreements made under Section 106 of the Town & Country Planning Act 1990 often include references to low cost housing and restricted to key workers, eg nurses, teachers, police etc. The restriction on occupation may be reflected, where that is judged to affect value, but specific restrictions on price reflected in leases is to be disregarded as explained below.

4.11 Restrictive covenants

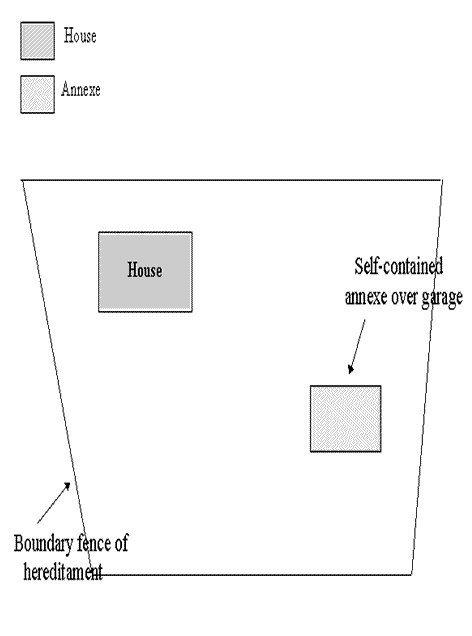

Restrictive covenants in a freehold or long leasehold interest which are not in the nature of a “rent charge or incumbrance” should be taken into account for Council Tax purposes and assumed to coexist with the hypothetical sale on the grounds that the dwelling must be valued on the assumption of a hypothetical sale of the freehold, or 99 year lease in the case of a flat. Coll v Walters 2016 EWHC 831 (Admin), a High Court case, examined whether a restrictive covenant benefiting neighbouring land should be taken into account. The restrictive covenant, benefiting the neighbouring land, provided that the house and an annexe in the garden, together the subject property, should not be occupied separately. The judge held that a restrictive covenant of this nature fell outside the definition of Reg 6 (2) ( c) “ free from any rent charge or other incumbrance” and, as such, had to be taken into account in the banding. The freehold was encumbered by the restriction and it is the freehold that has to be valued in the case of a house. It is considered the same answer would result with a flat notwithstanding the assumption of a 99 year lease rather than the actual lease. This is because the restrictive covenant would have an existence outside the actual dwelling being considered, as it benefitted other land.

By way of contrast , a restrictive covenant that provided a mechanism to create a discounted sale price should be ignored because it is in the nature of a “rent charge or incumbrance” . An appeal was made to the High Court by the Listing Officer in 1994 against the decision of the Birmingham Valuation Tribunal, that 52 dwellings in a sheltered housing development in Selly Park Birmingham, owned by the Sanctuary Housing Association, should be valued by reference to the restricted re-sale value of the leasehold interest under the terms of the lease i.e. 70% of the open market. This restriction was imposed because of the original funding of the development by way of 30% grant aid.

Legal advice was that Regulation 6(1) requires value to be ascertained for a hypothetical sale of the dwelling in question, not the particular interest which is held by the occupier. In the case of a flat that is a 99 year lease, and in the case of other properties a sale of the freehold is to be assumed. In neither case is the actual interest relevant, nor can price restrictions within that lease be taken into account.

The case was settled on this basis with solicitors acting for all parties by means of a Consent Order of the High Court and the original bands were restored. Listing officers should not, therefore, reflect price restrictions in bands.

4.12 Use of common parts

“Common parts” are defined in Reg 6(5) as being, in relation to a dwelling,

“any part of a building containing the dwelling and any land or premises which the owner or occupier of the dwelling is entitled to use in common with the owners or occupiers of other premises in the immediate locality”.

Where an owner or occupier is entitled to use “common parts”, it is to be assumed that those parts are not only in a state of reasonable repair, as defined above, but that the purchaser would be liable to contribute towards the cost of keeping them in this state. (Reg 6(2)(f)).

Even if, in practice, no contribution is actually required to be made for the upkeep of common parts, the valuation for banding purposes is to assume such an outgoing if the owner or occupier is entitled to their use. In such instances the amount of expenditure to be incurred should be estimated by having regard to how such a cost would be apportioned if actually demanded.

4.13 Service charges

Service charges are not specifically referred to in the regulations and accordingly regard should generally be had to those which were actually payable (or were deemed to be payable in the case of new property) as at 1 April 1991, and the extent to which they were seen to affect value.

However, it should be noted that where a service charge includes an amount to reflect the cost of repairing a property whose state of repair is not consistent with the assumptions contained in Reg 6(2)(e) and (f), then the valuation is to have regard to the assumed additional or reduced charge that would be required as opposed to the actual charge which was passing at 1 April 1991.

4.14 Disabled persons provisions

There is a specific provision contained in the regulations concerning a dwelling which has been made suitable for use by a physically disabled person.

Reg 6(2)(g) states that if a dwelling contains fixtures to which the sub-paragraph applies, then such fixtures are to be assumed not to be included in the dwelling. Reg 6(4) identifies these fixtures as follows;

“Sub-paragraph (g) of paragraph (2) applies to any fixtures which –

(a) are designed to make the dwelling suitable for use by a physically disabled person; and

(b) add to the value of the dwelling”.

Consequently any fixtures which satisfy the criteria laid down in Reg 6(4) should be assumed not to be included in the dwelling, (all fittings are already excluded under the general basis of valuation to be applied, see 4:15). Fixtures which are designed to make a dwelling more suitable for use by a physically disabled person will be extremely varied but will include ramps, some sanitary appliances, rails, chair lifts etc. It is to be noted that the actual use to which such features are put is irrelevant when considering whether they are appropriate for exclusion.

Where any fixture which has been designed to make a dwelling suitable for use by a physically disabled person does not add value to the property, it will not satisfy Reg 6(4) and must not be treated as a relevant fixture for the purposes of Reg 6(2)(g). Consequently, regard is to be had to the existence of the fixture and any reduction which it may cause when considering the appropriate band which should be ascribed to the property.

It should be noted that The Council Tax (Reductions for Disabilities) Regulations 1992 (SI No. 554) provide that the Council Tax bill of a person to whom the regulations apply (“the eligible person”) will, except in the case where a dwelling has been ascribed a band A, be calculated as if the dwelling was in a lower valuation band than is in fact the case. This is a charging provision and not one of valuation. Offices must not, therefore, become involved in discussions as to whether an individual qualifies as an “eligible person”. Taxpayers may be advised of the regulations’ existence but informed that it is a matter for the Billing Authority to determine.

4.15 Fixtures and fittings

When considering the value of any dwelling the effect of any fittings is to be ignored. Only items which may be considered to be fixtures are to be reflected unless, in relation to physically disabled persons, they are excluded by virtue of Reg 6(2)(g) (see 4:14).

The mere fact that an item may be fixed does not automatically mean that it is to be regarded as a fixture. Similarly, simply because any item is not actually fixed does not necessarily mean that it is a fitting.

Regard is to be had not only to the degree of fixing but also the actual purpose of the fixing. If the main purpose of the fixing is in order to allow the better enjoyment of an item, as opposed to trying to effect an improvement in the dwelling, the item is to be regarded as a fitting. Conversely, if an item which is not fixed is placed to effect an improvement to the dwelling it is to be regarded as a fixture.

Fittings: Carpets and Curtains

Fixtures: Bathroom Suites, Kitchen Units, Secondary Glazing, Central Heating.

4.16 The concept of ‘tone of the list’

In the High Court decision of Domblides v Listing Officer 2008, Counsel for the LO had introduced into her argument the concept of ‘tone of the list’. This is a familiar concept to Rating, but not until that time for Council Tax. This decision showed that evidence for banding can be gleaned, not from primary sales evidence, but (in that case) from decided cases. Hence the need for primary sales evidence is not always necessary to prove a band in a list that has been established over time. In his decision the Judge said:

“Secondly, it is the case that over time valuation tribunals’ decisions will shift from a consideration of individual sale prices, as they were in 1991, and will develop a body of case law which establishes that certain types of properties fall within bands. Thus, in relying on the later decisions, the tribunal is not relying on specific valuations; though it was specific valuations that underlay the subsequent decisions of the tribunal. This resembles the accepted method of valuation known as relying on the, “tone of the list” and this is an appropriate valuation method that is supported by a reference to Ryde on Rating”.

He continued:

“It is very important to note that the further away one gets from the 1991 list the more appropriate it becomes for the valuation tribunal or the listing officer to have regard, particularly in the interests of consistency, to the decisions of the tribunal….”

5. Valuation bands

All dwellings are to be ascribed valuation bands for the purpose of S.23(2) of the Local Government Finance Act 1992, in accordance with those set out in S.5(2) and (3) of the Act, namely,

In England

|

Valuation band |

Range of values |

| A |

Not exceeding £40,000 |

| B | Exceeding £40,000 but not exceeding £52,000 |

| C | Exceeding £52,000 but not exceeding £68,000 |

| D | Exceeding £68,000 but not exceeding £88,000 |

| E | Exceeding £88,000 but not exceeding £120,000 |

| F | Exceeding £120,000 but not exceeding £160,000 |

| G | Exceeding £160,000 but not exceeding £320,000 |

| H | Exceeding £320,000 |

And, in Wales

|

Valuation band |

Range of values |

|

A |

Not exceeding £30,000 |

|

B |

Exceeding £30,000 but not exceeding £39,000 |

|

C |

Exceeding £39,000 but not exceeding £51,000 |

|

D |

Exceeding £51,000 but not exceeding £66,000 |

|

E |

Exceeding £66,000 but not exceeding £90,000 |

|

F |

Exceeding £90,000 but not exceeding £120,000 |

|

G |

Exceeding £120,000 but not exceeding £240,000 |

|

H |

Exceeding £240,000 |

1.0 Introduction

The Local Government Finance Act (LGFA)1992 requires the Commissioners of Inland Revenue (now HMRC) to carry out valuations of dwellings in England and Wales for the purposes of compiling and maintaining valuation lists (sections 20-23), and specifies bands within which dwellings are to be placed (Section 5). The Act also requires that a similar valuation exercise be carried out in Scotland by the Scottish Assessors, acting under the direction of the Commissioners.

The Council Tax (Situation and Valuation of Dwellings) Regulations 1992 as amended by The Council Tax (Situation and Valuation of Dwellings) (Amendment) Order 1994 (hereinafter referred to as “the regulations”) contain, inter alia, the basis of valuation to be adopted when banding for Council Tax purposes.

2.0 Definition of dwelling

It is Section 3 of the LGFA 1992 that defines what a “dwelling” is for CT and reads as follows:

(1) This section has effect for determining what is a dwelling for the purposes of this Part.

(2) Subject to the following provisions of this section, a dwelling is any property which - a) by virtue of the definition of hereditament in section 115(1) of the General Rate Act 1967, would have been a hereditament for the purposes of that Act if that Act remained in force; and b) is not for the time being shown or required to be shown in a local or a central non-domestic rating list in force at that time; and c) is not for the time being exempt from local non-domestic rating for the purposes of Part III of the Local Government Finance 1988 Act (“the 1988 Act”); and in applying paragraphs (b) and (c) above no account shall be taken of any rules as to Crown exemption.

(3) A hereditament which - a) is a composite hereditament for the purposes of Part III of the 1988 Act; and b) would still be such a hereditament if paragraphs (b) to (d) of Section 66(1) of that Act (domestic property) were omitted, is also, subject to subsection (6) below, a dwelling for the purposes of this Part.

(4) Subject to subsection (6) below, none of the following property, namely - a) a yard, garden, outhouse or other appurtenance belonging to or enjoyed with property used wholly for the purposes of living accommodation; or b) a private garage which either has a floor area of not more than 25 square metres or is used wholly or mainly for the accommodation of a private motor vehicle; or c) private storage premises used wholly or mainly for the storage of articles of domestic use, is a dwelling except in so far as it forms part of a larger property which is itself a dwelling by virtue of subsection (2) above.

(5) The Secretary of State may by order provide that in such cases as may be prescribed by or determined under the order - a) anything which would (apart from the order) be one dwelling shall be treated as two or more dwellings; and b) anything which would (apart from the order) be two or more dwellings shall be treated as one dwelling.

(6) The Secretary of State may by order amend any definition of “dwelling” which is for the time being effective for the purposes of this Part.”

2.1 Points to note:

In respect of the above definition, the following points are to be noted;

(i) Hereditament is defined in Section 115(1) of the General Rate Act 1967 as being, “property which is or may become liable to a rate, being a unit of such property which is, or would fall to be, shown as a separate item in the valuation list”. It is case law, however, which tells us what this means in practice.

-

Hereditament in relation to CT was examined in the case RGM properties v Speight LO 2011. In paragraphs 13-17, an analysis of the law was undertaken in relation to beneficial occupation. The authorities were examined and the practical definition linked to that expounded in Post Office v Nottingham City Council CA 1979 in the answer to the question “as a matter of fact and degree, is or will the building, as a building, be ready for occupation, or capable of occupation, for the purposes for which it is intended?”

-

In both the RGM case and Wilson v Coll LO 2011, the need to separate the ‘hereditament test’ as to whether an existing property is capable of reasonable repair, and the valuation assumptions to be applied (see paragraph 3 below) once it was found that a hereditament existed, was emphasised.

-

In R v East Sussex Valuation Tribunal Ex p. Silverstone 1996 RVR 203, it was confirmed that where two separate dwellings are converted into a single unit, a new dwelling comes into existence.

-

The case of Baker (VO) v Citibank LT 2007 confirmed the principle that a change in the boundaries of a hereditament created a new hereditament. It follows from this that where a dwelling either acquires or disposes of land, to add or subtract from its boundaries (that is not merely de minimis in extent), a new dwelling will have been created in each case. In these circumstances a relevant transaction is not necessary to trigger a band review where material increases have taken place.

-

A dwelling which is removed from the list because it becomes non-domestic property will cease to be a dwelling. If subsequently it becomes domestic property again and qualifies as a dwelling it will be treated as a new dwelling when brought back into a CT list. Any improvements which may have occurred will be taken into account as part of the new dwelling.

(ii) Exemptions for the purposes of Part III of the LGFA 1988 are listed in its 5th Schedule.

(iii) Any property which satisfies the definition in Section 3 LGFA 1992 but is in the occupation of the Crown is nevertheless a dwelling for Council Tax purposes.

(iv) Any property which is a composite property as defined by Section 64(9) of the LGFA 1988 is a dwelling unless it forms such a hereditament by virtue of the fact that it contains only domestic property defined in paragraphs (b) to (d) of Section 66(1) of the 1988 Act.

(v) Any property included in those categories mentioned in S.3(4)(a) (b) and (c) LGFA 1992 will never constitute a dwelling in isolation. It will only ever be a dwelling to the extent that it forms part of a larger dwelling. Such property will only form part of a larger dwelling if, for the purposes of the General Rate Act 1967, it would have formed part of a hereditament as defined by S.115(1) e.g. a house and garage occupied together and situated within a single curtilage will together form a single dwelling.

-

A garage which is physically separated by a main road, from the dwelling house with which it is enjoyed, will not comprise a dwelling in its own right or be regarded as forming part of the dwelling. (It would have formed a separate hereditament for the purposes of the General Rate Act 1967). Similarly a garage situated within the curtilage of a block of flats will not comprise part of a dwelling if, for the purposes of the 1967 Act, it would have formed a separate hereditament. The value of any such garage should not be reflected directly in the value of the individual dwelling.

-

Communal facilities such as car parking areas, gardens, communal lounges at a block of flats or sheltered housing development will not generally comprise a dwelling in their own right but the value of such facilities will fall to be reflected in the market values of the individual units.

-

In those instances where a facility is used by both owners of adjoining living accommodation, as a right of occupation of their respective hereditaments and individuals living elsewhere (provided the latter use is not de minimis) it will have been treated as non-domestic property, e.g. leisure facilities at a luxury development. The right to use such facilities should be reflected in the market values of the individual dwellings.

(vi) The power conferred on the Secretary of State in subsection (5) has been exercised in the form of The Council Tax (Chargeable Dwellings) Order 1992 (SI No. 549) as amended by The Council Tax (Chargeable Dwellings, Exempt Dwellings and Discount Disregards) Amendment Order 1997 (SI No 656) and the Council Tax (Chargeable Dwellings, Exempt Dwellings and Discount Disregards)(Amendment) (England) Order 2003 SI 3121 . Articles 3 and 3A of the Order detail the circumstances where properties which would otherwise form single dwellings are to be treated as more than one. Article 4 gives the listing officer a discretion in prescribed circumstances to treat properties which would otherwise form multiple dwellings as single ones. For instructions on the disaggregation and aggregation of dwellings see CTM: PN5 and PN6 respectively.

3. Basis of valuation – valuation assumptions

The basis of valuation for any dwelling is found in Regulation 6(1), (2) and (3) of The Council Tax (Situation and Valuation of Dwellings) Regulations 1992 (SI No. 550) as amended by the Council Tax (Situation and Valuation of Dwellings) (Amendment) Orders 1994 and 2005. Reg 7 simply sets out an apportionment approach for the valuation of a composite dwelling but does not affect the basic assumptions. Reg 6 is as follows:-

(1) Subject to Reg 7, for the purposes of valuations under Section 21 (valuations for purposes of lists) of the Act, the value of any dwelling shall be taken to be the amount which, on the assumptions mentioned in paragraphs (2) and (3) below, the dwelling might reasonably have been expected to realise if it had been sold in the open market by a willing vendor on 1 April 2003.

(2) The assumptions are:-

(a) that the sale was with vacant possession;

(b) that the interest sold was the freehold or, in the case of a flat, a lease for 99 years at a nominal rent;

(c) that the dwelling was sold free from any rent charge or other encumbrance;

(d) except in a case to which paragraph (3) or (3A) applies, that the size, layout and character of the dwelling, and the physical state of its locality, were the same as at the relevant date;

(e) that the dwelling was in a state of reasonable repair;

(f) in the case of a dwelling, the owner or occupier of which is entitled to use common parts, that those parts were in a like state of repair and the purchaser would be liable to contribute towards the cost of keeping them in such a state;

(g) in the case of a dwelling which contains fixtures to which this sub-paragraph applies, that the fixtures were not included in the dwelling;*

(h) that the use of the dwelling would be permanently restricted to use as a private dwelling; and

(i) that the dwelling had no development value other than value attributable to permitted development.

*Reg 6(2)(g) only applies to fixtures which are designed to make a dwelling suitable for use by a disabled person and which add to the dwelling’s value - this is covered in Reg 6(4) *(see 4.14 & 4.15 below).

(3) In the case of a valuation carried out for the purposes of an alteration of the valuation list resulting from a material reduction in the value of the dwelling, it shall be assumed that -

(a) the physical state of the locality of the dwelling was the same as on the date from which the alteration of the list would have effect; and

(b) the size, layout and character of the dwelling were the same

(i) in the case of an alteration resulting from a change to the physical condition of the dwelling, as on the date from which the alteration in the list would have effect;

(ii) in a case where there has been a previous alteration of the valuation list in relation to the dwelling, as on the date from which that alteration had effect;

(iii) in a case where in relation to the dwelling, there has been a relevant transaction within the meaning of Section 24, not resulting in an alteration of the valuation list, as on the date of that transaction;

(iv) in a case to which more than one of sub-paragraphs (i) to (iii) applies, as on whichever is the latest of the dates there mentioned; and

(v) in any other case, as on 1 April 2005.

(4) In the case of a valuation carried out for the purposes of an alteration to correct an inaccuracy in a list which arose -

(a) in the course of making a previous alteration which resulted from a material reduction in the value of the dwelling, or

(b) since the date of such an alteration by reason of an alteration which was the next alteration to be made and was neither the result of a material reduction in the value of the dwelling nor the occurrence of any of the events described in paragraph (5B) below,*

it shall be assumed that the physical state of the locality of the dwelling, and the size, layout and character of the dwelling are the same as on the dates which were applicable in respect of the previous alteration in accordance with paragraph (3) above.

-End of extract-

The basis of valuation for any dwelling which is a composite hereditament or part of a single property which is a composite hereditament is contained in Reg 7(1) of The Council Tax (Situation and Valuation of Dwellings) Regulations 1992. For instructions on the valuation of such dwellings see CTM: PN 2.

4.0 Interpretation and application of basis of valuation

4.1 Open market value as at 1 April 2003

(a) “Reasonably expected” and “open market”

“Reasonably expected” and “open market” are not defined in the regulations but may be taken as having the same meaning as when used in a similar context in S.272(1) of the Taxation of Chargeable Gains Act 1992 and S.160 of the Inheritance Tax Act 1984.

It is therefore necessary to assume that

(i) all preliminary arrangements have been made prior to disposal

(ii) adequate publicity has been given to the sale

(iii) the most appropriate method of sale has been chosen so as to maximise the proceeds of the sale.

(NB Lotting – selling in parts - cannot be assumed as this would be inconsistent with the concept of the hereditament from which the dwelling is derived).

Problems can arise when a covenant is entered into a conveyance of the freehold or long leasehold interest, restricting the value on re-sale of the interest, to a percentage of the open market value of the dwelling. This restriction must be ignored for Council Tax purposes. (See paragraph 4.11 Restrictive Covenants).

Open market value will be determined by having regard to all the evidence of sales of similar dwellings in the locality at the antecedent valuation date (1 April 2003). Prices paid for new properties purchased from a builder should be treated with caution, since they often reflect a “new build premium” which will not be payable in the second-hand market from where the bulk of sales evidence is drawn.

(b) “Willing Vendor”

The term “willing vendor” is not defined in the regulations but may be taken to have the same meaning as “willing seller” as contained in S.5 of the Land Compensation Act 1961 (Rule 2) ie. not a person selling without reserve but one who does it as a free agent as opposed to one who is forced to sell.

(c) Special Purchaser and Marriage Value

The definition of open market value does not specifically exclude either a special purchaser or marriage value. However, an increase in value which is attributable to a situation where either a special purchaser or marriage value is seen to exist will often be excluded by virtue of Reg 6(2)(h) and (i) (ie the requirement to assume a restriction on use and limited development value only).

Where the existence of a special purchaser is identified and the above regulations would not be offended, regard should only be had to any overbid if it can be established that such a bid would have been made if the dwelling had been marketed at 1 April 2003.

(d) Number of properties assumed to be on the market as at 1 April 2003

No reduction should be made on account of a theoretical “flooding of the market” on 1 April 2003.

Regs 6 and 7 refer to the valuation of any one property as at the date of valuation and does not permit the assumption that all dwellings are placed on the market at the same time. In other words the valuer should consider that the equilibrium of the market place is maintained in the state which actually existed on 1 April 2003.

Accordingly the valuation of any dwelling is to be approached as if it were simply one additional dwelling coming on to the existing market as at 1 April 2003.

(e) Unlawful use of property

Reg 6(2) does not require an unlawful use of a property to be disregarded.

The banding of any property where any unlawful use is apparent should therefore take into account the value which the market would have placed on that use as at 1 April 2003, e.g. a dwelling which has been built without permission should be banded having regard to how the market would have viewed it as at 1 April 2003, as compared to others for which planning approval had been obtained.

4.2 Vacant Possession

The assumption as to vacant possession serves to ensure that any statutory provision or other circumstance which has an effect on value either by way of affording protection to an occupier or by allowing that person to purchase at a reduced figure, for example under the Right to Buy provisions of the Housing Act 1985, is to be disregarded.

It should be noted that the assumption is only to be made in respect of the actual dwelling being banded as at 1 April 2003. For example, if the dwelling to be banded is a tenanted, local authority owned flat situated within a block of similar units or a tenanted cottage on a large rural estate, regard must be had to the actual nature of the occupation of the surrounding premises as at 1 April 2003 and any consequential effect on the vacant possession value of the subject dwelling.

4.3 Tenure

All premises, excluding only those which may be defined as flats, are to be valued on the basis that it is a freehold interest which is for sale.

Flats, irrespective of the actual length of the remaining term or rent paid, are to be valued on the basis that there is the benefit of a lease for 99 years at a nominal rent. Consequently there will sometimes be instances where there is a substantial difference between the price a dwelling might have been expected to achieve if marketed as at the antecedent valuation date of 1 April 2003 and the valuation arrived at in accordance with the regulations.

Reg 6(5) defines “flat” as having the same meaning as in Part V of the Housing Act 1985. S.83 of that Act provides:

(2) A dwelling-house is a house if, and only if, it (or so much of it as does not consist of land included by virtue of S.184) is a structure reasonably so called; so that –

(a) where a building is divided horizontally, the flats or other units into which it is divided are not houses;

(b) where a building is divided vertically, the units into which it is divided may be houses;

(c) where a building is not structurally detached, it is not a house if a material part of it lies above or below the remainder of the structure.

(3) A dwelling-house which is not a house is a flat.”

Any dwelling, irrespective of its actual description and tenure, should be regarded as a flat if it satisfies the above definition. In essence, a property which forms part of a building will be a flat unless it is divided vertically from the rest of the building and no material part of it lies above another part of the structure.

4.4 Repair

NB CTM: PN4 deals with Repair in more detail.

It is required to be assumed that the dwelling was in a “state of reasonable repair”.

Reg 6(6) states,

“In determining what is “reasonable repair” in relation to a dwelling for the purposes of paragraph (2), the age and character of the dwelling and its locality shall be taken into account.”

Age The “age” of a dwelling will naturally affect the standard of repair which could reasonably be expected by a prospective purchaser but it is necessary to consider this factor in the context of the other two mentioned in the regulation. For example, the mere fact that a property is modern does not necessarily mean that it can be assumed to be in good repair. Due to a particular design or the fact that properties in a locality have generally been allowed to deteriorate, the state of repair which might reasonably be expected may be lower than that attaching to similar properties outside the locality.

Locality “Locality” as used in Reg 6(6) may be taken to be any area or district which is generally recognised and described as such, not necessarily only by reference to the housing stock, but also by reference to the district’s associated infrastructure and the level of amenities it is seen to enjoy.

Character The “character” of a dwelling may be seen to consist of all those characteristics which are peculiar to it (as opposed to its locality) including any advantages or disabilities which exist.

Often the character of any given dwelling will be the same as that exhibited by neighbouring dwellings of a similar age and design and there will be little problem in arriving at the state of repair to be assumed. For example, if one dwelling on an estate of identical houses has been allowed to deteriorate, its basic character would nevertheless be the same as that of the neighbouring property and the inferior state of repair existing would not be reflected in its valuation banding. Conversely, if one was valuing a dwelling in a row of Georgian town-houses, all of which have minor structural defects (which would never be remedied due to the expense involved), the state of repair assumed would be that which actually exists. Similarly when valuing any dwelling which has been designated defective under the Housing Defects Act 1984 regard must be had to the state of repair which actually attaches to that type of property in the locality.

There will, however, be instances where despite the fact that a property might be of a similar age and design its character will vary from that of its neighbours, e.g. a Victorian terrace might comprise various properties whose character is seen to vary considerably, either due to general neglect or because substantial improvements have occurred. The role that the character of a given property will have in determining what is “reasonable repair” in any instance will depend upon the extent to which this character is seen to vary from that attaching to the majority of properties within the locality.

If it is considered that the character of any dwelling is so different from that of the majority of other dwellings within the locality, then it will generally be inappropriate to assume that the same state of repair exists. For example, in the case of a property which is in an inferior condition, if the works required to be carried out to achieve the same state of repair as that which attaches to the majority of other dwellings, would result in the creation of a dwelling which was wholly different in character in its repaired state from that presently existing, then a similar state of repair should not be assumed to exist. Such works would not constitute repair simply to make good the ravages of time but rather renewal or improvement and it cannot be assumed that they would be carried out. However, it may be assumed that repairs would be carried out to such an extent to bring the property up to the average state of repair of its peer group. Similarly, if a dwelling has been so substantially improved and extended, so as to become wholly different in character from those around it, the state of repair which it is appropriate to assume may well differ from that state which attaches to its previously similar neighbours.

Where a dwelling is identified as being of a different character to that of its neighbours, it should be valued having regard to the state of repair which is seen to attach to dwellings which exhibit the same characteristics as those which exist in the subject dwelling. In such circumstances it may be appropriate to assume a state of repair exhibited by more comparable dwellings elsewhere than in the immediate vicinity.

Hereditaments and the repair assumptions: A useful summary of case law relating to a state of reasonable repair as it applied in the domestic Rating context is contained in Benjamin (VO) v Anston Properties Ltd (1998), in particular Wexler v Playle (VO) (1960) and Saunders v Maltby (VO) (1976). More recent cases, however, in relation to repair for CT are the High Court appeals in Burke v Broomhead (LO for Camden) 2009, RGM Properties v Speight LO 2011 and Wilson v Coll LO 2011.

In the Burke case, it was confirmed that if a hereditament existed, the repair assumption must be assumed and it was not possible to reduce a valuation on account of a necessary repair, in this case, the necessity of a new roof. A calculation as to whether it was an economic repair was unnecessary.

In RGM Properties v Speight this principle was spelt out in paragraph 35, “The assumption as to a reasonable state of repair, applies…only if a building is already accepted as a hereditament …..It is not relevant to determining that a property which is plainly uninhabitable but could be made habitable by reasonable repair is in some magical way capable of occupation so as to be a hereditament. The proposition is obvious: a barn without a roof which might be converted into a dwelling is not capable of occupation for the purposes of a dwelling, merely because it could be repaired to reach that state. Once it is however put into position as being capable of being a dwelling, the fact that elements of disrepair about and around it do not affect the banding….”

In Wilson V Coll, a landlord argued that a hereditament did not exist because it made no made no economic sense for him to do so. The Judgement confirmed that whether a repair was economic or not was not a relevant consideration in council tax, as it was in Non-Domestic Rating. If a vacant property was capable of normal repair, without major reconstruction or character changing work, then it would still qualify as a hereditament and thus a dwelling. It was also emphasized that the initial hereditament question is entirely separate from the subsequent repair assumption with regard to reasonable repair of a dwelling. Only if a hereditament exists, can the repair assumption be invoked, and the two ‘repair’ issues should not be confused.

Dwellings subject to major repair work or structural alterations

With effect from 1 April 2000, article 2 of the Council Tax (Exempt Dwellings) (Amendment) (England) Order 2000 (SI 424) amends Class A of the 1992 Order SI 558 to limit the exemption from Council Tax for a vacant dwelling subject to structural alteration or requiring or subject to major repair work, to a maximum of 12 months. “Major repair work” includes structural repair work. This order revokes SI 1999/1522.